Short-term foreign currency borrowing is largely used for carry trade-like activities rather than financing productive investment, underscoring the need to focus on debt maturity and firm heterogeneity when designing policies to manage financial risk.

In the years of cheap dollar funding following the global financial crisis, emerging market firms tapped international markets at an unprecedented scale. The surge in foreign currency corporate borrowing sparked a long-standing question: were firms merely financing productive investment, or were they behaving like ‘shadow banks’, borrowing in dollars at low interest rates to invest in higher-yielding local assets, effectively engaging in a form of carry trade?[1]

Despite the debate, little was known about firms' true currency exposure. Most firms are not required to disclose the currency composition of their balance sheets, leaving policymakers uncertain about whether foreign currency borrowing reflects prudent hedging or risky financial arbitrage.

Recent research has explored similar dynamics across emerging markets, finding that firms often act like financial intermediaries when global funding is cheap. According to the evidence base, as global carry-trade conditions improve, non-financial firms expand foreign-currency borrowing and place funds in higher-yielding local assets, mirroring classic carry-trade behaviour (Bruno and Shin 2017, Huang et al. 2024, Acharya and Vij 2025, Hardy and Saffie 2024). Yet the evidence rarely distinguishes between local- and foreign-currency liquidity and between short- and long-term foreign currency debt. Our analysis extends this work by directly linking debt maturity to firms’ currency-specific asset allocation.

Our work (Lee and Wu 2024) offers rare clarity. Using detailed firm-level data on Korea, we show that short-term foreign currency borrowing is directly tied to carry trade-like activity, while long-term borrowing is associated with more conventional financing behaviour. Our findings reveal a nuanced picture of how global liquidity conditions shape corporate risk-taking and point to better-targeted policies for managing external liabilities.

The missing piece: Currency positions across the balance sheet

Korea's accounting rules provide a unique window into firms' currency positions. Medium-sized companies are required to file detailed financial statements that include the currency denomination of assets and liabilities. Our dataset covers around 23,000 firms – ten times more than listed firms alone – providing an unusually comprehensive look at the corporate balance sheet.

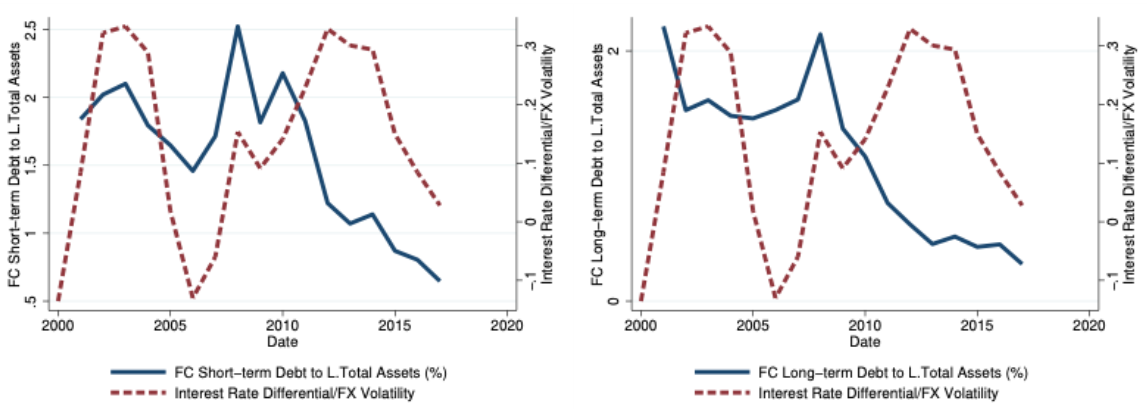

When we plot the ratio of foreign currency debt to lagged total assets against the interest rate differential between Korea and the US (normalised by FX volatility) a clear pattern emerges (Figure 1). As Korean rates rise relative to US rates, foreign currency borrowing, especially short-term, rises sharply. Cheap dollar funding, in other words, encourages firms to take positions that profit from interest rate gaps.

Figure 1: Firms’ foreign currency borrowing

Maturity determines behaviour

Our first major insight is that maturity determines behaviour.

Long-term foreign currency debt: When firms issue long-term foreign debt, they reduce local currency liquid assets – cash, deposits, and short-term financial instruments – consistent with the pecking order theory that firms draw down internal funds before seeking external finance.

Short-term foreign currency debt: In contrast, firms that issue short-term foreign debt increase local currency liquid assets. For every dollar borrowed in short-term foreign currency debt, firms save US$0.13 in local currency deposits and financial instruments. This suggests they are not borrowing to fund investment but to exploit the interest rate differential, an indicator of carry trade behaviour.

To establish this link, we use two strategies:

- We compare newly issued short-term foreign currency debt with the current portion of long-term debt (i.e. debt originally issued with long maturity but now nearing repayment). Only new short-term foreign currency borrowing increases local currency savings. This empirical observation confirms that cash inflows, not upcoming liabilities, drive the accumulation.

- We examine firms' interest income. If short-term foreign currency borrowing funded real investment, we would not expect higher interest income. Yet firms with more short-term foreign currency debt report significantly higher interest income, providing direct evidence that borrowed funds are parked in higher interest-bearing assets rather than invested in production.

Who borrows to carry trade?

Not all firms behave alike. On average, for every dollar borrowed in foreign currency, firms devote around $0.13 to carry trades.[2] The share rises sharply among certain groups: listed firms and financially dependent firms, as measured using Rajan and Zingales (1998)’s index of reliance on external finance:

| Type | Carry Trade Activity |

|---|---|

| Average firm | $0.13 per dollar |

| Listed firms | $0.25 per dollar |

| Financially dependent firms | $0.25 per dollar |

These findings suggest that large, listed firms and firms reliant on external financing are more inclined to exploit global interest rate differentials – behaving more like financial intermediaries than traditional producers.

Buffering the risks of carry trades

Carry trades sound risky – and they are – but the picture is not entirely one-sided. We find that many firms accumulate foreign currency liquidity buffers against exchange rate volatility. On average, firms add around $0.12 in foreign currency liquid assets for every dollar of short-term foreign currency borrowing – around $0.08 more than when they issue long-term foreign currency debt.

The buffer accumulation intensifies when exchange rate volatility increases, pointing towards active risk management rather than passive exposure.

Diverting funds from investment

This financial manoeuvring has real consequences. For each dollar of short-term foreign currency debt issued, firms reduce their capital expenditure by around $0.04. This implies that short-term foreign currency borrowing rarely finances productive investment. Instead, it fuels balance-sheet management – diverting funds away from long-term growth.

Firms with greater short-term foreign currency borrowing also earn more interest income, further supporting that a portion of these borrowed funds is held in interest-bearing assets rather than used for investment.

Policy implications: Targeting the right risk

Our findings offer two key lessons for policymakers:

- Focus on maturity not just quantity. It is short-term foreign currency borrowing – not overall foreign currency debt – that drives speculative exposure. Policies that treat all foreign currency debt equally miss this crucial distinction. Longer-term borrowing appears more conventional, funding real activities rather than financial arbitrage.

- Monitor firm heterogeneity not just aggregates. Not all firms are alike. There is a clear firm heterogeneity in incentives to participate in carry trades. Regulators should keep this heterogeneity in mind when designing policies.

Understanding how firms use foreign currency debt is as important as knowing how much they borrow. Korea's experience shows that even non-financial firms can behave like global traders when incentives align. They borrow in one currency to save in another, thereby profiting from interest rate differentials. The challenge for emerging market policymakers is not to shut off global finance but to channel it towards productive investment. By focusing on maturity structures of foreign currency borrowing and understanding firm heterogeneity in their incentives, regulators can better navigate the trade-offs between financial integration and stability.

References

Acharya, V V, and S Vij (2025), “Regulating carry trades: Evidence from foreign currency borrowing of corporations in India,” Review of Economic Studies 92(4): 2071–2107.

Bruno, V, and H S Shin (2017), “Global dollar credit and carry trades: A firm-level analysis,” Review of Financial Studies 30(3): 703–749.

Gratton, P (2025), “What is carry trade? Definition, example & risks explained,” Investopedia.

Hardy, B, and F Saffie (2024), “From carry trades to trade credit: Financial intermediation by non-financial corporations,” Journal of International Economics 152: 103988.

Huang, Y, U Panizza, and R Portes (2024), “Corporate foreign bond issuance and interfirm loans in China,” Journal of International Economics 152: 103975.

Lee, A S, and S P Y Wu (2025), “Carry trades and FX risk buffers: Foreign currency debt of emerging market firms,” Review of Economics and Statistics 1–45.