Tax evasion leads to large losses in government revenue. A recent study explores the limitations of a potential solution, third-party reporting

Tax evasion is a key concern for many governments around the world, particularly in developing countries. With this issue in mind, there is growing interest in third-party reporting – the verification of taxpayer reports against other sources. However, methods using third-party reporting may not always immediately lead to strong results. In particular, their effectiveness may be limited if the tax authority faces constraints on credible enforcement and if taxpayers can shift misreporting to non-third-party reported margins. We examine these issues in the context of a policy experiment in Ecuador.

Tax evasion reduces government capacity (Besley and Persson 2013) and can lead to large distortions in the economy (Skinner and Slemrod 1985). Historically, governments have relied on audits as a means to enforce proper payments (Allingham and Sandmo 1972). Recently, alongside a global revolution in information technology, governments are increasingly turning to third-party information. This involves verifying taxpayer reports against other sources, such as employer reports of salary and value-added tax (VAT) invoices, as a cheaper and more scalable tax enforcement mechanism (Kleven et al. 2011, Pomeranz 2015, Naritomi 2016). Can improvements in third-party reporting transform tax collection, particularly in developing economies?

In a new paper, we show that the effectiveness of third-party reporting in developing economies may be limited in practice along two dimensions (Carrillo et al. 2017). First, information verification must ultimately be backed by credible enforcement. Second, when there are other margins of the tax return that are not covered by third-party reporting, firms can continue to evade by substituting their misreporting to these margins.

Introduction of enforcement based on third-party information

What happens when a government introduces tax enforcement based on third-party information? To shed light on this question, we analysed the effect of notifications sent to firms in Ecuador regarding detected discrepancies on previously filed corporate income tax returns. Corporate taxes play a critical role in all modern tax systems, and in developing countries they typically represent more than half of a countries’ tax revenues.

Using VAT data from reported purchases by a firms’ clients, as well as other sources such as credit card sales, the Ecuadorian tax authority (Servicio de Rentas Internas, or SRI) developed estimates of a firms’ revenues based on third-party information.1 Between August 2011 and March 2012, the tax authority notified almost 8,000 firms about discrepancies that were detected between the sales they reported in their recent tax returns and third-party estimates. The tax authority focused their efforts on those with especially large revenue discrepancies, in line with how enforcement efforts are generally conducted by tax authorities in practice.

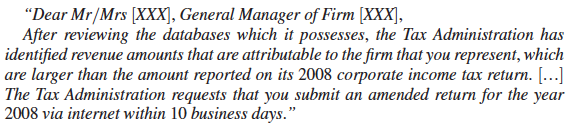

For discrepancies on 2008 returns, firms were notified of a general mismatch:

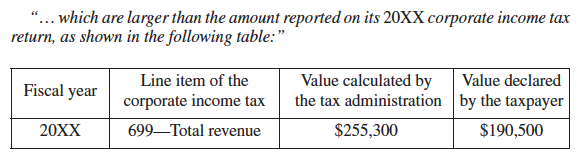

For 2009 and 2010 returns, the tax authority provided the actual numbers of the third-party information on the firm’s revenue:

Given that almost no other firms amended their tax returns precisely around the time of the notification (2-3 years after the original filing date), we can measure the causal effects of the intervention by simply comparing firms' pre-notification filings to post-notification reports.

Three key results stood out from the analysis:

1. Widespread misreporting

To contextualise the effects of discrepancy notifications, we first sought to understand the general reporting landscape in the full sample of active firms for which third-party information is available (>85,000 firms). Twenty-four percent of firm filings have self-reported revenues below third-party amounts, a lower bound on revenue underreporting. Additionally, we also present what is to the best of our knowledge the first evidence of cost underreporting: 26% of firm filings and 5% of those with positive tax liability report costs lower than third-party amounts (again, a lower bound on underreporting). This is consistent with a model in which the audit regime provides an incentive for firms to underreport scale (see Carrillo et al. 2017).

2. Limited responsiveness

While about 90% of e-mails were successfully delivered to addresses on file, only about 16% of all firms subsequently filed amendments. This may in part be due to the fact that a response was not explicitly required by law. It may also result from the realisation by firms and their accountants that the Ecuadorian tax authority did not have the capacity to follow up with an audit on all firms that had received such a notification. In this case, tax authorities may want to avoid sending out more deterrence messages than they have the capacity to follow up on. More generally, the challenges faced by many developing countries such as limits to capacity, poor legal regimes, and corruption, can undermine enforcement of the tax code, even conditional on informational improvements.

3. Inflating reported costs to compensate for higher reported revenues

Firms that did amend their tax returns made substantial revenue adjustments. When told the specific amount of the detected discrepancy (2009 and 2010 returns), 36% of firms matched the given amount exactly, and firms on average adjusted revenue by 93 cents per dollar of notified discrepancy. When firms weren’t told the amount (2008 returns), they adjusted their revenues only by about a third of the discrepancy. This suggests that they underestimated how much information the tax authority had.

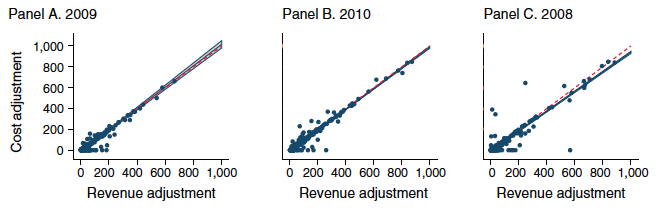

However, firms also increased reported costs by 96 cents for every dollar of revenue adjustment, indicating that third-party reporting had little effect on the ultimate levels of tax evasion (Figure 1). This pattern holds throughout the distribution of revenue adjustments, regardless of whether firms were given a specific revenue discrepancy amount.

Figure 1 Cost matching

Notes: The dashed line indicates a 45-degree line. Also shown are a fitted line and a 95 percent confidence interval for the fitted line. Slopes are as follows: 1.028 for the 2009 round, 0.993 for the 2010 round and 0.942 for the 2008 round. Axes are in thousands of US dollars and are restricted to show zero to one million, but the fitted line and confidence interval reflect the unrestricted sample.

For all adjusting firms, the notifications ultimately resulted in an average taxable profit increase of 3.7% of notified discrepancy, or $1,850 in actual tax payments.

Lessons for tax policy

If all amending firms had fully adjusted their revenues to third-party information and held other line items constant, the Ecuadorian tax authority would have received approximately $23 million in additional tax payments. Instead, these notifications resulted in around $2 million in additional payments. This $21 million gap reveals three implications for policymakers:

- Third-party information is not a silver bullet in solving the tax compliance problem in developing countries; its effectiveness will be determined in large part by other aspects of the information and enforcement environment. To the extent that enforcement capacity is limited, tax payers may not respond even when they know that the tax authority has information about discrepancies on their part, because they (correctly) expect the chance of the tax authority following up and prosecuting to be low. In addition, when third-party reporting exists only on one of several margins, taxpayers may substitute misreporting from the third-party reported margin to another. This has implications for the optimal tax base, in line with findings by Best et al. (2015).

- The fact that some firms may be underreporting their costs poses some considerable challenges for enforcement based on third-party reporting. It also undermines the ‘self-enforcing’ properties of VAT. The flip side of this problem is that enforcement based on third-party reported information that in turn leads firms to report more of such information can lead to positive spillovers.

- Third-party reporting and traditional tax enforcement can complement each other. On the one hand, without strong traditional enforcement capacities to follow up on discrepancy notifications, the latter will not have significant deterrence power. On the other, as some firms respond directly to the enforcement based on third-party reporting, the tax authority can refocus its auditing resources on those who don’t. Strengthening ‘traditional’ auditing and enforcement capacity in tandem with comprehensive third-party information cross-checks could be a desirable strategy for continually improving overall tax enforcement.

Photo credit: Ken Teegardin/flickr

References

Allingham, M G and Agnar, S (1972), “Income tax evasion: A theoretical analysis”, Journal of Public Economics 1 (3–4): 323–38.

Besley, T and Torsten, P (2013), “Taxation and Development”, in Handbook of Public Economics, Vol. 5, edited by Auerbach, A J, Chetty, R, Feldstein, M S and Saez, E 51–110. Amsterdam: North-Holland.

Best, M C, Brockmeyer, A, Kleven, H J, Spinnewijn, J and Waseem, M (2015), “Production versus Revenue Efficiency with Limited Tax Capacity: Theory and Evidence from Pakistan”, Journal of Political Economy 123 (6): 1311–55.

Carrillo, P, Pomeranz, D and Singhal, M (2017), "Dodging the Taxman: Firm Misreporting and Limits to Tax Enforcement", American Economic Journal: Applied Economics, 9(2): 144-64.

Kleven, H J, Knudsen, M B, Kreiner, C T, Pedersen, S and Saez, E (2011), “Unwilling or Unable to Cheat? Evidence from a Tax Audit Experiment in Denmark”, Econometrica 79 (3): 651–92.

Naritomi, J (2016), Consumers as Tax Auditors.

Pomeranz, D (2015), “No Taxation without Information: Deterrence and Self-Enforcement in the Value Added Tax”, American Economic Review 105 (8): 2539–69.

Skinner, J and Slemrod, J (1985), “An Economic Perspective on Tax Evasion”, National Tax Journal 38 (3): 345–53.

Endnotes

[1] Third-party information is a lower bound of true revenue, since third-party reporting is often incomplete. This means the tax authority’s measure likely provides an underestimate of a firm's true revenue.