Central banks can lose credibility quickly when policy decisions are seen as politically driven. Evidence from Brazil shows that even a single ungrounded policy shift can unanchor inflation expectations and deteriorate inflation dynamics.

Editor's note: The authors have made slides available here.

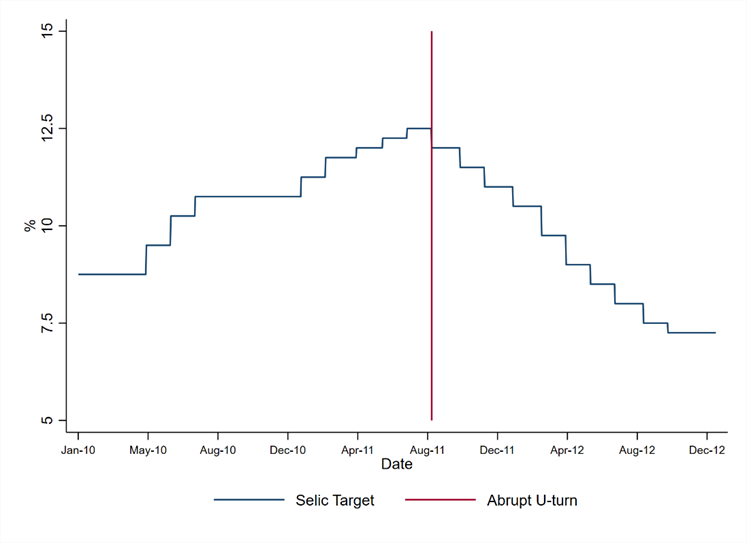

In August 2011, Brazil’s central bank (BCB) unexpectedly cut interest rates, abruptly reversing an ongoing tightening cycle (Figure 1). In the following days, inflation expectations, including for long-term horizons, jumped up and continued to rise thereafter. The episode shows that hard-earned credibility can be lost quickly if a central bank takes actions that are perceived as inconsistent with its stated policy objectives.

Figure 1: Abrupt monetary policy reversal

Notes: Selic is BCB’s policy rate. Vertical line marks policy meeting that delivered abrupt policy reversal.

But what are the costs of losing credibility? Recent years have seen unusually large supply shocks. Supply-chain disruptions during the pandemic, higher tariffs after the Trump administration’s trade policy shift, and surging oil prices linked to conflict in the Middle East all put significant cost pressure on firms. Although these shocks generated historically high inflation, they have not – at least so far – produced the stagflation seen in the 1970s. In many economies, inflation has fallen sharply since its pandemic peak without triggering a recession.

There is a consensus that central bank credibility has played a key role in moderating the effects of these shocks. In a classic survey of central bankers, Blinder (2000) documents near-unanimous agreement that credibility is essential for maintaining price stability and enhancing policy effectiveness. The main channel through which credibility is thought to operate is the anchoring of inflation expectations.

When households, firms, and investors believe that inflation will return to target within a reasonable horizon, they treat shocks as temporary. Firms are less likely to raise prices aggressively and workers are less likely to demand large wage increases. As a result, inflation responds less to shocks, allowing central banks to stabilise the economy with smaller interest rate adjustments. A credible central bank, in this sense, anchors long-run expectations and reduces the real costs of disinflation.

In recent research (Bonomo et al. 2024), we use the abrupt policy reversal by Brazil’s central bank, illustrated in Figure 1, to identify the causal effects of loss of credibility on inflation expectations.

Brazil’s 2011 policy reversal

Monetary policy affects the economy not only through the level of interest rates, but also through how policy actions are understood. When a monetary policy decision is inconsistent with reasonable expectations, it can be perceived as a change in the central bank’s objectives. In such cases, even a single decision can have large effects on expectations. The 2011 policy reversal is particularly informative because it surprised virtually all professional forecasters. It was widely interpreted as a departure from the central bank’s commitment to its inflation target, rather than as a response to new economic information.

To study this question, we use high-frequency data from the Central Bank of Brazil’s Focus survey, whereby participants can update their forecasts daily if they so wish. This allows us to track how expectations evolved immediately following the policy reversal.

Unanchoring expectations

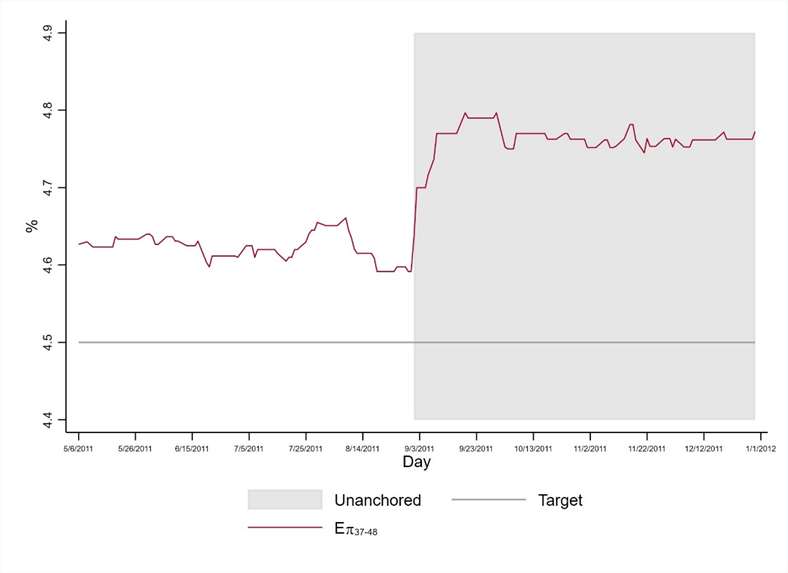

We find that inflation expectations unanchored almost immediately. In the days following the policy shift, both short- and long-horizon inflation forecasts increased (Figure 2). At the same time, expected policy rates were revised downward. This combination is inconsistent with an improving inflation outlook and instead reflected a deterioration in perceived policy commitment (Bonomo et al. 2024).

Figure 2: Daily mean inflation expectations from the BCB’s Focus survey, for 4 years ahead

Note: Shaded area begins on the day after the monetary policy meeting that delivered the abrupt reversal.

‘Unanchoring’, in this context, goes beyond a temporary deviation of expectations from the target. As we document in our paper, unanchoring reflects a broader change in how expectations are formed. After the policy reversal, long-run expectations became more sensitive to short-run news, more dispersed across forecasters, and more volatile. Thereafter, forecasters also updated their projections more frequently and reacted more strongly to monetary policy surprises. Taken together, these patterns indicate that the nominal anchor broke loose.

Credibility and anchored inflation expectations returned only after five years. This reanchoring followed a broader regime change, including the impeachment of Brazil’s president, the appointment of a new economic team, and a shift in both fiscal and monetary policies (Bonomo et al. 2024).

These shifts in expectations have important implications for economic behaviour. In related work (Abib et al. 2025), we use producer price microdata to show that firms respond more strongly to cost shocks when expectations are unanchored. The key margin is not how often firms change prices, but by how much they adjust them. When firms do update prices, they make larger changes. As a result, cost shocks pass through more strongly to inflation, making stabilisation more difficult.

These findings provide evidence on a critical channel through which credibility is thought to operate. By changing the behaviour of inflation expectations, it alters the transmission of shocks to inflation. When expectations are well anchored, firms and households treat shocks as temporary. When they are not, the same shocks can generate more persistent and amplified inflation dynamics.

So, why did the BCB chose to reverse policy so abruptly? Contemporary accounts and market commentary interpreted the policy ‘U-turn’ as reflecting government influence rather than a technical reassessment of economic conditions. This interpretation is especially relevant today because it links credibility loss directly to threats to central bank independence – whether perceived or real. If policy actions start to be seen as subject to political influence, they can alter how agents interpret future decisions, even if the actual policy framework remains unchanged.

A growing body of evidence shows that these concerns are not unique to emerging economies. Political pressure on central banks can affect expectations and financial market outcomes even in advanced economies. For example, Eichengreen et al. (2025) show that perceived threats to central bank independence are associated with expectations of lower short-term interest rates, higher long-term yields, and greater macroeconomic uncertainty. Using high-frequency social media data, Bianchi et al. (2023) find that political attacks on central banks move financial markets and inflation expectations in real time. Historical evidence from Drechsel (2025) points in the same direction, showing that political pressure on the Federal Reserve can lead to persistent increases in the price level.

Implications for monetary policy

Taken together, this evidence reinforces a key insight: political pressure does not need to directly alter policy decisions to matter. It can instead affect how those decisions are understood. When agents begin to doubt the central bank’s commitment to its objective, expectations become more sensitive to shocks and less tightly anchored to the target.

The policy implications are straightforward but consequential. Central bank independence is not merely a legal or institutional feature – it is a key requirement for credibility in practice. Maintaining that credibility requires a consistent alignment between actions and stated objectives, especially in environments where political pressures are salient.

References

Abib, D, J Ayres, M Bonomo, C Carvalho, S Eusepi, S Matos, and M Perrupato (2025), "Price setting when expectations are unanchored," Unpublished manuscript.

Bianchi, F, R Gómez-Cram, T Kind, and H Kung (2023), "Threats to central bank independence: High-frequency identification with Twitter," Journal of Monetary Economics, 135: 37–54.

Blinder, A S (2000), "Central bank credibility: Why do we care? How do we build it?" American Economic Review, 90: 1421–1431.

Bonomo, M, C Carvalho, S Eusepi, M Perrupato, D Abib, J Ayres, and S Matos (2024), "Abrupt monetary policy change and unanchoring of inflation expectations," Journal of Monetary Economics, 145: 103576.

Drechsel, T (2025), "Political pressure on the Fed," Unpublished manuscript.

Eichengreen, B, G Viswanath-Natraj, J Wang, and Z Wang (2025), "Under pressure? Central bank independence meets blockchain prediction markets," Unpublished manuscript.