Pakistan’s tax system shows that even with extensive withholding and VAT-based reporting, weak documentation and limited enforcement capacity – exacerbated by political resistance – undermine revenue collection, highlighting the need to strengthen both information and enforcement channels.

Editor’s note: This article is part of a series of posts reflecting on how the evidence from VoxDevLits applies to specific contexts. This post explores how evidence on Taxation relates to Pakistan.

Pakistan’s struggle to raise tax revenues is often framed as a problem of weak enforcement. Yet the country already has one of the broadest withholding regimes in the developing world: employers, banks, and utility companies are legally obliged to deduct and remit taxes on behalf of clients and employees. Withholding taxes make up nearly half of all direct taxes in Pakistan while VAT makes up nearly 45% of all tax revenue (FBR 2024), with both constituting main sources of third-party information. Despite this, 60 to 70% of potential revenue is still lost to evasion (Waseem 2017).

This gap between the promise and performance of third-party data points to a deeper issue. Effective enforcement through third-party reporting is not just a question of whether tax administrations use that information; it depends on whether information is reliably generated in the taxpayer’s value chain, and whether the state has the capacity and political space to use it for enforcement. Pakistan’s recent experience highlights the fragility of both these conditions.

Third-party reporting and tax withholding in Pakistan

Third-party reporting is essential to enforcing tax compliance (Jensen et al. 2024). Evidence from high-income contexts shows that when income is subject to independent reporting by employers or banks, compliance is nearly perfect (Kleven et al. 2011). Value-added tax, now used in most low- and middle-income countries, generates a built-in paper trail: sellers report their sales, buyers report their purchases, and discrepancies reveal evasion (Pomeranz 2015).

However, third-party reporting has its limitations. At the final consumer stage, where buyers have little incentive to demand receipts, the trail often breaks down (Naritomi 2019). Firms may also adjust margins that are harder to verify: when confronted with discrepancies in reported revenues, they may inflate unverifiable costs instead (Carrillo et al. 2017). Even where information trails exist, weak administrative capacity can blunt their impact. For example, in Uganda, sellers and buyers reported different values for the same transaction in nearly four-fifths of cases, with little consequence (Brockmeyer et al. 2024).

A related strand of evidence shows why withholding is particularly effective in developing countries. By delegating collection directly to third parties, governments can raise compliance without relying on their own limited enforcement capacity. In Costa Rica, higher withholding rates raised effective collections both because firms did not reclaim withheld taxes and because they perceived enforcement to have become stricter (Brockmeyer and Hernandez 2022). In Argentina, appointing large firms as collection agents increased compliance among their trading partners (Garriga and Tortarolo 2024).

Why paper trails break down in Pakistan

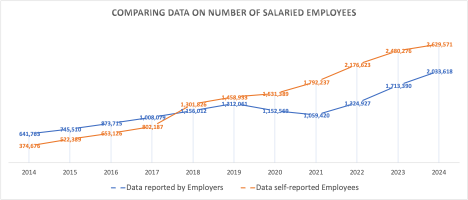

Figure 1: Number of employees according to employers and employees

Note: Data sourced from PRAL using administrative tax return declarations.

In Pakistan, the challenge of third-party reporting begins well before enforcement. Large parts of the economy are undocumented, and firms and consumers have little incentive to keep records. So, the first question is whether reliable third-party information, such as data from withholding statements and value chains, is even being generated.

Even in the case of salaries, employer and employee reports diverge, suggesting evasion (Figure 1). Such discrepancies raise doubts about the accuracy of employer-reported withholding data on other revenue streams as well. Similar issues are evident in retail transactions as most retailers prefer not to issue receipts, and consumers rarely demand them. Without consumer pressure, the paper trail breaks down at the very last mile of the value chain, if not earlier. These issues of inconsistent and fragmented information flows exist in other sectors as well.

More recently, Pakistan has started enforcing reliable consumer-facing mechanisms such as point-of-sale (POS) devices, which yielded a 22% increase in the volume of reported sales from June 2024 to June 2025.[1] However, this is sensitive to physical enforcement such as random physical checks conducted by FBR officials ensuring POS machines are not disconnected.

Where documentation does exist, its quality is uneven; invoices may be handwritten, incomplete, or designed in ways that make cross-checking difficult. Record-keeping obligations exist in law but are not consistently enforced in practice, especially for small and medium-sized enterprises. This creates a patchwork of partial information that cannot easily be harnessed for technology-assisted enforcement.

Such challenges necessitate the use of human resources to enforce legal record-keeping obligations. However, in addition to limited capacity, the use of in-person enforcement efforts is met with a completely different set of political economy challenges.

Pakistan, along with other low- and middle-income countries, sits at an earlier stage of the third-party reporting ‘chain’ than the global evidence benchmarks. While research focuses on how tax authorities can use available third-party information, countries like Pakistan struggle to ensure that such information is first generated, let alone transmitted through the taxpayer’s value chain and documented in a verifiable form.

Although Pakistan is increasingly using technology for detection and compliance – as per Okunogbe and Tourek (2024) – unless challenges of data availability and quality are addressed, even the most advanced digital tools will fail to deliver the desired compliance gains witnessed elsewhere.

Why stronger laws don’t always mean stronger enforcement

Beyond generating useable data, Pakistan faces a second set of hurdles: transforming that data into actual revenue. Here, two distinct constraints deserve attention: first, the legal authority of the tax administration, and second, its operational capacity.

Legal authority: The law on books

Generally, it is assumed that once the laws are passed, tax authorities can act on available information. In Pakistan, the legal framework itself is contested terrain. Efforts to strengthen the enforcement arm of the FBR often meet resistance from powerful business groups and political lobbies (Bukhari et al. 2025).

A recent example is the Finance Act of 2025, which endeavoured to strengthen existing provisions for the prevention of tax fraud. Although Parliament passed the legislation, business associations mounted a sustained campaign against these powers (Khan 2025), forcing extensive negotiations before limited implementation – conditional on intense administrative oversight – became possible. This shows how enforcement efforts can be weakened even after laws are passed due to political pushback, highlighting the prevalence of mistrust between the public and government (Alm and Zehra 2024) that hinders compliance.

Operational capacity: The law in action

Even when the FBR has legal authority, converting laws into effective enforcement is constrained by limited human and technical resources. The FBR cannot place officials at every production site, audit every return, or verify every invoice. Instead, it is considered optimal to focus on one or two ‘key players’ in a value chain, with the assumption that ensuring compliance at these nodes will permeate compliance throughout the value chain. However, this does little to fix the evasion problem if industries adapt by moving evasion to other points of the chain or lobby to have monitoring removed altogether.

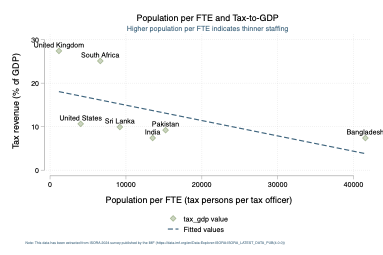

Figure 2: Population of tax persons by tax officials

Notes: All data has been sourced from ISORA except for data on Bangladesh’s GDP (CEIC n.d.), Pakistan’s tax-to-GDP ratios (Ministry of Finance 2023); and South Africa’s tax statistics (National Treasury and SARS 2023).

Furthermore, given that Pakistan has one of the highest taxpayer-to-officer ratios (Figure 2), assigning officers to physical enforcement activities compromises the number and efficiency of formal audits, thereby undermining tax revenues.

Finally, enforcement capacity is shaped by perceptions. If taxpayers believe the administration cannot act consistently or will eventually back down under pressure, deterrence is blunted (Best et al. 2021). The frequent cycle of enforcement drives followed by negotiated retreats sends the signal that compliance is optional. Together, this reinforces that enforcement depends not only on the actual probability of detection but also on the perceived credibility of enforcement (Jensen et al. 2024).

Key takeaways

Pakistan’s constraints are not only technical but political. Laws can be passed and data collected, yet both can be neutralised, either through lobbying that weakens enforcement powers or capacity gaps that limit enforcement. In practice, this means third-party reporting cannot achieve its intended effect unless the state simultaneously strengthens its legal authority, protects that authority from dilution, and builds the operational depth to act on information at scale.

The two-chain framework and lessons for tax policy

Pakistan’s experience illustrates that third-party reporting depends on the interaction of two parallel chains. The information chain, existing between suppliers, producers, retailers and consumers, determines whether data on economic transactions is documented and transmitted in a way that is verifiable. And the political economy chain, which exists between the law, state institutions, and political stakeholders, that determines whether the state has the authority to act on that data. Weakness in either chain – data without enforcement or enforcement without data – undermines compliance.

The lesson here is that for third-party reporting to yield significant revenue gains, both chains need to remain strong and should mutually reinforce each other. Policies must generate reliable data and build trust, so enforcement powers are credible and consistently applied. For countries like Pakistan, a bridge between these two chains will ensure a credible self-reinforced system of enforcement and compliance.

References

Alm, J, and Z Farooq (2024), “Increasing tax collections by local governments in developing countries by improving tax compliance,” International Center for Public Policy Working Paper.

Best, M, J Shah, and M Waseem (2021), “Detection without deterrence: Long-run effects of tax audit on firm behavior.”

Brockmeyer, A, and M Hernandez (2022), “Taxation, information and withholding: Evidence from Costa Rica,” World Bank.

Brockmeyer, A, G Mascagni, V Nair, M Waseem, and M Almunia (2024), “Does the value-added tax add value? Lessons using administrative data from a diverse set of countries,” Journal of Economic Perspectives 38(1): 107–132.

Bukhari, H, I Haq, and A R Shakoori (2025), “Tax laws (Amendment) Ordinance, 2025: Ill-advised, confiscatory & undemocratic,” Business Recorder.

Carrillo, P, D Pomeranz, and M Singhal (2017), “Dodging the taxman: Firm misreporting and limits to tax enforcement,” American Economic Journal: Applied Economics 9(2): 144–164.

CEIC (n.d.), “Bangladesh tax revenue: % of GDP.”

Federal Board of Revenue (FBR) (2024), “Yearbook 2023–24,” Government of Pakistan.

Garriga, P, and D Tortarolo (2024), “Firms as tax collectors,” Journal of Public Economics 233(C).

Jensen, A, A Brockmeyer, and L Gadenne (2024), “Taxation and development,” VoxDevLit 12(1).

Khan, A F (2025), “Trade associations reject ‘draconian’ powers for FBR,” Dawn.

Kleven, H J, M B Knudsen, C T Kreiner, S Pedersen, and E Saez (2011), “Unwilling or unable to cheat? Evidence from a tax audit experiment in Denmark,” Econometrica 79(3): 651–692.

Ministry of Finance, Government of Pakistan (2023), “Pakistan: Summary of consolidated federal and provincial fiscal operations, 2022-23.”

Naritomi, J (2019), “Consumers as tax auditors,” American Economic Review 109(9): 3031–3072.

National Treasury and South African Revenue Service (SARS) (2023), “Tax statistics 2023.”

Okunogbe, O, and G Tourek (2024), “How can lower-income countries collect more taxes? The role of technology, tax agents, and politics,” Journal of Economic Perspectives 38(1): 81–106.

Pomeranz, D (2015), “No taxation without information: Deterrence and self-enforcement in the value added tax,” American Economic Review 105(8): 2539–2569.

Waseem, M (2017), “Using movement of exemption cutoff to estimate tax evasion: Evidence from Pakistan,” Proceedings Annual Conference on Taxation and Minutes of the Annual Meeting of the National Tax Association 109: 1–57.