A shift from a state-led to an agribusiness-led development model in Kenya reallocated profits away from farmers towards agribusiness firms

About 78% of the world’s poor – close to 800 million people – live in rural areas and rely largely on agricultural work to make a living (World Bank 2014). The bulk of the world’s farmers are smallholders who lack the productive assets, access to technologies, and infrastructure needed to market their produce (e.g. Fafchamps and Hill 2008). Yet much of the literature in international trade treats crops as homogenous products, exchanged in perfectly competitive markets. While this may be true of world commodity markets, a vast literature finds that farmers face high transaction costs in selling their crops to markets at home and abroad.

Though governments often play an active role in crop markets, years of government control have done little to improve low yields and limited commercialisation of farming in developing countries. Following market reforms in the 1980s and 1990s, many countries moved towards policies to reduce the role of governments in crop markets and encourage agribusiness firms to work directly with farmers. The process of moving to an agribusiness model is now high on the agenda of many low-income countries. For example, the G7 countries’ New Alliance for Food Security and Nutrition in ten African countries contained a number of proposals, such as new legislation for seeds, land, contract enforcement, and taxes to ease consolidation and operation of large commercial farms (Guardian 2016, UNCTAD 2009).

Large agribusiness firms have the modern technologies, quality control methods, and access to markets that can raise rural incomes on a large scale and lift millions of low-income households out of poverty. Many countries that adopted market reforms have seen accompanying increases in the production of export crops and new agribusinesses, including supermarket chains, agro-industrial firms, and export-oriented companies offering out-grower schemes to farmers (Barrett and Mutambatsere 2008).

Yet much agricultural work, especially in the poorest parts of the world, has shown few signs of that longed-for radical transformation, raising doubts about the ability of the current model to transform agriculture (Collier and Dercon 2014).

Plans for new policies and anecdotal evidence on the role of agribusinesses in smallholder farming abound. But systematic analysis of the topic is remarkably thin (Dillon and Dambro 2017). In Dhingra and Tenreyro (2020), we inform this debate by examining the impact of policies to promote agribusiness participation in crop markets in the context of Kenya.

Kenya typifies the debate over policies to move to an agribusiness-led development model. It is a lower middle-income country in sub-Saharan Africa, where agriculture makes up 75% of the labour force. In 2004, the Kenyan national government implemented a set of policies under its Strategy for Revitalising Agriculture to shift from state-led to agribusiness-led development of major crop markets. Laws pertaining to 18 distinct crops (out of about 100) saw a big shift in policy towards easing operation of private-sector firms in intermediation and agribusiness activities, such as milling and processing of produce.

We compile the full list of crops that were shifted to an agribusiness model from official documents. The policy-affected crops include different varieties of maize, coffee cherries, wheat, cotton, sugarcane, sisal, pyrethrum, fodder, cashew nuts, rice, and oats, which together make up about half of farm incomes among Kenyan households. We obtained information on farmers’ crop incomes received per buyer from surveys of over 1,300 rural households that represent eight different agricultural-ecological zones in Kenya. Households with less than 50 acres of land were surveyed in 2000 and 2004 (Pre-policy period) and then again in 2007 (Post-policy period). Unlike many developing country panels, attrition rates are low and about 90% of the households are re-sampled across years.

Given the national policy shift and reliable panel data on farm incomes during the period, Kenya provides a unique setting to examine the impact of agribusiness policies. We find that policies to ease operation of agribusinesses raised farmers’ engagement with agribusinesses. But their incomes from policy-affected crops fell and farmers who sold to agribusinesses saw sizable losses in crop incomes.

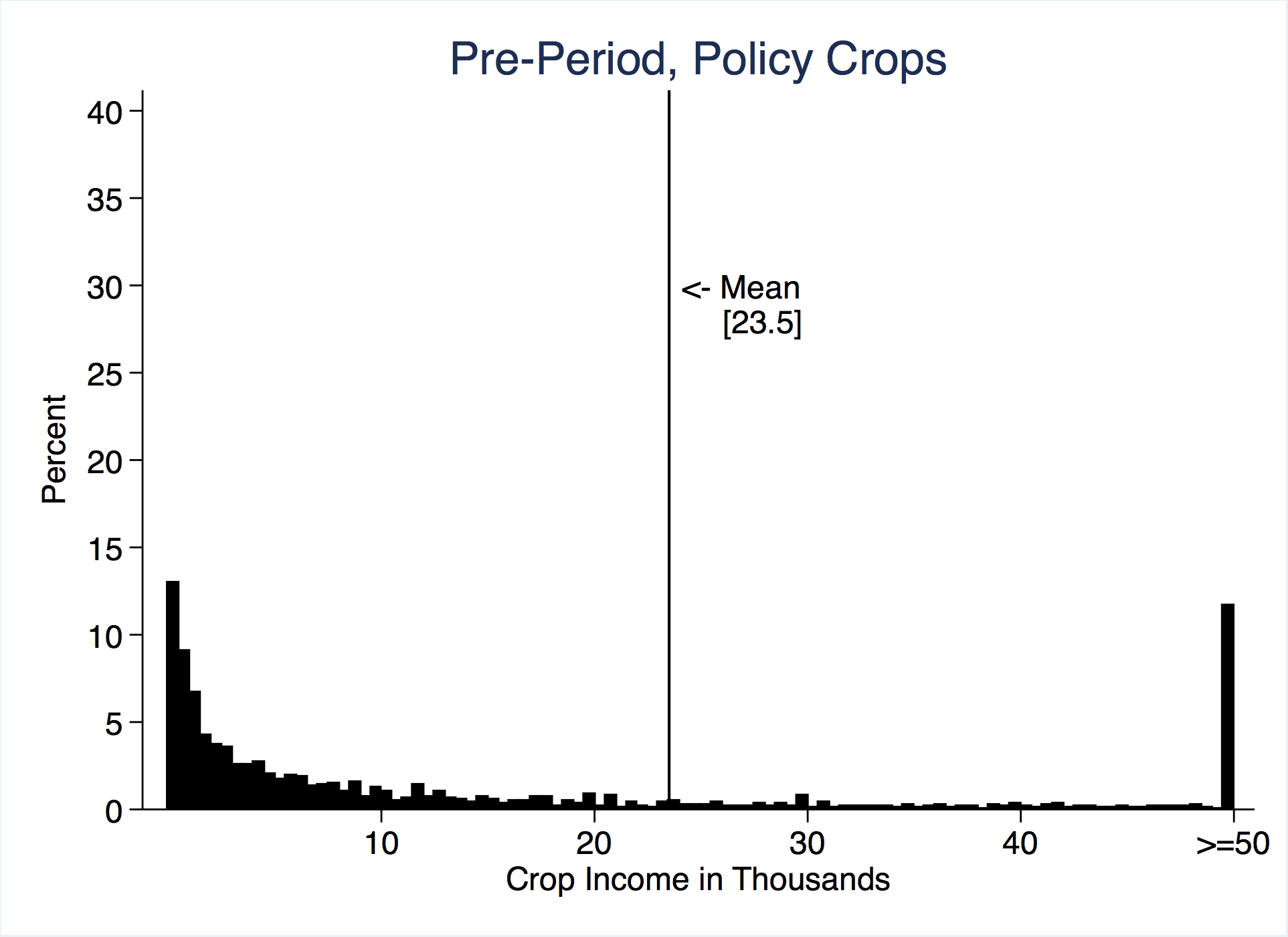

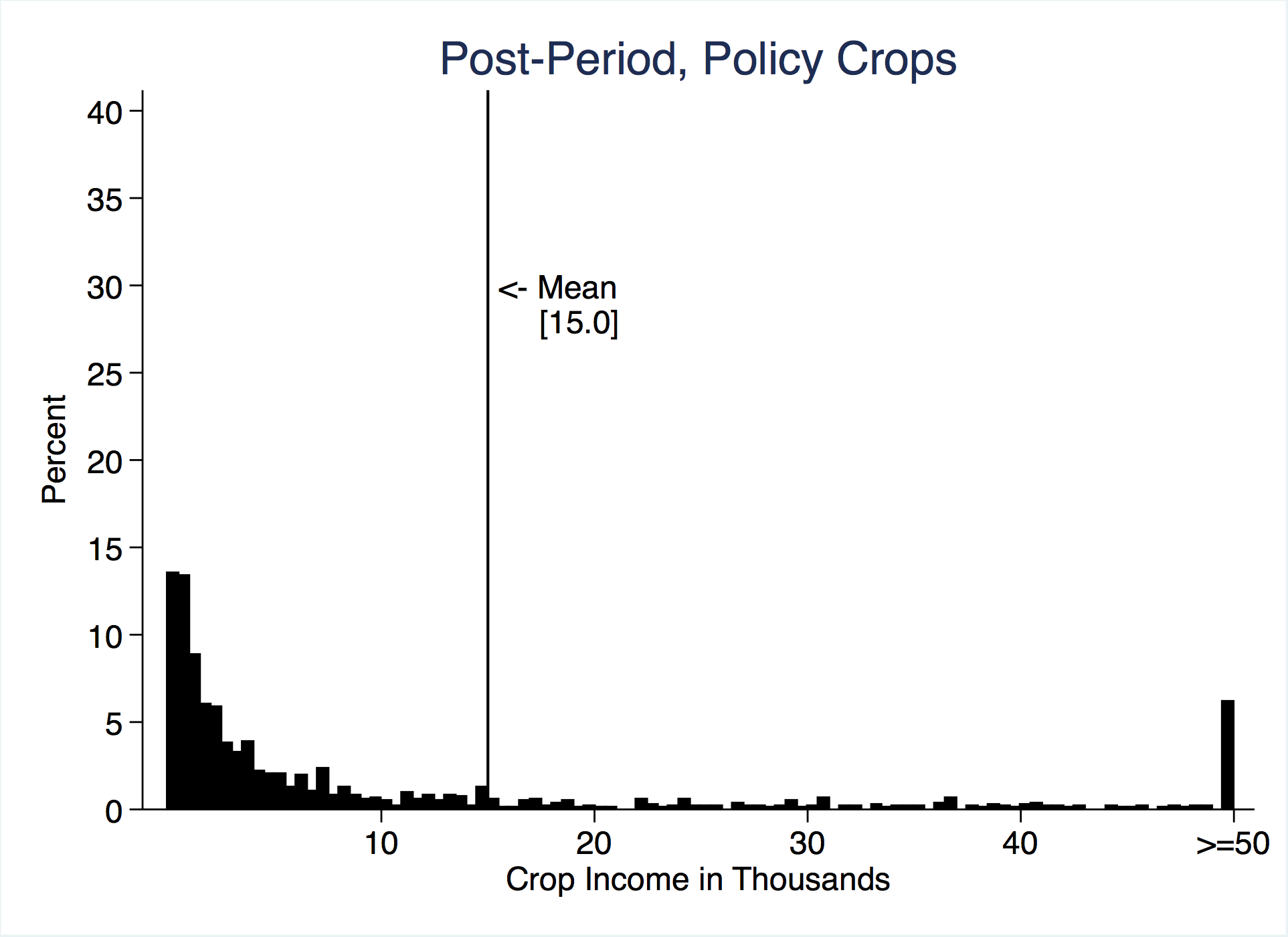

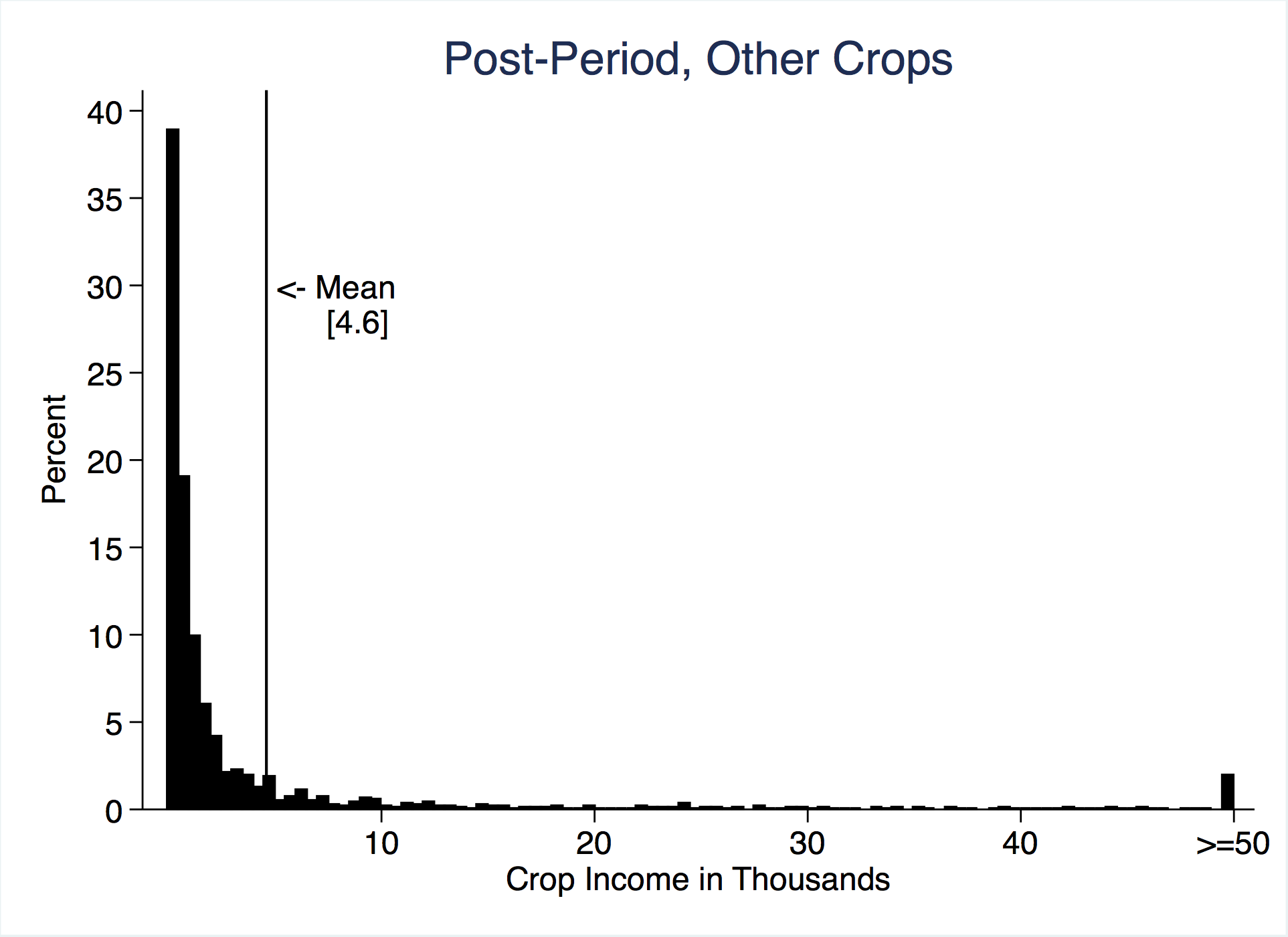

Farm incomes from the policy-affected crops fell, and they fell much more – on average by 6,600 Kenyan shillings (or US$66) more – than those from other crops. Figure 1 shows quite starkly that the entire distribution of household incomes from policy-affected crops shifted to the left after the policy change (first and third panels of Figure 1), compared to other crops that did not see a change in policy during the same period.

Figure 1 Pre- and post-period incomes from policy-affected crops and other crops

Note: Incomes above 50 (in ’000s Kenyan shillings) are top-coded for visualisation. Policy-affected crops refer to crops that were covered by Kenya’s national policy to shift from state-led to agribusiness-led development. Pre-period refers to 2000 and 2004 and Post-period to 2007.

The policy had its desired consequence in terms of agribusiness participation in these crop markets. The share of agribusinesses buying from farmers rose, making them the majority buyer of these crops. Farmers selling to agribusinesses saw large reductions in their crop incomes, which is estimated to be 7% of their crop income on average. These income losses are not driven by crop-specific negative shocks such as a collapse in world prices or spoilage of crop harvest.

Agribusiness firms did not suffer such losses after the policy shift. Putting together data on agribusiness firms listed on the Nairobi stock exchange, we estimate that profit margins of agribusinesses that were specialised in the policy-affected crops rose 5% to 9% more than other agribusinesses (which specialised in other crops). The shift to an agribusiness model therefore reallocated profits away from farmers towards agribusiness firms.

Building on previous insights on intermediated trade (Antras and Costinot 2011), we develop a model that reconciles these empirical insights. Moving to an agribusiness model raises farm incomes through improved marketability of farmers’ produce but lowers it through greater market power arising from larger purchases by firms. If crop markets outside of the agribusiness relationships are inefficient, the productivity-increasing effect is dominated by the rise in market power from policies that shift market shares towards agribusinesses. In this case, incomes of farmers fall and the losses are larger for farms that have a comparative advantage in growing policy-affected crops.

Taking the household-level welfare insights to data, we find that Kenyan households saw a reduction in total net incomes (income from farming, businesses and livestock, net of fertiliser and land preparation costs) and the value of owned assets. The welfare losses after the policy shift were concentrated in villages with a comparative advantage in the policy-affected crops.

To determine comparative advantage, we compare potential yields across crops and villages based on FAO’s agroecological model, which uses a range of geographic and climatic data to project crop yields for different parts of the world. Comparative-advantage villages (with above-median potential yields in policy-affected crops relative to other crops) had greater income dependence on policy-affected crops and suffered greater losses in household welfare.

Total net household income fell by 28.8 Kenyan shillings in comparative-advantage villages, compared to 13.1 in other villages. This is a bigger income loss for comparative-advantage villages, which amounts to 13% of mean annual consumption in rural Kenya. Households therefore scaled back on their big-ticket purchases, especially in comparative-advantage villages. There is also some evidence suggesting that credit needs for education, health, and household consumption were higher in these villages.

The results provide evidence for long-standing concerns in the literature that commercialisation of agriculture, via agribusinesses that wield monopsony power, need not raise income-earning opportunities for small farmers. This sentiment is echoed in the revised version of Kenya’s agricultural strategy, which notes that smallholder farmers could suffer when “liberalisation is carried out where there is no critical mass and enough capacity for the private sector to grow” (ASDS 2010). As long panels start to evolve, further evidence can provide a better understanding of the conditions that enable productivity gains in farming to translate into greater prosperity for low-income farmers.

Author's note: Swati Dhingra would like to thank European Research Council (Starting Grant 760037) for supporting this research.

Note: This column first appeared on www.VoxEU.org. The data used in this work were collected and made available by the Tegemeo Institute of Agricultural Policy and Development of Egerton University, Kenya. However, the specific findings and recommendations remain solely the authors’ and do not necessarily reflect those of Tegemeo Institute.

References

ASDS (2010), “Agricultural Sector Development Strategy 2010—2020”, Government of Kenya.

Antras, P and A Costinot (2011), “Intermediated Trade”, The Quarterly Journal of Economics, 126 (3): 1319-1374.

Barrett, C B and E Mutambatsere (2008), Agricultural markets in developing countries, 2nd Edition, Palgrave Macmillan.

Collier, P and S Dercon (2014), “African Agriculture in 50Years: Smallholders in a Rapidly Changing World?”, World Development 63: 92-101.

Dhingra, S and S Tenreyro (2020), “The Rise of Agribusiness and the Distributional Consequences of Policies on Intermediated Trade”, CEPR Discussion Paper No. DP14384.

Dillon, B and C Dambro (2017), “How Competitive Are Crop Markets in Sub-Saharan Africa?”, American Journal of Agricultural Economics 99 (5): 1344-1361.

Fafchamps, M and R V Hill (2008), “Price transmission and trader entry in domestic commodity markets”, Economic Development and Cultural Change, 56 (4): 729-766.

The Guardian (2020), “European parliament slams G7 food project in Africa”.

UNCTAD (2009), World Investment Report 2009: Transnational Corporations, Agricultural Production and Development.

The World Bank (2014), “For Up to 800 Million Rural Poor, a Strong World Bank Commitment to Agriculture”, World Bank Group Agriculture Action Plan: 2013-2015.