In Andhra Pradesh, credit contraction in the rural economy, triggered by microfinance regulation, lowered educational investments and caused lasting learning losses, with larger effects for girls and younger children.

Editor’s note: For a broader synthesis of themes covered in this article, check out Issue 3 of our VoxDevLit on Microfinance.

Over the last few decades, microfinance has grown into one of the most prominent tools in the development policy toolkit, reaching hundreds of millions of low-income households across the developing world. Policymakers have come to value it for its dual role: as a source of liquidity that enables poor households to undertake productive activities, invest in businesses, and build livelihoods, and as a form of implicit insurance that helps families smooth consumption and buffer against income shocks (Karlan and Zinman 2011, Cai et al. 2025). Yet despite its scale and policy prominence, evidence on its impact remains mixed – with most studies finding modest income effects and limited influence on broader welfare outcomes such as education or health (Attanasio et al. 2015, Banerjee et al. 2015, Tarozzi et al. 2015).

But most of this research has focused on what happens when credit is expanded. Less is known about what happens when credit is withdrawn, and whether the costs of losing credit mirror the benefits of gaining it. In Kalliyil and Sahoo (2026), we examine this question using a regulatory shock in India to study how a policy-induced credit contraction affected children’s human capital formation.

A crisis that crossed state lines

On 15 October 2010, the government of Andhra Pradesh – then the heartland of India's microfinance industry – enacted an emergency ordinance that effectively halted all microfinance operations in the state. The ordinance restricted disbursements and collections, capped interest rates, and required microfinance institutions (MFIs) to obtain local government approval before resuming operations. Its stated purpose was borrower protection: in the months prior, a wave of suicides among rural borrowers had received extensive media coverage, with many cases linked to over-indebtedness and aggressive loan recovery by MFIs (The Economic Times 2010, The Hindu 2010).

But the regulation was controversial. Critics argued that the government used MFIs as a visible target while deeper agrarian distress and farmer suicides reflected broader economic conditions. Others pointed to political self-interest: by weakening private microfinance, the government could strengthen its own state-sponsored self-help group lending programmes while appealing to indebted rural voters (Rai 2010, Roodman 2010, Sriram 2012). Whether driven by genuine consumer protection, political convenience, or institutional rivalry – or some combination of all three – the ordinance had immediate and far-reaching consequences.

Within Andhra Pradesh, the ordinance disrupted MFI operations and led to near-total borrower defaults. The effects were not confined to Andhra Pradesh. Breza and Kinnan (2021) show that the Andhra Pradesh crisis reduced microfinance credit outside the state through lenders’ exposure to Andhra Pradesh, and that this contraction affected rural livelihoods, including wages, earnings, and consumption. Between 2010 and 2011, India’s aggregate microfinance loan portfolio fell by around 20%, a decline of more than one billion US dollars.

Our research asks whether this credit contraction also affected children’s human capital. To answer this, we compare districts outside Andhra Pradesh that differed in their exposure to the crisis. Districts were more exposed when a larger share of their local MFI lending came from lenders with greater exposure to Andhra Pradesh before the crisis. Exposure was shaped by pre-existing lender networks rather than by local economic conditions, household demand for education, or borrower behaviour outside Andhra Pradesh. We use this variation to study how the credit contraction affected household livelihoods, educational investments, and children’s learning. We estimate this by comparing changes over time in more- and less-exposed districts outside Andhra Pradesh, before and after the 2010 regulation. This analysis accounts for fixed differences across districts, national time trends, and pre-crisis district characteristics such as microfinance lending, population, wages, consumption, distance from AP, and school infrastructure.

The link between credit and children’s human capital can operate through several channels. Reduced liquidity can tighten household budgets and lower spending on education, nutrition, and schooling inputs. However, the effect on enrolment is ambiguous. If the credit contraction weakens local labour markets, children may have fewer paid work opportunities outside school and may therefore remain enrolled. These forces can affect children even when their households are not direct microfinance borrowers, since the credit contraction can depress local demand, employment, wages, and consumption. The effects may also persist if the shock occurs during formative years, when foundational skills are still developing.

Persistent decline in children’s learning outcomes

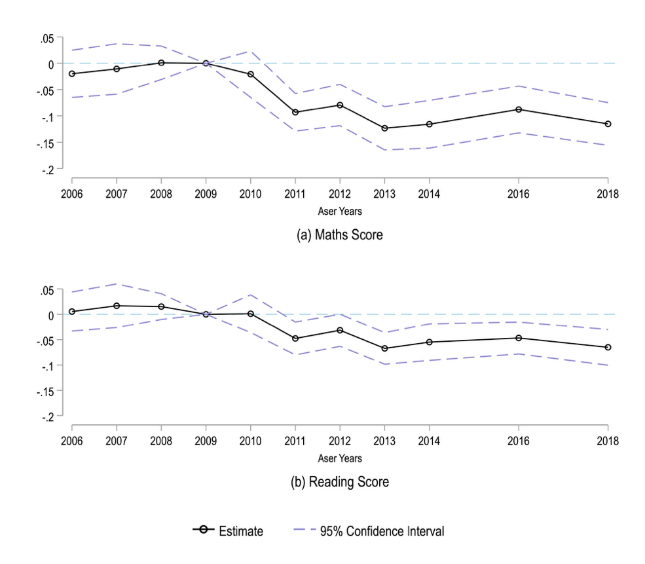

Children in districts outside Andhra Pradesh that were more exposed to the credit disruption experienced larger and more persistent declines in foundational literacy and numeracy than children in less-exposed districts (Figure 1). A one-standard-deviation increase in exposure to the credit contraction lowered maths scores by about 0.08 standard deviations and reading scores by about 0.05 standard deviations. These effects are comparable to the median learning effects reported by Evans and Yuan (2022) across randomised evaluations of education interventions in low- and middle-income countries. The learning losses continued for several years after the regulation was withdrawn, suggesting that a temporary disruption in credit access can have longer-term consequences for children’s human capital.

We then examine the channels through which the credit shock affected children. The effects were not limited to test scores. Households in more-exposed districts reduced education spending by around 13%, shifted children from private to government schools, reduced food spending, and experienced weaker livelihoods, including lower maternal employment. These results are consistent with a mechanism in which a credit contraction affects children by changing household resources and investments in education, nutrition, and schooling inputs. The effects were also larger for girls and younger children, consistent with existing gender inequalities in educational investment and with the cumulative nature of skill formation.

Figure 1: Effects of exposure to the Andhra Pradesh regulation on learning outcomes

Note: This figure shows how children’s test scores in districts outside Andhra Pradesh changed with district-level exposure to the credit contraction, year by year, relative to 2009, the year before the regulation. The solid line plots the estimated effect of a one-standard-deviation increase in exposure; the dashed lines show 95% confidence intervals. Before the regulation (2006–2009), the estimates are close to zero, indicating no differential pre-trends by exposure level. From 2011 onwards, test scores declined more in districts with greater exposure to the credit contraction, for both maths and reading.

Policy implications: Credit regulation and household welfare

The 2010 Andhra Pradesh microfinance regulation illustrates a broader policy trade-off. The ordinance was introduced in response to concerns about coercive lending and recovery practices within the state. At the same time, the contraction in microfinance credit extended beyond Andhra Pradesh through lenders’ exposure to the Andhra Pradesh crisis. Our estimates capture aggregate district-level effects, which may reflect both direct effects on borrowing households and indirect effects through the wider rural economy, including changes in local demand, employment, wages, and consumption.

Our findings show that policy interventions in financial markets can generate unintended consequences that extend well beyond the institutions being regulated. In this case, the shock affected household livelihoods, educational investments, and children’s learning, with implications for human capital formation beyond the immediate credit disruption.

Three broader lessons emerge for policymakers.

First, financial regulations should consider not only consumer protection and financial stability, but also the wider welfare consequences of sudden credit contractions – particularly in contexts where poor households rely heavily on informal or small-scale borrowing to manage income volatility.

Second, restrictions on credit access may need to be accompanied by complementary support measures, such as temporary cash transfers or other state-sponsored safety nets, to help households smooth consumption during periods of financial stress.

Third, policymakers should pay particular attention to vulnerable groups. Our findings suggest that younger children and girls were disproportionately affected, highlighting how financial disruptions can amplify existing inequalities in human capital formation.

Overall, the evidence suggests that access to credit plays a broader developmental role than simply financing consumption or business investment. It can also help households protect long-term investments in children during periods of economic stress.

References

Attanasio, O, B Augsburg, R De Haas, E Fitzsimons, and H Harmgart (2015), "The impacts of microfinance: Evidence from joint-liability lending in Mongolia," American Economic Journal: Applied Economics, 7(1): 90–122.

Banerjee, A, E Duflo, R Glennerster, and C Kinnan (2015), "The miracle of microfinance? Evidence from a randomized evaluation," American Economic Journal: Applied Economics, 7(1): 22–53.

Breza, E, and C Kinnan (2021), "Measuring the equilibrium impacts of credit: Evidence from the Indian microfinance crisis," Quarterly Journal of Economics, 136(3): 1447–1497.

Evans, D K, and F Yuan (2022), "How big are effect sizes in international education studies?" Educational Evaluation and Policy Analysis, 44(3): 532–540.

Kalliyil, M, and S Sahoo (2026), "Does restricting access to credit affect learning outcomes? Evidence from a regulatory shock to microfinance in India," Journal of Development Economics, 103790. Ungated version available here.

Karlan, D, and J Zinman (2011), "Microcredit in theory and practice: Using randomized credit scoring for impact evaluation," Science, 332(6035): 1278–1284.

Rai, V (2010), "India’s microfinance crisis is a battle to monopolize the poor," Harvard Business Review. Accessed 10 May 2026.

Roodman, D (2010), "Backgrounder on India’s microfinance crisis," Center for Global Development. Accessed 10 May 2026.

Sriram, M S (2012), "The AP microfinance crisis 2010: Discipline or death?" Vikalpa, 37(4): 113–128.

Tarozzi, A, J Desai, and K Johnson (2015), "The impacts of microcredit: Evidence from Ethiopia," American Economic Journal: Applied Economics, 7(1): 54–89.

The Economic Times (2010), "Andhra passes law to regulate MFIs." Accessed 10 May 2026.

The Hindu (2010), "Rising suicides force AP ordinance to check microfinance firms." Accessed 10 May 2026.

Cai, J, M Meki, S Quinn, E Field, C Kinnan, J Morduch, J de Quidt, and F Said (2025), "Microfinance," VoxDevLit, 3(3).