Combining monthly data for 96 economies with a geophysical dataset of more than 44,000 earthquakes from 2012–2023, our analysis uncovers a stark asymmetry: major earthquakes raise sovereign spreads only in countries with low administrative and fiscal capacity, while spreads remain unchanged – or even fall slightly – in high-capacity states. The spread response emerges with a delay of one to two months, consistent with investors pricing not the physical shock itself but what it reveals about a government’s ability to manage its fiscal and administrative aftermath. These findings highlight that state capacity functions as a form of sovereign insurance, and that incorporating institutional quality into sovereign-risk assessments could improve the evaluation of vulnerability to natural and climate-related shocks.

Earthquakes are among the easiest shocks for macroeconomists to study. They arrive without warning, are unrelated to a country’s economic policies or political cycles and follow the logic of tectonic plates rather than financial markets or fiscal authorities. Yet their consequences place immediate and visible demands on the state (see Eickmeier et al. 2024, Keiller and van Reenen 2024). This combination of exogeneity and institutional stress makes earthquakes an unusually powerful setting for studying how investors perceive sovereign resilience. In our research, we use earthquakes as a quasi-natural experiment to examine how emerging-market sovereign bond spreads respond when the ground literally shifts beneath a country’s feet.

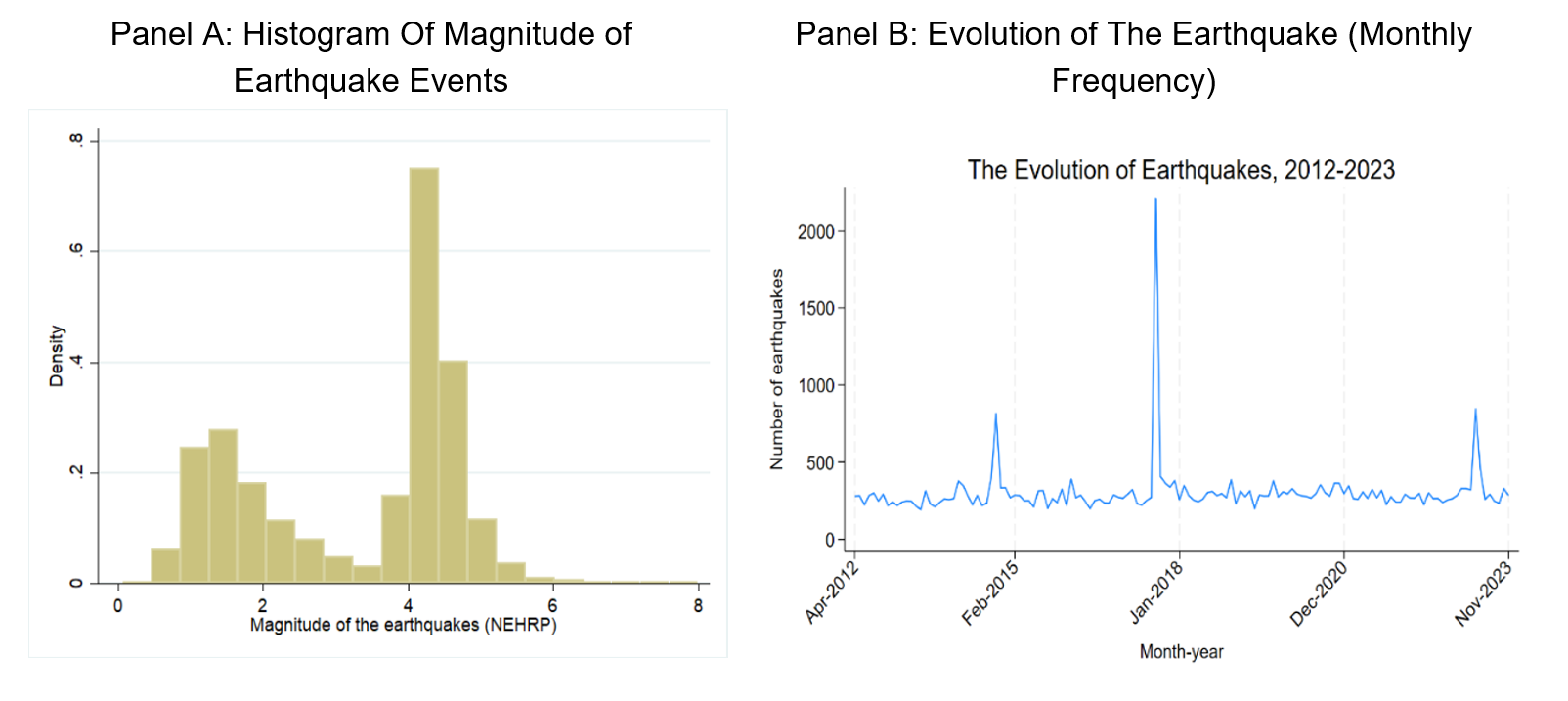

Figure 1. Earthquake evolution and magnitude histogram

Sovereign spreads react differently

Our central finding is straightforward but carries wide implications. Earthquakes do not generate a uniform sovereign spread response. Instead, they serve as a revealing test of state capacity. In countries with low institutional capacity, sovereign spreads rise sharply and persistently after a major earthquake. In countries with strong capacity, spreads do not rise at all, and in some cases, they even fall. Identical natural disasters elicit fundamentally different financial reactions depending on the quality of institutions that must respond.

To investigate these dynamics, we construct a monthly panel of 96 emerging and developing economies from 2012 to 2023, merging sovereign bond spreads with a detailed seismic dataset comprising more than 44,000 earthquake events. We link these shocks to long-run measures of state capacity and employ modern empirical techniques, heterogeneity-robust difference-in-differences (Sun and Abraham 2021, de Chaisemartin and d’Haultfoeuille 2020) and local-projection DiD estimators (Dube et al. 2023) to capture dynamic, heterogeneous effects.

The first empirical result is that earthquakes do affect spreads on average, but not immediately, and not dramatically. Markets wait. The spread response becomes visible only after one to two months, corresponding to the period when the fiscal consequences of the disaster become clearer. This delay suggests that investors are not pricing the physical event itself. They are pricing what the event reveals about the sovereign’s ability to manage fiscal pressures, mobilise administrative capacity, and coordinate emergency responses.

Earthquakes in low- vs high-capacity states

Once we allow for institutional heterogeneity, the picture becomes sharper. In low-capacity states, defined using long-run measures of administrative effectiveness, fiscal capability and bureaucratic quality, spreads rise significantly. These increases persist for several months, suggesting a sustained reassessment of sovereign risk. Earthquakes appear to expose institutional fragility, prompting markets to expect slower recovery, weaker revenue mobilisation, or potential fiscal slippages.

In contrast, high-capacity states exhibit no such spread increase. In fact, in several cases we observe mild reductions in spreads after earthquakes. This counterintuitive result becomes clearer when viewed through the lens of investor expectations. States with greater administrative capability coordinate responses more effectively, communicate more credibly, and access external financing swiftly. Rather than signaling elevated fiscal risk, the shock demonstrates the state’s ability to cope. In this reading, the earthquake becomes not a source of fragility but a visible test of resilience, one that some states pass.

The response is non-linear as well. Smaller tremors, those occurring frequently but with limited destructive potential, do not move markets. Only larger earthquakes, located in the upper tail of the magnitude distribution, trigger meaningful financial reactions. This threshold effect aligns with the institutional interpretation. Minor shocks impose minimal administrative demands, while major events test the entire system. Markets react only when institutional capability is genuinely on display.

We further examine whether predictability plays a role. Some regions experience seasonal or clustered seismic patterns, raising the possibility that markets might anticipate certain shocks. To address this, we extract unanticipated earthquake shocks by removing predictable components using autoregressive and seasonal filters. The core results remain robust. It is not the surprise element of the earthquake that drives sovereign spread movements; it is how the state manages the fallout.

Understanding sovereign risk in a changing world

These findings carry several implications for understanding sovereign risk in a world where climate- and disaster-related shocks are becoming more frequent. First, they highlight that state capacity is a central determinant of financial resilience. The ability to mobilise resources, coordinate agencies, and implement policy does more than improve long-run development outcomes, it directly shapes how markets price sovereign debt in the aftermath of shocks. Institutional quality functions as a form of sovereign insurance.

Second, the results suggest that standard sovereign-risk frameworks, which emphasise fiscal balances, debt ratios and macroeconomic fundamentals, may overlook an important dimension. Two countries with similar debt burdens may experience the same shock differently if one possesses a capable administrative apparatus and the other does not. Incorporating measures of institutional robustness into sovereign analysis could therefore improve the predictive accuracy of debt sustainability assessments.

Third, the findings speak to the design of international support. Post-disaster financing remains essential, but the effectiveness of such support depends heavily on domestic institutional capability. Investments in public financial management, emergency response systems, and administrative coordination generate lasting returns by strengthening a country’s ability to withstand and absorb shocks. The long-run dividends include not only more effective disaster response but also lower sovereign risk premia.

Finally, the results speak to a broader political economy question. How shocks shape the perceived credibility of the state. In low-capacity states, earthquakes may become focal events that reveal institutional weaknesses and deepen investor concern. In higher-capacity states, the same events provide a demonstration effect that reinforces confidence in governance. Shocks interact with institutions, rather than operating independently of them.

The overarching message that emerges from our analysis is simple. Earthquakes do not create sovereign fragility; they reveal it. They shake the ground everywhere, but they move sovereign bond markets only where institutional foundations are already brittle. As climate-related and natural shocks become more frequent, this asymmetry will matter more, not less. For countries seeking to strengthen fiscal and financial resilience, building state capacity is not a secondary priority. It is a central part of sovereign risk management.

References

Arezki, R, P A Imam, K Kpodar, and D Le-Van (2025), Earthquakes and Emerging Market Sovereign Bond Spreads, IMF Working Paper WP/25/218, IMF, Washington, DC.

de Chaisemartin, C and X d’Haultfoeuille (2020), “Two-way fixed effects estimators with heterogeneous treatment effects”, American Economic Review 110(9): 2964–2996.

Dube, A, B Horn, and Y Kamada (2023), “Local projections, difference-in-differences, and staggered adoption designs”, NBER Working Paper 31265.

Eickmeier, S, J Quast, and Y Schüler (2024), “Large, broad-based macroeconomic and financial effects of natural disasters”, VoxEU.org, 26 May, https://cepr.org/voxeu/columns/large-broad-based-macroeconomic-and-financial-effects-natural-disasters

Keiller, A N and J Van Reenen (2024), “Managing to cope with natural disasters”, VoxEU.org, 8 August, https://cepr.org/voxeu/columns/managing-cope-natural-disasters

Sun, L and S Abraham (2021), “Estimating dynamic treatment effects in event studies with heterogeneous treatment effects”, Journal of Econometrics 225(2): 175–199.