International capital flows can boost global growth and reduce inequality, but numerous geopolitical barriers distort where investment goes – often away from developing countries where it is most productive. Removing these barriers could increase global GDP by nearly 7%, substantially narrowing inequality between nations.

Editor’s note: For a broader synthesis of themes covered in this article, check out our VoxDevLit on Foreign Direct Investment.

International capital flows have long been an important and controversial topic within the policy debate on ‘globalisation and its discontents’ (Stiglitz 2002). A growing body of empirical research has highlighted how capital flows benefit both source and recipient countries by reducing financing costs, enhancing productivity and technological innovation, and allowing people to smooth consumption though borrowing and lending (Reinhardt et al. 2013, Kalemli-Özcan et al. 2013, Maggiori 2017, Bau and Matray 2023), while simultaneously showing that “these benefits of capital flows stem not only from FDI flows to non-financial sectors, but also from portfolio and debt flows” (IMF 2022). Such benefits could particularly accrue to developing countries, where capital is relatively scarce and labour relatively abundant. On the other hand, critics have stressed potential costs from more exposure to international capital, such as higher financial instability or tighter political constraints (Rodrik 2011) and have argued for a broader use of capital controls (Stiglitz and Ostry 2022).

In order to assess the benefits and costs of international investment, it is crucial to understand why capital moves from some countries to others in the first place. In recent years, advances in data collection and analysis have shed much new light on the empirics of international capital flows (Coppola et al. 2021, Florez-Orrego et al. 2024). And yet, numerous open questions remain about the determinants of global capital allocation, as cross-border investment flows display several patterns that we would not expect if they were frictionless and efficiently allocated. One major puzzle regarding international capital flows (the ‘Lucas puzzle’) is that, although capital is expected to yield higher returns where it is scarcer, flows from richer to poorer countries remain limited (Lucas 1990). More recently, the finding that international capital does not consistently move to countries with higher productivity growth has been called the ‘allocation puzzle’ (Gourinchas and Jeanne 2013). Related puzzles include the fact that people disproportionally invest in their own domestic assets (home bias) and the existence of large unexplained differences in countries’ rates of returns to capital (Monge-Naranjo et al. 2019).

Measuring barriers to international capital flows

In recent research (Pellegrino, Spolaore, and Wacziarg 2025), we have made progress on our understanding of global capital allocation and misallocation by developing and estimating a new quantitative model that does for international investment what economists have typically done for bilateral trade flows, using what are generally known as ‘gravity’ models. Like trade models, our model can factor in several frictions (barriers to international investment) that help account for anomalies in international investment data, such as the Lucas and home bias puzzles.

To measure and estimate these barriers to capital flows, we also created a new database on geographic, cultural, and linguistic distances between countries and of international taxation, available at geopoliticaldistance.org. This database includes information on over 100 countries.

Geopolitical distances distort international investment

We found that these measures of geographic, cultural, and linguistic distances across societies play a key role in explaining international investment patterns. Specifically, they explain why capital does not flow as much as it should to developing countries, despite capital being more productive in those economies, even when accounting for risk differences and other factors.

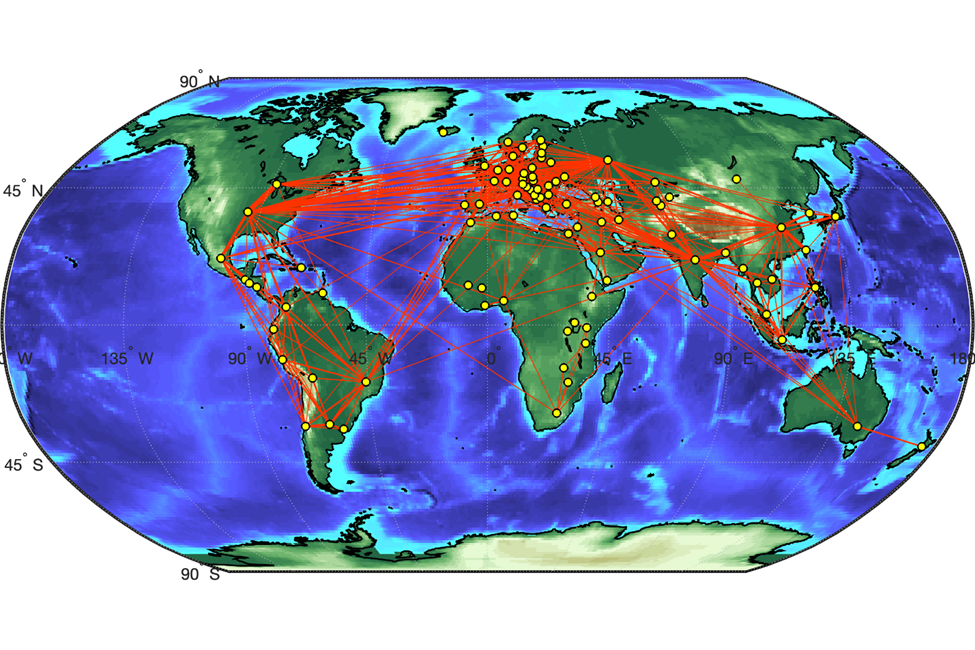

We find that geo-cultural distances across countries function as barriers to international investment. An investor who wants to invest in a country that is geographically distant, or where the language and culture are unfamiliar, or where taxation is higher, will require a higher rate of return. Therefore, countries that are less accessible (more peripheral) because of geography, culture, language, or that have higher taxation, tend to receive less capital and produce less income. Figure 1 shows the patterns of international investments predicted by our model, with a very dense network around the rich centre and much smaller flows towards the periphery.

Figure 1: Equilibrium spatial investment network

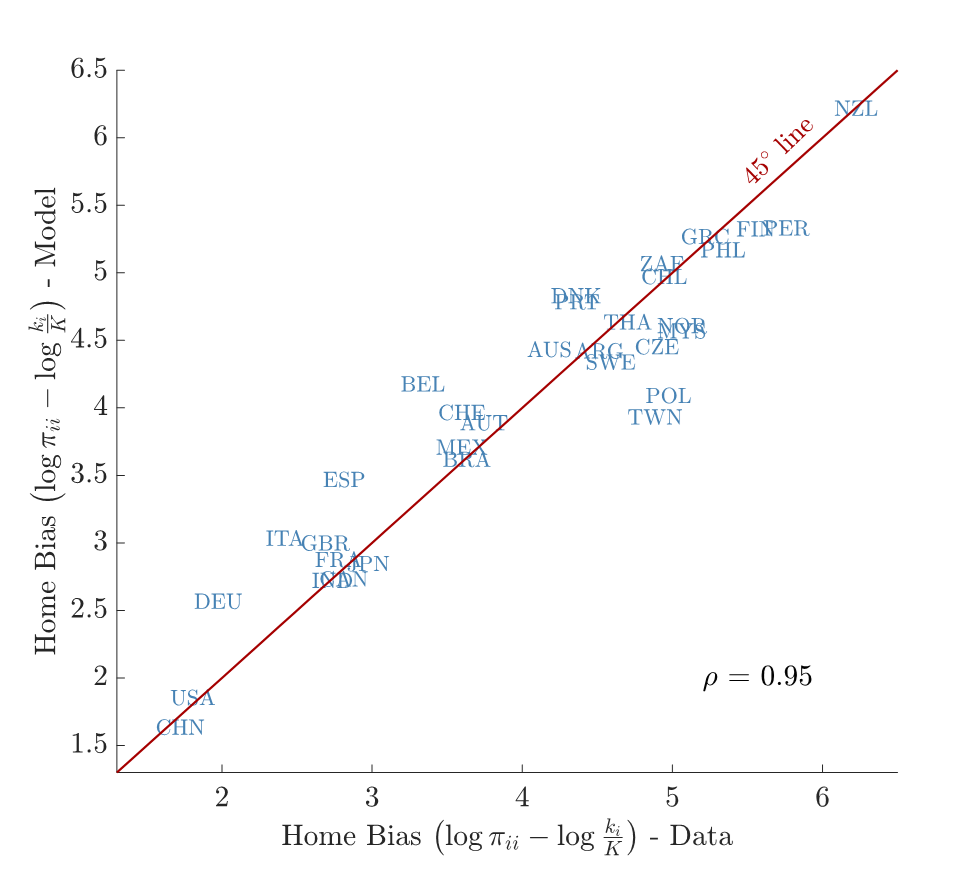

Our model can fit the data and explain existing anomalies with high accuracy. For example, it can match not only the overall level of home bias but also the specific values for individual countries. This is shown by the tight clustering of points along the 45-degree line in Figure 2. The fact that our model can reproduce the pattern of home bias so accurately for the vast majority of countries, even though we do not use any data on domestic investment in our empirical estimates, validates our approach to modelling global capital allocation.

Figure 2: Model fit–home bias (untargeted)

What would happen if barriers to international investment were removed?

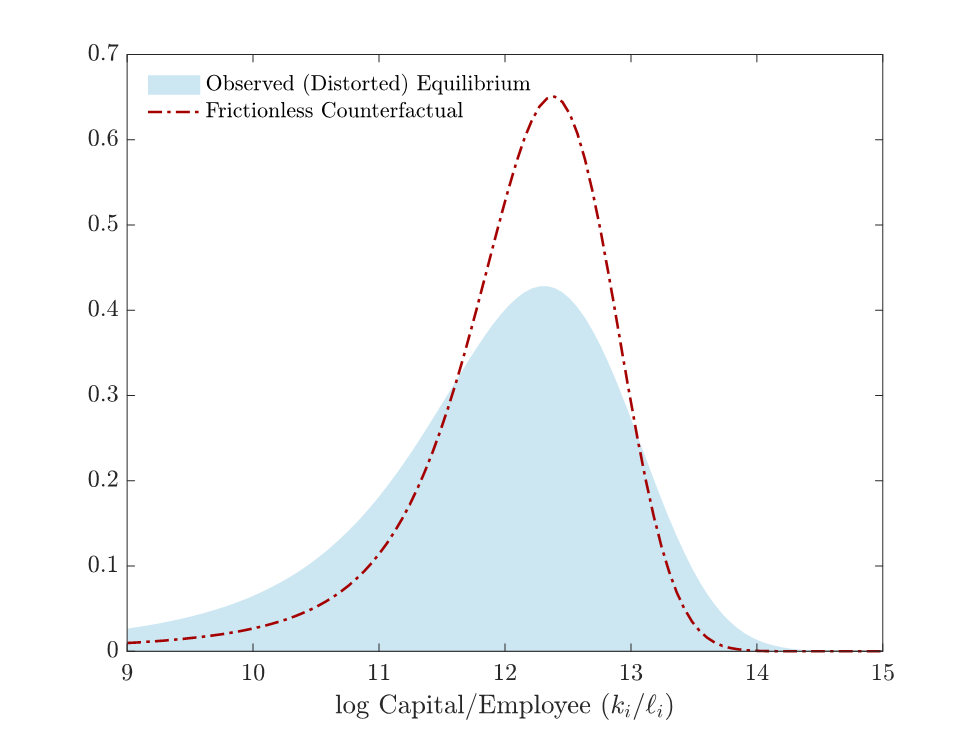

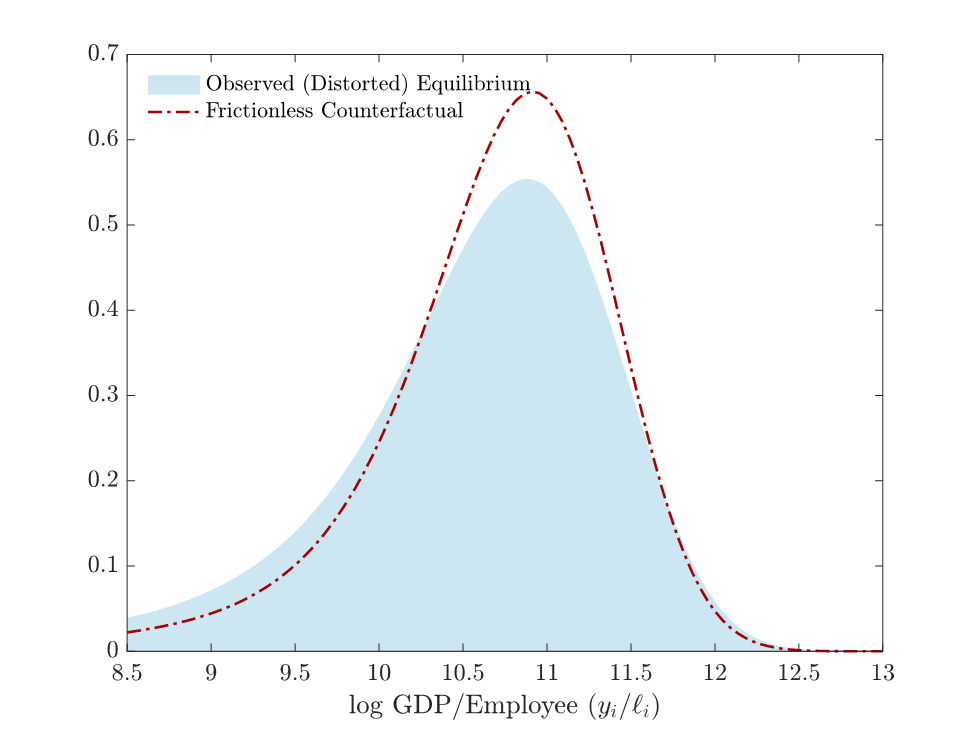

A central goal of our study is to understand the quantitative effects that barriers to global capital allocation have on global income and its distribution across countries. An informative way to address these questions is to ask what would happen if all those frictions were removed. We estimate that eliminating the barriers associated with geopolitical distance and taxation would boost global GDP by nearly 7%, a sizable efficiency gain. The effects on global inequality are even more striking: by removing barriers to international capital movements, we could eliminate a third of the dispersion in capital per worker across countries (a measure of inequality, see Figure 3) and almost a fifth of the dispersion in GDP per person across countries (Figure 4).

Figure 3: Distribution of capital per employee

Figure 4: Distribution of output per employee

Policy implications for international investment

Geo-cultural factors are major drivers of the global distribution of capital: they help make sense of many stylised facts about international investment that have long puzzled economists. These barriers matter greatly for global economic efficiency and the persistent gaps in wealth between countries. Therefore, our analysis sheds new light on global capital misallocation, which is especially relevant for the ongoing debate on the role of international investment in development. Our findings suggest that lack of capital investment is an important determinant of income differences across countries: numerous countries have struggled to attract investment, in spite of growing financial globalisation, as they are isolated from a geo-cultural perspective.

An open question is how to affect barriers associated with cultural and linguistic differences. These variables may be hard to change in the short term, as they result from long-term historical divergence between societies. And shrinking such differences may not be optimal, because cultural and linguistic diversity can also be beneficial, both in itself and for its effects on innovation and creativity. Hence, our view is that policies should not be aimed at reducing the distances themselves but should lower the effects of those distances on investment flows (the ‘betas’ in our gravity regressions). As these distances are likely to capture information frictions, it is possible in principle to reduce their effects by fostering effective exchanges of information and communication across different cultures and societies. Other factors highlighted in our analysis, such as tax policies and regulatory harmonisation, may also offer more immediate avenues for reform. More generally, our quantitative framework can provide a useful new tool for researchers and policymakers to assess the impact of different barriers to international investment, and to evaluate the positive and negative effects of various policy interventions, including capital taxation and capital controls.

References

Bau, N, and A Matray (2023), “Misallocation and capital market integration: Evidence from India,” Econometrica 91(1): 67–106.

Coppola, A, M Maggiori, B Neiman, and J Schreger (2021), “Redrawing the map of global capital flows: The role of cross-border financing and tax havens,” Quarterly Journal of Economics 136: 1499–1556.

Florez-Orrego, S, M Maggiori, J Schreger, Z Sun, and S Tinda (2024), “Global capital allocation,” Annual Review of Economics 16: 623–653.

Gourinchas, P-O and O Jeanne (2013), “Capital flows to developing countries: The allocation puzzle,” Review of Economic Studies 80(4): 1484–1515.

International Monetary Fund (IMF) (2022), “Capital flows and capital flow management measures – benefits and costs.”

Kalemli-Özcan, S, E Papaioannou, and J L Peydró (2013), “Financial regulation, financial globalization, and the synchronization of economic activity,” Journal of Finance 68(3): 1179–1228.

Lucas, R E (1990), “Why doesn’t capital flow from rich to poor countries?,” American Economic Review 80: 92–96.

Maggiori, M (2017), “Financial intermediation, international risk sharing, and reserve currencies,” American Economic Review 107(10): 3038–3071.

Monge-Naranjo, A, J M Sánchez, and R Santaeulàlia-Llopis (2019), “Natural resources and global misallocation,” American Economic Journal: Macroeconomics 11(2): 79–126.

Pellegrino, B, E Spolaore, and R Wacziarg (2025), “Barriers to global capital allocation,” Quarterly Journal of Economics, qjaf031.

Reinhardt, D, L Ricci, and T Tressel (2013), “International capital flows and development: Financial openness matters,” Journal of International Economics 91: 235–251.

Rodrik, D (2011), “The globalization paradox: Democracy and the future of the world economy,” W.W. Norton.

Stiglitz, J E (2002), “Globalization and its discontents,” W.W. Norton.

Stiglitz, J E and J D Ostry (2022), “The IMF is still behind the times on capital controls,” Project Syndicate.