Performance-linked contracts, increasingly enabled by financial technology, can better spur investment among small firms than rigid microcredit—especially for risk- and loss-averse business owners.

Editor’s note: For a broader synthesis of themes covered in this article, check out Issue 3 of our VoxDevLit on Microfinance.

Microfinance institutions have rapidly expanded and are seen by many policymakers as key for small firm growth and poverty alleviation. While they have undeniably succeeded in extending credit to millions who would otherwise be excluded from formal financial systems, strikingly, multiple experimental studies have found that classic microcredit products yield only modest average impacts on key welfare-relevant outcomes such as household income and consumption (Banerjee et al. 2015). This is somewhat puzzling given the macro-level associations between financial access and growth (Beck et al. 2007) and extensive micro-level evidence on high returns to capital for small firms (De Mel et al. 2008, Liu and Roth 2022).

One explanation for these disappointing results is that many borrowers simply use loans for consumption rather than business investment. Yet for the subset of more entrepreneurial borrowers capable of high returns, can financing models in developing countries be improved? This is a key question given perennial policy discussions on the importance of small firms for employment and substantial funds channelled into small business support programmes (McKenzie 2021), especially in developing countries with large informal sectors.

Financial innovation in the age of digitisation

The classic microfinance model uses rigid repayments to help lenders screen clients, monitor loans, and ensure repayments. However, such rigidity may not suit businesses with high return but riskier investment profiles that may take longer to generate profits. This rigidity can push entrepreneurs toward safer, shorter-term projects rather than more productive investments that can generate broader private sector development. Evidence shows that contractual innovations that allow borrowers extra time to make repayments can improve outcomes for businesses by aligning repayment requirements more closely with firm cash flows, enabling entrepreneurs to better manage temporary income shocks (Barboni and Agarwal 2023, Battaglia et al. 2023). However, flexible-repayment credit contracts have sometimes led to increased microfinance institution default rates (Brune et al. 2022, Field et al. 2013, Afzal et al. 2024). Performance-based contracts can offer better risk-sharing and incentive alignment but are challenging in data-poor contexts with high monitoring and enforcement costs (Townsend 1979, Stiglitz and Weiss 1981, Udry 1994, Ligon et al. 2002).

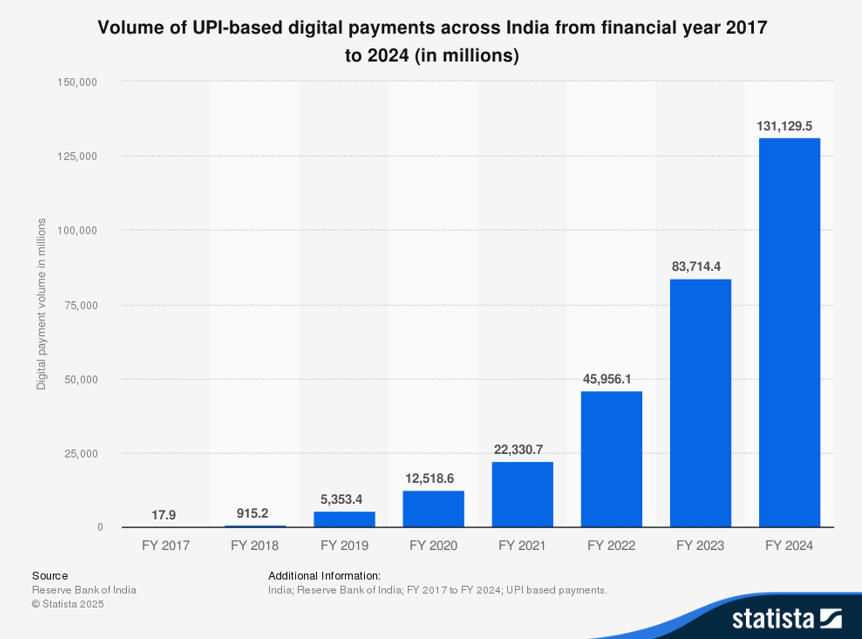

Rapidly expanding digital ecosystems open up new possibilities for enhancing financial inclusion and providing credit to previously underserved consumers and firms (Alok et al. 2024, Chioda et al. 2024). For instance, digital Unified Payments Interface (UPI) payments in India reached an astonishing 131 billion transactions in 2024, from only 17.9 million in 2017, mirroring trends in other low- and middle-income countries since COVID-19.

Figure 1: Volume of UPI-based digital payments across India from FY 2017 to 2024

Source: Keelery (2024).

By leveraging richer digital footprints, financial institutions can not only identify high-potential borrowers more effectively at the point of loan issuance, but they can also utilise high-frequency data after disbursing loans. This includes offering repayment terms that are better aligned with the underlying cash flows of the business and can encourage small firms to pursue more profitable investments, which I explore in Meki (2024).

Exploring equity-like innovations for small firms in developing countries

I investigate how ‘equity-like’ innovations, increasingly enabled by digital footprints, can improve outcomes for small firms. These contracts use performance-linked repayments, tying what borrowers owe to how well their business performs. Such contracts are similar to conventional equity finance in linking payments to performance, but they differ from conventional equity in that they do not involve taking a formal ownership stake in the business. While formal equity may offer additional benefits beyond the repayment structure, it remains challenging to implement in developing countries due to limited exit strategies and legal enforcement challenges (De Mel et al. 2019).

I assessed the effect of equity-like contracts on investment behaviour in Kenya and Pakistan with 765 small firm owners who were investing in fixed assets as part of two larger field experiments (Bari et al. 2024, Cordaro et al. 2025). Working closely with local institutions, I conducted ‘artefactual field experiments’, in which each entrepreneur made incentivised investment decisions under two types of contract: a standard fixed-repayment debt arrangement and an equity-like arrangement with performance-linked repayments. My objectives were to assess how equity-like contracts affected investment choices compared to debt, and how impacts varied with risk preferences, measured using incentivised activities. In those activities, I found that, on average, business owners exhibited a moderate level of risk aversion (suggesting they value insurance-like or risk-sharing mechanisms to mitigate income volatility), many were loss averse (placing greater weight on potential losses than on equivalent gains), and a substantial fraction overweighted low-probability events–a phenomenon also documented in high-income contexts with important implications for household finances and financial market asset pricing (Barberis and Huang 2008, Dimmock et al. 2021).

Equity-like contracts improved small firm investment in Kenya and Pakistan

1. Equity led to more profitable investment choices on average. In the investment games, small firm owners who were financed with equity chose more profitable investment options. This pattern, observed in both Kenya and Pakistan, aligns with previous research showing rigid repayments discourage riskier yet lucrative investments.

The standard economic framework for analysing decision-making in uncertain environments, Expected Utility Theory, assumes individuals rationally assess outcomes based on objective probabilities. However, Kahneman and Tversky (1979) highlights that people often exhibit behavioural biases, significantly affecting financial decisions. I incorporate these behavioural insights, exploring how equity and debt contracts impact small firm owners differently based on their individual risk preferences. I measure risk aversion, loss aversion, and overweighting of small probabilities using data from approximately 30,000 incentivised questions. Figure 2 illustrates key results on loss aversion and probability weighting.

Figure 2. Investment choice: Heterogeneity by risk preference

Notes: i) Each panel presents heterogeneous effects of the treatment (intervention), based on 3,060 observations from 765 unique business owners. ii) The dependent (outcome) variable is the expected profit of the investment option chosen by the business owner, with a ‘dummy’ for individuals with an above-median value for two distinct dimensions of risk preferences measured using incentivised activities at baseline: (1) loss aversion; (2) probability weighting. iii) In panel (1), ‘Equity*Loss-averse’ represents the expected profit of the investment option chosen by the most loss-averse business owners when financed with equity relative to the expected profit of the investment option chosen by the most loss-tolerant business owners under equity, and ‘Debt*Loss-averse’ represents the expected profit of the investment option chosen by the most loss-averse business owners when financed with debt relative to that chosen by the most loss-tolerant under debt. iv) The hypothesis tests whether individuals with higher risk preference are differentially affected by the equity and debt treatments. v) ‘p-values’ from a test of the null hypothesis that ‘Equity*Loss-averse = Debt*Loss-averse’ and ‘Equity*Overweighting = Debt*Overweighting’ are displayed in each panel.

2. Equity's advantage over debt is largest for risk-averse and loss-averse business owners. Equity was more impactful for the most risk-averse small firm owners, leading them to choose more profitable investment options than they would have under debt. This aligns with the idea that such individuals benefit from the insurance-like features of equity, which provide greater risk sharing than more rigid, fixed-repayment debt contracts.

Equity was also more impactful for loss-averse small firm owners, leading to more profitable investment options than they otherwise would have chosen under debt. Equity appeals to these individuals as it protects against downside risk—after a negative shock, required payments fall, reducing the chance of losing their existing assets—unlike under a more rigid debt contract. In return for that downside protection, these individuals are willing to share in the upside, making equity contracts especially well-suited for business owners who are more sensitive to losses than gains.

3. Debt outperforms equity for business owners who overweight small probabilities. Small firm owners who overweight small probabilities performed better under debt rather than equity. In skewed‐return environments that are common for firm return distributions (with a small chance of very high profits) such owners dislike equity as it forces them to share gains in those low-probability states they overweight. Consequently, these individuals tended to do better under fixed-repayment debt, which helps them avoid sharing those high profits.

Providing better-tailored financial products for small firms

Building on these results, I then explore a contractual innovation that can address this demand-side constraint to the uptake of equity-like contracts. I examine a ‘hybrid’ contract that combines features of both equity and debt contracts. Like equity, the hybrid contract reduces repayments when business revenues are low, offering valuable downside protection for risk- and loss-averse borrowers. At the same time, it caps repayments so that if a business experiences a rare, very high-profit outcome, repayments never go beyond a predefined cap (for example, twice the original loan principal). This design is particularly appealing to those who overweight small probabilities, as it avoids the need to share a disproportionately large portion of infrequent high profits. Field data from the Kenya study suggests hybrid features increase uptake among those preferring conventional debt to standard equity contracts without a capped upside.

In low-income countries, traditional lenders may find it particularly difficult to provide riskier products and longer-term financing (Choudhary and Limodio 2022). However, digitisation is lowering the cost of offering such tailored financial products. Hybrid contracts—designed to adjust repayment terms based on performance—are increasingly being used by innovative non-bank financial institutions such as payment fintechs (Russel et al. 2023). These contracts also share features with venture capital arrangements—such as equity clawbacks, performance ratchets, and convertibles—that align investor and business owner incentives through adaptable, outcome-based reward structures (Kaplan and Strömberg 2003).

More broadly, rapidly evolving digital ecosystems are transforming how financial services are delivered. Advanced data infrastructures and real-time monitoring tools enable lenders to assess business performance with greater precision and offer financing that better matches cash flow patterns. By harnessing these innovations, policymakers and financial institutions can develop more flexible financial solutions that both protect borrowers during downturns and encourage more productive investments to support small firm growth.

References

Afzal, U, G d’Adda, M Fafchamps, S Quinn, and F Said (2024), “Demand for commitment in credit and saving contracts: A field experiment”, Economic Journal, 134(664): 3063–3095.

Alok, S, P Ghosh, N Kulkarni, and M Puri (2024), “Open banking and digital payments: Implications for credit access”, Unpublished manuscript.

Banerjee, A, D Karlan, and J Zinman (2015), “Six randomized evaluations of microcredit: Introduction and further steps”, American Economic Journal: Applied Economics, 7(1): 1–21.

Barberis, N and M Huang (2008), “Stocks as lotteries: The implications of probability weighting for security prices”, American Economic Review, 98(5): 2066–2100.

Barboni, G and P Agarwal (2023), “How do flexible microfinance contracts improve repayment rates and business outcomes? Experimental evidence from India”, Unpublished manuscript.

Bari, F, K Malik, M Meki, and S Quinn (2024), “Asset-based microfinance for microenterprises: Evidence from Pakistan”, American Economic Review, 114(2): 534–574.

Battaglia, M, S Gulesci, and A Madestam (2023), “Repayment flexibility and risk taking: Experimental evidence from credit contracts”, Review of Economic Studies, 91(5): 2635–2675.

Beck, T, A Demirgüç-Kunt, and R Levine (2007), “Finance, inequality and the poor”, Journal of Economic Growth, 12(1): 27–49.

Brune, L, X Giné, and D Karlan (2022), “Give me a pass: Flexible credit for entrepreneurs in Colombia”, Unpublished manuscript.

Chioda, L, P Gertler, S Higgins, and P C Medina (2024), “FinTech lending to borrowers with no credit history”, Unpublished manuscript.

Choudhary, M A and N Limodio (2022), “Liquidity risk and long-term finance: Evidence from a natural experiment”, Review of Economic Studies, 89(3): 1278–1313.

Cordaro, F, M Fafchamps, C Mayer, M Meki, S Quinn, and K Roll (2025), “Finance and mutuality: Experimental evidence on credit with performance-contingent repayment”, Unpublished manuscript.

De Mel, S, D McKenzie, and C Woodruff (2008), “Returns to capital in microenterprises: Evidence from a field experiment”, Quarterly Journal of Economics, 123(4): 1329–1372.

De Mel, S, D McKenzie, and C Woodruff (2019), “Micro-equity for microenterprises”, World Bank.

Dimmock, S G, R Kouwenberg, O S Mitchell, and K Peijnenburg (2018), “Probability weighting and household portfolio choice: Empirical evidence”, Unpublished manuscript.

Field, E, R Pande, J Papp, and N Rigol (2013), “Does the classic microfinance model discourage entrepreneurship among the poor? Experimental evidence from India”, American Economic Review, 103(6): 2196–2226.

Fischer, G (2013), “Contract structure, risk-sharing, and investment choice”, Econometrica, 81(3): 883–939.

Kahneman, D and A Tversky (1979), “Prospect theory: An analysis of decisions under risk”, Econometrica, 47(2): 263–291.

Kaplan, S N and P Strömberg (2003), “Financial contracting theory meets the real world: An empirical analysis of venture capital contracts”, Review of Economic Studies, 70(2): 281–315.

Keelery, S (2024), “Volume of UPI digital payments across India FY 2017–2024”, Statista.

Ligon, E, J P Thomas, and T Worrall (2002), “Informal insurance arrangements with limited commitment: Theory and evidence from village economies”, Review of Economic Studies, 69(1): 209–244.

Liu, E M and B N Roth (2022), “Contractual restrictions and debt traps: Empirical evidence from a microfinance experiment”, Review of Financial Studies, 35(3): 1141–1182.

McKenzie, D (2021), “Small business training to improve management practices in developing countries: Re-assessing the evidence for ‘training doesn’t work’”, Oxford Review of Economic Policy, 37(2): 276–301.

Meki, M (2024), “Small firm investment under uncertainty: The role of equity finance”, Unpublished manuscript.

Russel, D, C Shi, and R Clarke (2024), “FinTech and financial frictions: The rise of revenue-based financing”, Unpublished manuscript.

Stiglitz, J E and A Weiss (1981), “Credit rationing in markets with imperfect information”, American Economic Review, 71(3): 393–410.

Townsend, R M (1979), “Optimal contracts and competitive markets with costly state verification”, Journal of Economic Theory, 21(2): 265–293.

Udry, C (1994), “Risk and insurance in a rural credit market: An empirical investigation in northern Nigeria”, Review of Economic Studies, 61(3): 495–526.