Both sanctions and social norms reduced fare evasion at metro stations in Buenos Aires, but only the latter increased accountability-seeking. What does this mean for civic engagement in developing countries?

Editor’s note: For a broader synthesis of themes covered in this article, check out our VoxDevLit on Bureaucracy.

What are the ‘best’ policies to raise tax compliance?

Improving tax compliance and collecting more revenue has long been a core development priority for many low- and middle-income countries (LMICs). Particularly, in those LMICs where government expenditure represents less than 20% of GDP, which is far below the OECD country average of almost 50%.

To identify the most effective instruments for increasing compliance, several randomised control trials (RCTs) have been conducted recently, in which researchers collaborated with tax authorities to send letters with various messaging to taxpayers (Slemrod 2019, Ajzenman et al. 2025). These RCTs allow researchers to measure the relative effectiveness of two strategies to increase compliance: enforcement and social norms. Evidence suggests that enforcement messages are more effective at increasing compliance than messages appealing to social norms (Bergolo et al. 2023, Blumenthal et al. 2001, Castro and Scartascini 2015, Chirico et al. 2016, Fellner et al. 2013, Pomeranz 2015).

Though this evidence is useful for policymaking, it is likely insufficient as additional costs and benefits, beyond the partial equilibrium effect, need to be considered. One possibility is that paying taxes motivated by social norms yields additional social benefits—such as civic engagement—compared to paying taxes out of fear of fines. We test this hypothesis in recent research (Krakowski and Ronconi 2025).

Revisiting the ‘taxation produces representation’ hypothesis

Does paying taxes make citizens more likely to civically engage? Do the effects differ depending on the motives that produced tax compliance (i.e. enforcement or social norms)? Let’s start by revisiting the “Taxation-produces-representation” hypothesis, an influential narrative in political science and history, particularly in the UK (Carta Magna) and the USA (American Revolution). According to this hypothesis, paying taxes makes citizens more likely to demand representation (i.e. civic engagement) regardless of the strategy used by the government to raise revenues (Bates and Lien 1985).

Thus, a plausible justification for the partial equilibrium analysis is that the subsequent social effects are identical (or very similar) across compliance strategies. The amount of credible evidence testing whether taxation can stimulate political participation, however, is notoriously small (Paler 2013, Weigel 2020). We studied this using a novel field experiment.

Studying the impact of sanctions and social norms on fare evasion

We conducted a two-step field experiment at metro stations in Buenos Aires in 2021. In the first step, we exposed metro commuters to messages aimed at inducing them to pay the ticket. We placed a research assistant at the entry of the train station (that is, where passengers decide whether to pay or dodge the fare) wearing a t-shirt with the treatment message and handing out flyers with the same message (Figure 1). The messages reminded passengers that: (1) there is a fine for evading the ticket, and that (2) 90% of the passengers pay the ticket. The latter message was an estimation of the share of total passengers across public transport modes (i.e. bus, subway and metro) in Buenos Aires. (Note that compliance with the bus and subway fare is almost 100%).

Figure 1: Field experiment outside metro stations in Buenos Aires

Notes: These photographs show the research assistant at the entry of a train station delivering treatments.

In the second step, researchers interviewed passengers while waiting on the platform for the arrival of the train. They asked whether the passenger was willing to sign a petition demanding a guaranteed minimum level of public transport even during strikes. Signing the petition serves as our behavioural measure of respondents’ propensity to seek accountability.

The threat of sanctions was more effective at reducing fare evasion, but appealing to social norms had a meaningful effect on civic engagement

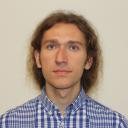

Only 31.5% of passengers in the control group paid for their tickets. While 43.7% and 36.9% of the ‘avoid fines’ and ‘90% passengers pay their tickets’ passengers paid their fare, respectively. This finding is consistent with previous research, which finds that the threat of fines is more effective at raising compliance than appeals to social norms.

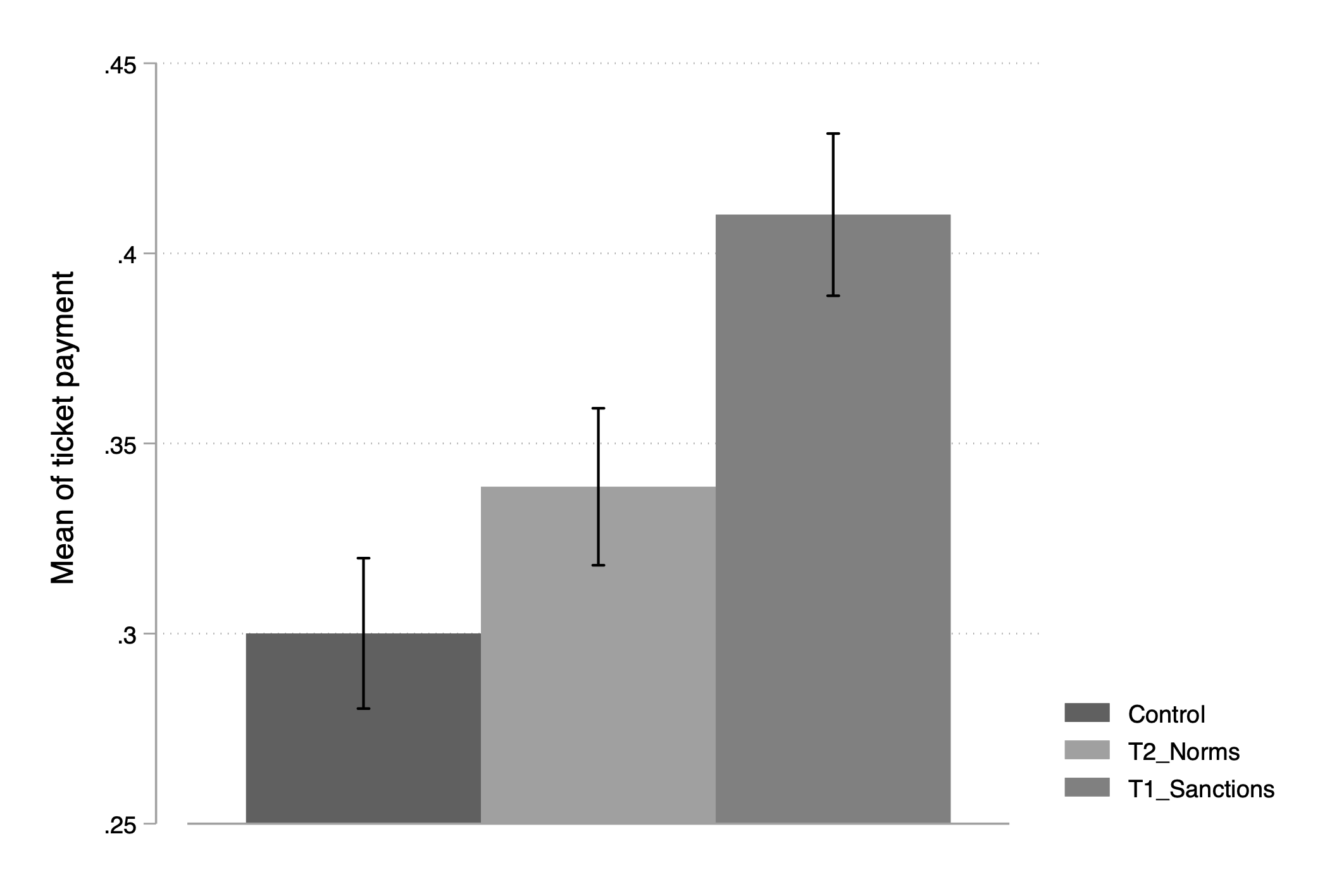

However, we also find that people who paid the fare, when motivated by the social norms treatment, were more likely to sign the petition compared to the control group. In contrast, we found no significant effect on civic engagement among those who paid the fare due to the threat of fines.

Figure 2: Ticket payment and signing petition by treatment

Notes: The figures show the means and the accompanying 95 confidence intervals of the indicated outcomes by the treatment assignment status. The outcome of the figure on the left is ticket payment, and the outcome of the figure on the right is signing the petition.

Homo economicus vs Homo reciprocant: How motivations for compliance impact civic accountability

Let’s assume that every person has two sides: one that is self-interested (homo economicus) and one cooperative (homo reciprocant). The self-interested side makes decisions through rational calculation, maximising personal benefit. In contrast, the cooperative side is motivated by a tendency to reciprocate prosocial behaviour, often extending beyond immediate self-interest; that is, they tend to cooperate when they observe others doing the same.

The ‘avoid fines’ treatment is expected to activate the self-interested side by priming concerns about sanctions, while the appeal to social norms likely engages the cooperative side. As a result, an increase in accountability-seeking behaviours related to compliance should only occur when compliance is motivated by a shared sense of fairness and trust in collective participation. When individuals view compliance as part of a broader social contract—where contributing to public goods is both a duty and a right—they are more likely to perceive accountability-seeking as a natural extension of their civic responsibilities. In contrast, when compliance is driven by the threat of fines, the self-interested side dominates. In this case, contributors are likely to perceive accountability-seeking as a classic collective action dilemma, where individual efforts appear irrational and free-riding becomes the preferred strategy.

The political economy of compliance

A common paradox in many LMICs is that, despite a pressing need for revenue, governments often intentionally refrain from collecting taxes or enforcing compliance. One explanation for this is that states purchase political stability by tolerating noncompliance, thereby undermining citizens’ ability to seek accountability (Dewey et al. 2021, Holland 2016). While we do not directly examine politicians’ behaviour, our findings suggest that increasing compliance—especially when motivated by appeals to social norms—increases citizens’ accountability-seeking behaviour.

This has important implications: politicians who fear being held accountable may have an incentive to discourage broad, norm-based compliance. Instead, it may be politically safer—and less costly—for them to rely on selective enforcement or even tacitly accept widespread noncompliance, thereby avoiding the civic empowerment that widespread, fairness-driven adherence to rules can foster.

Policy implications for civic engagement

Our research offers important implications for policymakers designing institutions to promote compliance and encourage citizens’ contributions to public goods. While the threat of sanctions may yield more immediate, targeted results, appealing to social norms has the potential to generate broader benefits across multiple areas of civic behaviours.

References

Ajzenman, N, M Ardanaz, G Cruces, G Feierherd, and I Lunghi (2025), “Unraveling the paradox of anticorruption messaging: Experimental evidence from a tax administration reform”, Inter-American Development Bank.

Bates, R and D Lien (1985), “A note on taxation, development, and representative government”, Politics & Society, 14(1): 53–70.

Bergolo, M, R Ceni, G Cruces, M Giaccobasso, and R Perez-Truglia (2023), “Tax audits as scarecrows: Evidence from a large-scale field experiment”, American Economic Journal: Economic Policy, 15(1): 110–153.

Blumenthal, M, C Christian, J Slemrod, and M G Smith (2001), “Do normative appeals affect tax compliance? Evidence from a controlled experiment in Minnesota”, National Tax Journal, 54(1): 125–138.

Castro, L and C Scartascini (2015), “Tax compliance and enforcement in the Pampas: Evidence from a field experiment”, Journal of Economic Behavior and Organization, 116: 65–82.

Chirico, M, R P Inman, C Loeffler, J MacDonald, and H Sieg (2016), “An experimental evaluation of notification strategies to increase property tax compliance: Free-riding in the city of brotherly love”, Tax Policy and the Economy, 30(1): 129–161.

Dewey, M, C Woll, and L Ronconi (2021), “The political economy of law enforcement”, MaxPo.

Fellner, G, R Sausgruber, and C Traxler (2013), “Testing enforcement strategies in the field: Legal threat, moral appeal and social information”, Journal of the European Economic Association, 11(3): 634–660.

Holland, A (2016), “Forbearance”, American Political Science Review, 110(2): 232–246.

Krakowski, K and L Ronconi (2025), “Compliance and accountability-seeking: Evidence from a field experiment in Argentina”, Journal of Development Economics, 103492.

Paler, L (2013), “Keeping the public purse: An experiment in windfalls, taxes, and the incentives to restrain government”, American Political Science Review, 107(4): 706–725.

Pomeranz, D (2015), “No taxation without information: Deterrence and self-enforcement in the value added tax”, American Economic Review, 105(8): 2539–2569.

Slemrod, J (2019), “Tax compliance and enforcement”, Journal of Economic Literature, 57(4): 904–954.

Weigel, J (2020), “The participation dividend of taxation: How citizens in Congo engage more with the state when it tries to tax them”, Quarterly Journal of Economics, 135(4): 1849–1903.