How does monetary policy transmit through developing economies? New evidence shows that firms do react to both monetary policy contraction and expansion, but not symmetrically.

Monetary policy is a cornerstone of economic management, yet its effectiveness in developing countries remains a subject of intense debate. Why does it seem to work in some contexts but not others? Three main explanations have emerged to account for the apparent weakness of monetary policy transmission in these economies:

- The lack of observed effects may simply reflect methodological limitations (Li et al. 2019). Traditional macroeconomic research relies on aggregate yearly indicators that often fail to capture the nuanced adjustments actors make in response to policy shifts.

- The impact of monetary policy may genuinely be weaker in developing economies due to structural constraints (Mishra et al. 2014). Shallow financial markets, excess liquidity in banking systems, or a lack of credibility can all dampen the transmission of policy signals to the real economy, making monetary tools less effective than in advanced economies.

- Monetary policy may only reveal its full effects under specific conditions, such as during periods of dramatic tightening when central banks aggressively raise interest rates to combat inflation (Abuka et al. 2019, Willems 2020). In these cases, the effects become more visible, but they often remain obscured during normal times or following modest policy adjustments.

To better understand how monetary policy shapes economic activity, we (Dramé and Léon 2025) adopted a novel approach. Rather than broadly asking whether monetary policy affects the economy, we focused on a more precise inquiry: “Do firm managers notice when monetary policy changes – and do they adjust their behaviour as a result?”

Combining high-frequency data with firm-level insights

To answer this question, we combined the World Bank’s Enterprise Surveys – which allowed us to track managers’ perceptions of credit access and their actual loan applications – with a manually collected database on policy events in developing countries.

Rather than relying on aggregate data, which could mask the responses of individual firms, we examined how firms react in real time to changes in monetary policy, providing a clearer picture of the mechanisms at play. More specifically, we examined how perceptions of credit constraints are shaped by monetary policy events in the days that follow, and how monetary policy influences borrowing decisions.

Firms react to both monetary policy contraction and expansion, but not symmetrically

Our findings confirm that firms do indeed react to monetary policy.

After a monetary contraction, managers quickly perceive credit as becoming more difficult to access. The effect is substantial: a 100-basis-point hike increases the likelihood that a manager will report credit constraints as a ‘serious obstacle’ by 12-19%. However, despite this shift in expectations, firms do not significantly reduce their loan applications. This suggests that while managers anticipate tighter credit conditions, they may not act immediately – perhaps because they have already secured financing or are waiting to see how conditions evolve.

The response to monetary easing is even more intriguing. Managers adjust their perceptions less dramatically after a rate cut, but their behaviour changes more noticeably: loan applications increase by 17%. This asymmetry indicates that firms may wait for confirmation that banks are actually easing lending standards before they act. It also highlights a potential limitation in our data: annual credit application figures may miss short-term timing effects, such as firms applying for loans early in the year before a rate hike fully materialises.

Not all firms (or countries) react the same way

The effectiveness of monetary policy depends heavily on who you are and where you operate.

At the firm level, we found that companies with prior bank relationships are less sensitive to policy changes. These firms often have alternative funding sources, such as existing credit lines or internal cash reserves, which insulate them from the immediate effects of monetary tightening or easing. Similarly, foreign-owned firms react less to local monetary policy, likely because they rely on financing from parent companies rather than domestic banks. Surprisingly, firm size and age do not play a significant role, suggesting that access to credit – rather than firm characteristics – drives sensitivity to monetary policy.

At the country level, our findings align with and extend the existing evidence base. Monetary policy is most effective when:

- Central banks are more credible, particularly under inflation-targeting regimes and when they are independent.

- The excess liquidity in the banking systems impedes transmission of monetary policy.

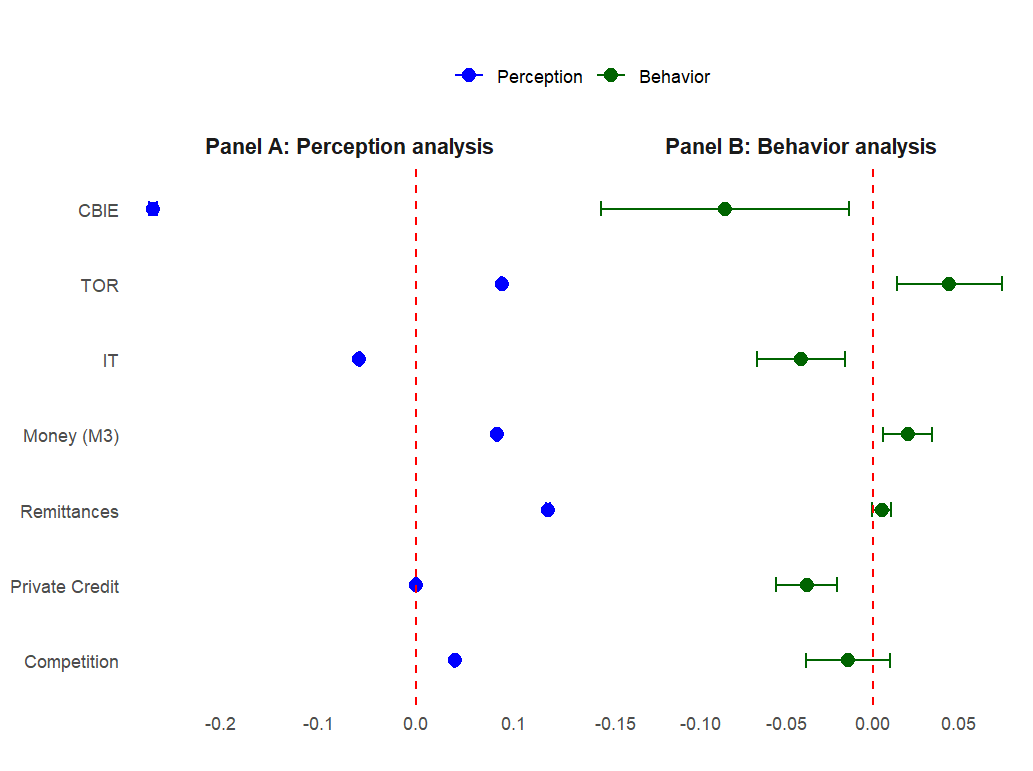

However, we found no robust effect from other commonly cited factors, such as banking depth or competition (see Figure 1). This suggests that while deeper financial markets and competitive banking sectors are often assumed to enhance monetary policy transmission, their actual impact may be more limited than previously thought.

Figure 1: The effectiveness of monetary policy based on country characteristics

Note: The figure displays estimates from a triple-difference model (Post × ∆(IR) × Z, where Post is a dummy variable equal to 1 if the firm was surveyed after the event, ∆(IR) is the change in the key policy rate, and Z represents the country characteristics). The dependent variable is the manager's perception of access to finance as an obstacle in Panel A and a dummy equal to 1 if the firm applied for a loan in the year before the survey in Panel B. Z represents the central bank independence index (CBIE), turnover rate of central bank governors (TOR – decrease with higher independence), inflation targeting dummy (IT), cyclical component of broad money M3 to GDP (Money (M3)), remittance inflows to GDP (Remittances), private credit to GDP (Private Credit), and assets of the five largest banks (Competition). Dots indicate coefficient estimates representing the effect of a 100-basis point hike in the policy rate, and vertical lines are 95% confidence intervals.

Implications for monetary policy in developing countries

Our research offers three key lessons for policymakers.

- Monetary policy in developing countries is not broken – it’s complex. Firms do react, but the effects depend on their characteristics and where they operate.

- Policymakers should focus on the plumbing of the financial system. Excess liquidity can dull the transmission of monetary policy; therefore, tools such as dynamic reserve requirements or liquidity absorption operations may help. Additionally, protecting central bank independence from political interference is critical to maintaining credible policy signals.

- Do not overlook firm-level heterogeneity. Firms without bank relationships are the most sensitive to policy changes yet the least able to adapt.

Research implications: Reconstructing high-frequency data for developing countries

One of the most significant contributions of our study is demonstrating how researchers can reconstruct high-frequency data – a method often used to assess policy effects in industrialised countries – using survey data from developing economies. This approach allows us to detect hidden patterns that traditional macro-level studies might miss.

By leveraging firm-level surveys and real-time policy events, we show that the toolkit for understanding monetary policy in developing countries is more powerful than previously thought. As researchers continue to refine these methods, we can expect even deeper insights into how short-term policy interventions shape economic outcomes in low- and middle-income economies.

References

Abuka, C, R K Alinda, C Minoiu, J-L Peydró, and A F Presbitero (2019), “Monetary policy and bank lending in developing countries: Loan applications, rates, and real effects,” Journal of Development Economics 139: 185–202.

Dramé, D, and F Léon (2025), “Do firms react to monetary policy in developing countries?,” European Economic Review 105102.

Li, B G, C Adam, A Berg, P Montiel, and S O’Connell (2019), “Structural VARs and the monetary transmission mechanisms in low-income African countries,” Journal of African Economies 28(4): 455–478.

Mishra, P, P Montiel, P Pedroni, and A Spilimbergo (2014), “Monetary policy and bank lending rates in low-income countries: Heterogeneous panel estimates,” Journal of Development Economics 111: 117–131.

Willems, T (2020), “What do monetary contractions do? Evidence from large tightenings,” Review of Economic Dynamics 38: 41–58.