A government-endorsed supplemental insurance scheme in China expanded coverage for hundreds of millions of people, but also crowded out private insurance purchases, suggesting that enrolment growth alone overstates the true gains in risk protection.

Expanding access to health insurance in developing countries is both important and challenging. Public systems are often constrained by limited fiscal capacity, while voluntary private insurance is hindered by adverse selection and affordability concerns (Rothschild and Stiglitz 1976, Geruso and Layton 2017). As a result, many individuals – especially those with high health risks and low incomes – remain underinsured (Wagstaff et al. 2018, World Bank 2019). To address this gap, many countries are turning to public–private partnership (PPP) insurance schemes. By combining public oversight with private provision, these programmes aim to expand access through low-cost, widely available coverage without requiring substantial public subsidies.

Yet an important question follows directly: when PPP insurance is introduced, does it add new coverage, or does it reshape the existing insurance market? While such programmes can expand access where private insurance is limited, they also change the relative attractiveness of different options, prompting individuals to adjust both whether they purchase other insurance and how much coverage they choose. Understanding PPP insurance therefore requires going beyond enrolment counts. Its impact depends on its design and how it interacts with existing insurance programmes.

Public–private partnership (PPP) insurance programme in China

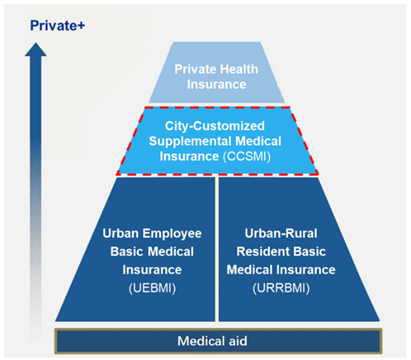

China has achieved near-universal public health insurance coverage, yet out-of-pocket spending remains relatively high (WHO 2023). To address this gap, China introduced City-Customised Supplemental Medical Insurance (CCSMI), a government-endorsed, privately operated supplemental programme. Figure 1 Panel (a) illustrates the health insurance system in China and the position of CCSMI within it.

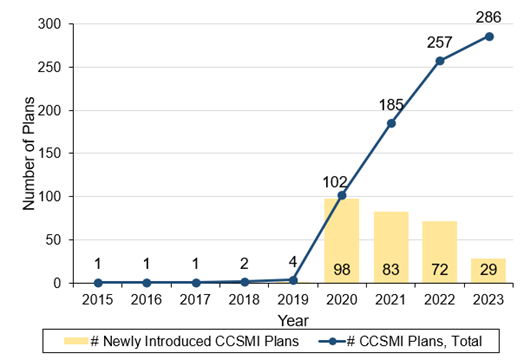

Following the central government’s guidelines in 2020, the programme expanded rapidly nationwide, as shown in Figure 1 Panel (b). By 2023, over 280 CCSMI products had been launched, covering more than 300 million individuals.

The partnership is organised at the city level. Local governments primarily play a supervisory and promotional role, without providing direct financial subsidies. Their involvement helps generate large enrolment pools, mitigating adverse selection and lowering per capita costs. As a result, premiums are very low – typically CNY 60–150 (US$10–25) – with no differential pricing or enrolment restrictions based on age or health status. While private insurers are responsible for selling the products and reimbursing claims.

Figure 1: China City-Customised Supplemental Medical Insurance (CCSMI)

(a) Health insurance system in China

(b) Introduction of CCSMI plans

Note: Panel (a) illustrates the multi-tiered health insurance system in China and the position of CCSMI. Universal public insurance (UEBMI and URRBMI) forms the core, with medical aid serving as the safety net at the bottom and private insurance providing add-on coverage at the top. CCSMI sits in between as a government-endorsed supplement to public insurance, with less comprehensive coverage than private insurance. Panel (b) shows the number of newly introduced CCSMI plans and the total CCSMI plans in China from 2015 to 2023.

What changes when access expands?

CCSMI stands out for its rapid scale-up and broad participation at low premiums. But what happens elsewhere in the insurance system? In recent work, we examine how this expansion affects private insurance markets by exploiting the staggered rollout of CCSMI across cities (Ding, Wang, and Xu 2026). We combine this policy variation with a transaction-level dataset from a major private insurer, allowing us to track the change in private insurance participation, coverage levels, and premiums, before and after the introduction of CCSMI.

Our findings show clear crowd-out effects in the private insurance market following the introduction of CCSMI. At the extensive margin, private insurance purchases decline by 13.7%; at the intensive margin, among remaining purchasers, coverage levels fall by about 13.6%, and premiums decline by 4.6%. Decomposing the premium changes suggests that about two-thirds of this decline reflects lower coverage choices, while the remainder implies that insurers adjust prices in response to a more competitive environment.

These results suggest that when access expands through PPP insurance, part of the effect comes from reshaping demand across insurance tiers rather than simply adding entirely new coverage.

The net effect of PPP insurance expansion

Comparing the increase in CCSMI enrolment with the decline in private insurance purchases, our estimates suggest that the reduction in private insurance purchases offsets roughly 25% of the increase in CCSMI enrolment. This implies that while PPP insurance expands participation, a meaningful share of the growth in CCSMI enrolment reflects substitution across insurance tiers. Moreover, since private insurance typically provides more comprehensive protection, this substitution may imply an even stronger crowd-out effect in the level of risk protection.

The design of PPP insurance and its interaction with existing plans matter

Heterogeneity results provide further evidence on when this crowd-out effect is stronger. In cities where CCSMI covers more ‘special drugs’ for cancer treatment, the reduction in the number of private insurance purchases is larger. This is because the indications of these drugs often overlap with those covered by private critical illness insurance. When these drugs are covered by CCSMI, consumers are more likely to view it as a substitute for private insurance and therefore forgo private coverage. Private insurers also adjust prices more in cities where CCSMI provides stronger special-drug coverage, in response to stronger competition.

Meanwhile, in cities with broader special-drug coverage, average coverage amounts become higher among remaining buyers. This suggests that CCSMI with greater overlap in risk protection tends to filter out individuals with lower insurance demand, leaving a pool of remaining buyers with stronger coverage needs on average. This compositional change outweighs the substitution effect at the intensive margin and leads to an overall increase in average coverage amounts.

Policy implications

The expansion of PPP health insurance should be interpreted with care. In our setting, increased enrolment does not translate one-for-one into additional insurance protection. This highlights that enrolment growth alone is an incomplete metric for evaluating insurance expansions, and that accounting for crowd-out and coverage structure is essential for understanding their welfare implications.

This substitution may nonetheless be beneficial in some respects. Low premiums and non-restrictive access make PPP insurance particularly attractive to groups less well served by existing markets. However, this may also put pressure on its own sustainability and reshape the broader insurance market.

This highlights the need for better PPP design and stronger integration with existing insurance programmes. Clear positioning of PPP insurance, by target risks or population groups, can help reduce direct substitution. Coordination with existing insurance in benefit structure, reimbursement rules, and pricing may also help mitigate disruptive competition and support a more balanced multi-tier system. Sharing clear information with consumers is also important. As individuals adjust their insurance choices, helping them better understand product differences and align coverage with their needs may improve the effectiveness of insurance expansion.

References

Ding, H, X Wang, and X Xu (2026), "The impact of public-private partnership health plans on private insurance," Journal of Development Economics, 182: 103780.

Geruso, M, and T J Layton (2017), "Selection in health insurance markets and its policy remedies," Journal of Economic Perspectives, 31(4): 23–50.

Rothschild, M, and J Stiglitz (1976), "Equilibrium in competitive insurance markets: An essay on the economics of imperfect information," Quarterly Journal of Economics, 90(4): 629–649.

Wagstaff, A, G Flores, J Hsu, M-F Smitz, K Chepynoga, L R Buisman, K van Wilgenburg, and P Eozenou (2018), "Progress on catastrophic health spending in 133 countries: A retrospective observational study," Lancet Global Health, 6(2): e169–e179.

World Bank (2019), "High-performance health financing for universal health coverage: Driving sustainable, inclusive growth in the 21st century."

WHO (2023), "Out-of-pocket expenditure as percentage of current health expenditure, data by country."