Grants and finance can alleviate poverty traps associated with lumpy investments, but the impact on development depends on the supply of investment goods

The aggregate and individual impacts of expanding financial services, such as credit and savings, to the poor can depend greatly on the importance of high-yield, indivisible investments for these populations. When small investments pay low returns but large investments pay substantially higher returns due to the need to make lumpy or indivisible investments (e.g. a tractor as opposed to seeds or fertiliser), access to credit and savings can help poor households overcome barriers to making investments at a larger, more profitable scale (Balboni et al. 2022, Banerjee et al. 2019). How important are these lumpy investments for the peri-urban poor, and what are the implications for the potential gains from expanding financial services? We explore these questions theoretically, experimentally and quantitatively in our recent working paper (Kaboski et al. 2022).

The importance of lumpy investments

To illustrate the theoretical importance of lumpy investments, we develop a simple model in which households earn uncertain, volatile labour income and have different levels of productivity, which determines how much they would profit from an indivisible investment. The theory yields three important findings.

First, we show that in the absence of financial services, households with high-yield, indivisible investment opportunities can fall into poverty traps. Households with sufficient wealth to immediately fund the investment—or easily save for it in the short-term—enter virtuous cycles of higher income, whereas otherwise identical households who lack wealth fall into poverty traps because they are never able to make these lucrative investments.

Second, although people are generally risk averse — especially poor households near subsistence where risk could have dire consequences (Rosenzweig and Binswanger 1993) — the presence of high-yield, indivisible investments can actually induce households to make risk-loving choices. Concretely, given the choice of two lotteries, one that pays out US$100 with a 50% chance of winning and another that pays out about $485 with a 10% chance of winning, the theory implies that some people choose the higher stakes lottery, even though it is riskier and offers a lower expected return. Although the high stakes lottery is riskier, the larger winnings will enable some to make the lumpy investment, and thus lead to a transformative outcome. The chance to escape the poverty trap is worth the risk. Moreover, some households appear unusually patient as they see the benefits of saving for the high-yield investment.

Third, the aggregate consequences of expanding credit or interest-bearing savings depend critically on the aggregate supply of the desired lumpy investment. If the lumpy investment is elastically supplied to a community (e.g. tractors), then access to credit or savings expands the set of people able to invest, and the increase in demand expands the amount of real investment in the community. In this case, financial services can increase income, investment, and economic mobility. If instead the lumpy investment is inelastically supplied in the community (e.g. land), then increased demand from expanding financial services manifests largely in an increase in prices rather than real investment.

The first result explains the potential importance of lumpy investments for household poverty dynamics. The second result suggests a way to test whether lumpy investments (or increasing returns) are present and important in driving household behaviour. If they are important, then the third result provides insight into the effectiveness of financial services in addressing aggregate poverty.

Experimental evidence in peri-urban Uganda

In three underbanked districts in peri-urban Uganda, we conducted an experiment based on the exact lottery choice above. In a baseline survey, we asked households about their desired investments if credit were available. The $100 and $485 pay-outs of the smaller and larger lotteries correspond to the 25th and 75th percentiles of desired investment amounts, respectively.

Consistent with our risk-loving hypothesis, we find that 27% of households chose the larger lottery, even with a lower expected value. The proportion of households which chose the large lottery corresponds closely to the 25% of the sample who wanted to make larger investments at baseline, which may suggest that, in accordance with the model, choice of the riskier lottery is correlated with investment-oriented household characteristics. Indeed, we find that households selecting the large lottery have higher levels and growth rates of wealth and business assets, are more likely to report wanting to use credit for investment, and would like to make investments that exceed $100.

How are the grants spent?

The lotteries generate randomised variation in large and small grant winners. By comparing winners and losers of each lottery, we can estimate the impact of winning the large and small grants. We evaluate short- and medium-term impacts through two endline surveys, at four (EL1) and eighteen (EL2) months after grant receipt.

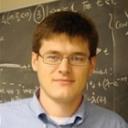

Figure 1 shows the estimated impact of winning the small lottery on expenditures of various categories at each of the endlines (note that land assets are plotted on the right-axis, using a higher scale). After four months, we find sizable and significant impacts of winning the small lottery (350,000 UGX, or approximately $100 at the time of the experiment) on livestock and business inventory, which may not require large, lumpy purchases. At eighteen months, however, the estimated impacts on these two assets have declined and are no longer statistically significant. Importantly, we see no statistically significant impacts on business durables, home durables, or land, which may be more prone to requiring larger, lumpier purchases.

Figure 1

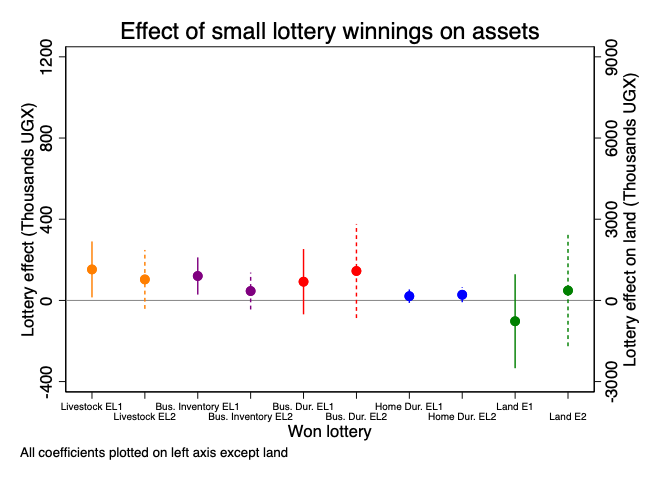

Figure 2 shows the analogous impacts of winning the large lottery (1,700,000 UGX). As with the small lottery, the large lottery increases investment in livestock and business inventory, but that impact is short-lived. In contrast to the small lottery, however, the large lottery leads to large, statistically significant increases in land at four months and even still at eighteen months. Again, the right-scale of the figure demonstrates that these impacts are sizable. Moreover, winning the large lottery leads to substantial, statistically significant, medium-term increases in business assets after eighteen months.

Figure 2

As the model’s second prediction suggested, the difference in impacts between the large and small lotteries appears in lumpier investments, which could therefore cause poverty traps. Recalling the third prediction, the distinction between land and other investments is also important, since other investments can be accumulated and purchased elastically, while the supply of land is relatively fixed, even in peri-urban areas. Indeed, we find evidence that the price of land increases in areas with greater lottery winnings, which indicates that peri-urban land is not perfectly elastic.

Policy implications

We calibrate a model to match key features of the experimental data, including lottery choices, skewed income and savings distributions, and low rates of economic mobility. We use the model to quantitatively evaluate financial policies by simulating the impacts of making interest-bearing savings accounts or, alternatively, credit available. When the lumpy investment is elastically supplied – as is the case for most types of business investment – financial services have large impacts, increasing output by as much as 52% and lowering poverty by 32%. In this case, credit is more powerful than savings. However, when the lumpy investment is in fixed supply, the impacts are muted, and savings becomes the more powerful policy.

Our findings join recent work by Gertler et al. (2021), who show long-run impacts of expanding access to interest-bearing savings among underbanked populations, and work by Acampora et al. (2022), who illustrate the economic mobility costs of land market imperfections. While we find that expanding access to interest-bearing savings only increases income by 4% (primarily through reallocating land to more productive households), it still lowers poverty by 23% and increases mobility out of poverty, with the probability of staying poor from one period to the next falling by 24%.

Editor's note: This project was funded by STEG.

References

Acampora, M, L Casaburi and J Willis (2022), “Land rental markets: Experimental evidence from Kenya”, NBER Working Paper 30495

Balboni, C, O Bandiera, R Burgess, M Ghatak and A Heil (2022), “Why do people stay poor?”, The Quarterly Journal of Economics 137(2): 785-844.

Banerjee, A, E Breza, E Duflo and C Kinnan (2019), “Can microfinance unlock a poverty trap for some entrepreneurs?”, NBER Working Paper 26346

Gertler, P, S Higgins, A Scott and E Seira (2021), “Increasing financial inclusion and attracting deposits through prize-linked savings”, Unpublished manuscript, Available here.

Kaboski, J P, M Lipscomb, V Midrigan and C Pelnik (2022), “How Important are Investment Indivisibilities for Development? Experimental Evidence from Uganda”, NBER Working Paper 29773

Rosenzweig, M and H Binswanger (1993), “Wealth, Weather Risk and the Composition and Profitability of Agricultural Investments”, The Economic Journal 103(416): 56-78.