When people in developing countries believe their tax systems are fair and progressive, they are more willing to pay taxes.

Editor’s note: For a broader synthesis of themes covered in this article, check out our VoxDevLit on Taxation. The author has made slides available to accompany this research here.

Many governments in developing countries struggle to raise enough tax revenue, primarily due to low levels of compliance (Jensen et al. 2024). It is therefore valuable to understand what influences people’s willingness to comply. Traditionally, economists believed that people simply weighed the cost of paying taxes against the risk of being caught if they did not (Allingham and Sandmo 1972). However, there has been a growing recognition that other factors, such as trust in government and beliefs about fairness in the tax system, may lead to ‘quasi-voluntary’ compliance (Luttmer and Singhal 2014, Prichard et al. 2019, Best et al. 2025). For example, if people believe richer citizens pay more taxes and/or poorer citizens benefit the most from how tax revenue is spent, they may be more likely to comply.

My research provides the first cross-country, experimental evidence on how the progressivity of the tax system strongly shapes people’s willingness to pay tax across the developing world (Hoy 2025). Using a randomised survey experiment with more than 30,000 respondents across eight middle-income countries, I find that when people learn their country’s tax system is progressive (i.e. that richer households pay a higher share of their income in taxes), their willingness to pay taxes increases. When they learn it is not progressive, their willingness to pay taxes falls. These findings suggest that efforts to improve a country’s fiscal position, which increase (decrease) progressivity, may also have an additional benefit (or potentially backfire) by increasing (decreasing) compliance.

Understanding tax progressivity across countries

I collect data on people’s preferences for progressivity and their willingness to pay taxes using a randomised online survey experiment with over 3,200 respondents in each of the following countries: Colombia, Ghana, Indonesia, Jordan, Mexico, Sri Lanka, South Africa, and Tanzania. The total effect of taxes is only progressive in half of these countries.[1] Although online survey experiments on policy preferences are common in high-income countries (Alesina et al. 2018, Stantcheva 2021), they remain relatively rare in lower-income countries, with few exceptions (Hoy and Mager 2021, Hoy et al. 2026). In these settings, online surveys can only be representative of internet users, not the entire population, as a significant minority of people do not have access to the internet (ITU 2025).

In this work, respondents were first asked about their beliefs and preferences for the progressivity of taxes and government transfers (e.g. cash transfers) in their country, and then randomly assigned to one of four groups:

- Tax treatment: received information about how taxes are distributed across income groups.

- Transfer treatment: received information about how government transfers are distributed across income groups.

- Combined treatment: received information about the combined effect of taxes and government transfers across income groups

- Control: received no information.

Information about the distribution of taxes and government transfers across income groups was sourced from the Commitment to Equity (CEQ) Database (Lustig et al. 2020).

Respondents were then asked a series of questions about their willingness to pay taxes, which is often referred to as ‘tax morale’ (Luttmer and Singhal 2014). For example, they were asked if it is important to pay taxes, if they would pay even without enforcement, and if the government always has the right to make people pay taxes. These questions have been widely used in other contexts (Prichard et al. 2022) and featured in regional surveys, such as the Afrobarometer. The answers were combined into a ‘tax morale’ index.

People prefer progressive tax systems

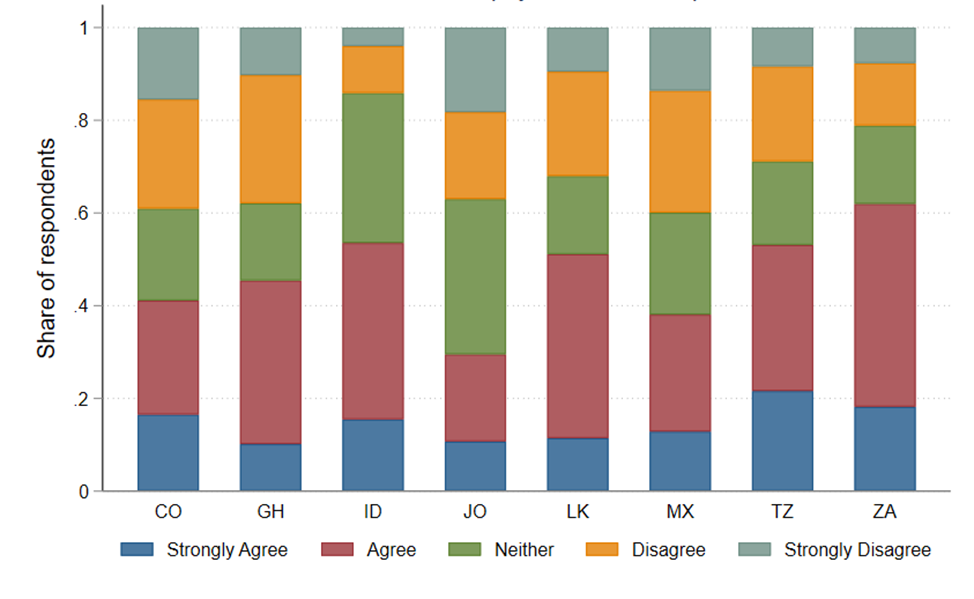

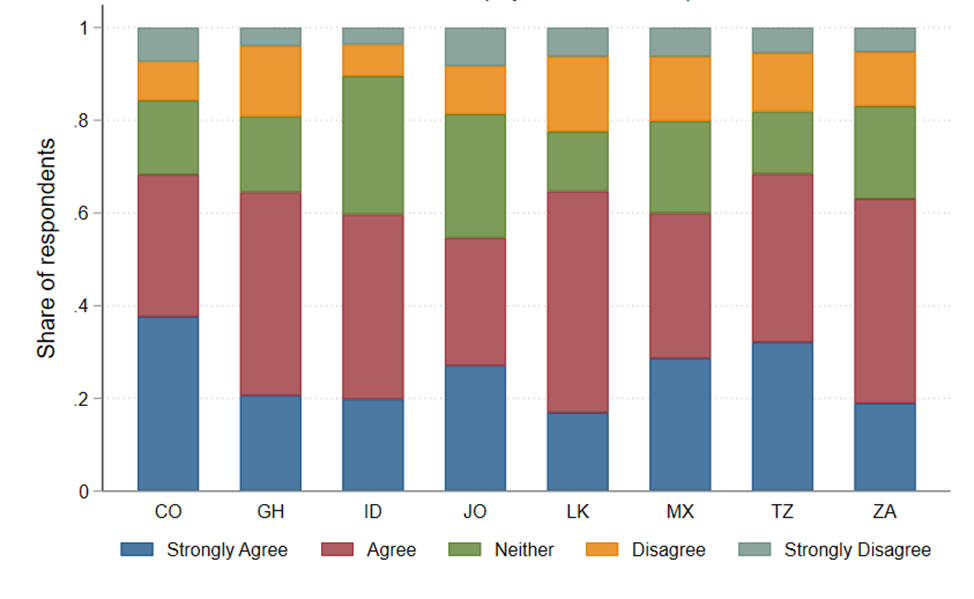

On average, around two-thirds of respondents across the eight countries stated that they prefer richer households to pay a higher share of their income in tax than poorer households, but less than half stated that they believed this was the case. Figure 1 illustrates the proportion of respondents in each country who believe the tax system is progressive, as well as those who would prefer it to be. Even richer respondents prefer progressive taxation (but to a slightly lesser extent). In all countries, in every income group, more respondents agreed than disagreed that richer households should pay a higher share of their income in tax than poorer households.

Figure 1: Beliefs and preferences regarding the progressivity of taxes across countries

(a) Believe that richer households pay more taxes than poorer households

(b) Prefer that richer households pay more tax than poorer households

Note: This figure shows the share of respondents stating they had a prior belief and/or an existing preference that the tax system is progressive in their country. CO: Colombia. GH: Ghana. ID: Indonesia. JO: Jordan. LK: Sri Lanka. MX: Mexico. TZ: Tanzania. ZA: South Africa.

Information about tax progressivity shapes people’s willingness to pay tax

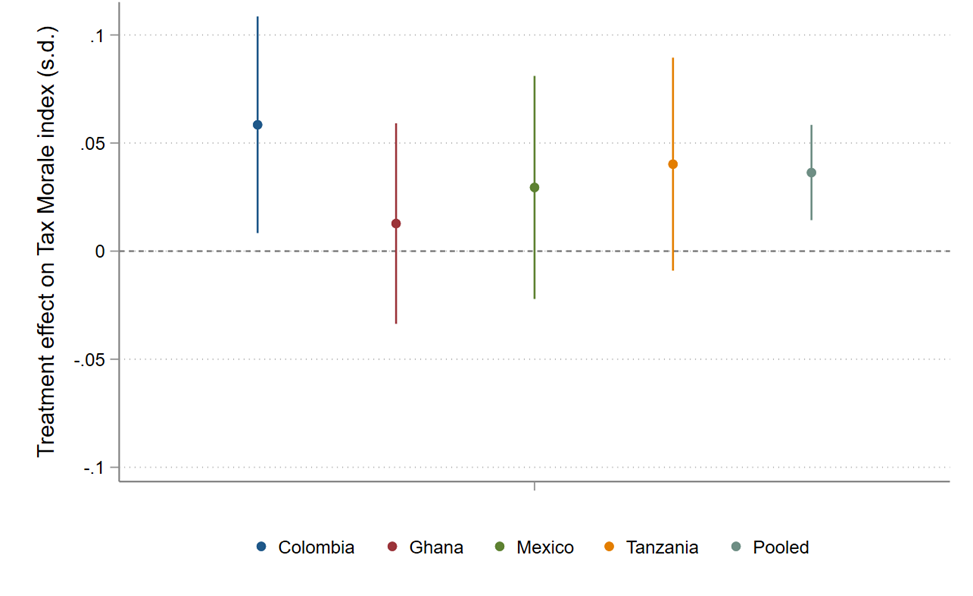

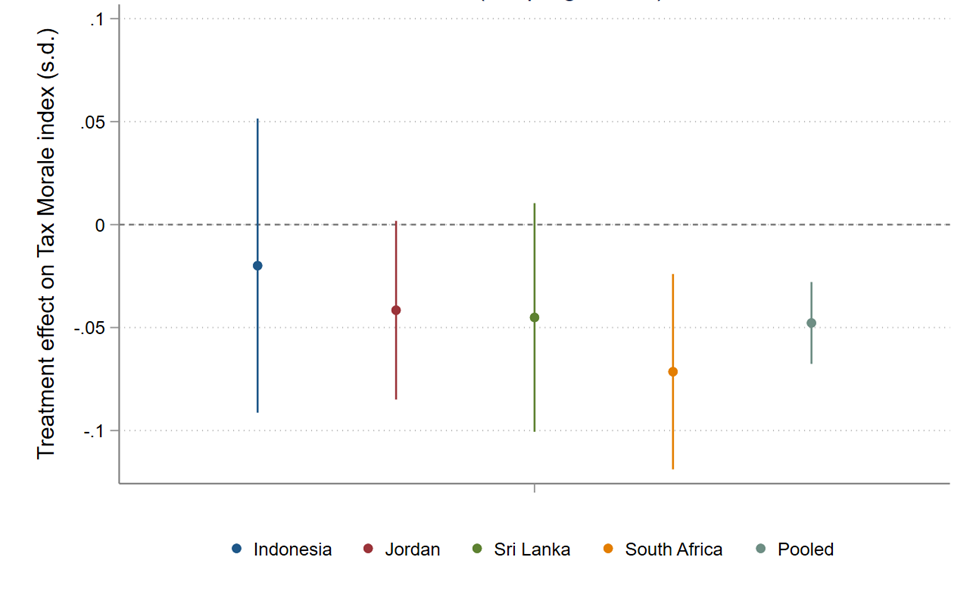

Information about the progressivity of taxes substantially shapes respondents’ willingness to pay taxes. Figure 2 shows the impact of the tax treatment on the tax morale index in each country. When taxes were progressive (in Colombia, Ghana, Mexico, Tanzania), respondents who received this information reported higher tax morale. When taxes were not progressive (in Indonesia, Jordan, Sri Lanka, South Africa), respondents who received this reported lower tax morale. Interestingly, the negative effects (from receiving information about taxes not being progressive) were stronger than the positive effects. In other words, people’s tax morale appears to be easier to erode than to build.

Figure 2. Overall impact of tax treatment in each country

(a) Taxes (progressive)

(b) Taxes (not progressive)

Note: This figure shows the overall impact of tax treatment in each country and the results pooled across countries. The ‘Tax Morale index’ is an unweighted average of the Z-scores of all outcome variables, oriented so that a higher index means more tax morale.

These effects were driven mainly by two groups. People whose prior beliefs were wrong (i.e. people who thought taxes were progressive but learned they were not, or vice versa), and who prefer a progressive tax system. In contrast, people whose prior beliefs were accurate or who did not value progressivity showed little change in tax morale.

Similar, albeit weaker, effects exist for the combined treatment, which had information about taxes and government transfers, while receiving information about the progressivity of transfers (i.e. who receives cash transfers) had almost no impact. This suggests that people’s tax morale is influenced more by who pays taxes than by who benefits from them.

Implications for tax policy

- A more progressive tax system may have greater tax compliance: Governments mainly focus on increasing tax revenue through enforcement, but my research suggests that equity in the tax system also influences people’s willingness to pay. When citizens believe the rich contribute their fair share, their intrinsic motivation to comply increases. Conversely, if the system appears regressive, such as when rich individuals avoid taxes, then tax morale collapses. However, recent research suggests that increasing progressivity may not necessarily increase revenue (Ajzenman et al. 2024).

- Effective communication of tax reforms is critical: My research suggests that policymakers can improve tax compliance by not only adjusting tax policy and administration, but also by communicating more effectively. If taxes are already progressive, public information campaigns highlighting this could strengthen tax morale. Reforms that boost progressivity and are effectively communicated could yield a ‘double dividend’: greater fairness and higher compliance.

- Beware of the fiscal consequences of reducing progressivity: Changes in the tax system that aim to raise revenue but reduce progressivity, such as raising consumption taxes, could backfire. Even if they appear to increase revenue on paper, they risk undermining voluntary compliance. In extreme cases, lower compliance could entirely offset the intended fiscal gains. Pursuing progressive tax reforms is not only a moral imperative but also a pragmatic one, as it is likely to raise more revenue.

References

Ajzenman, N, G Cruces, R Perez-Truglia, D Tortarolo, and G Vazquez-Bare (2024), “From flat to fair? The effects of a progressive tax reform,” Unpublished manuscript.

Alesina, A, S Stantcheva, and E Teso (2018), “Intergenerational mobility and preferences for redistribution,” American Economic Review 108(2): 521–554.

Allingham, M, and A Sandmo (1972), “Income tax evasion: A theoretical analysis,” Journal of Public Economics 1(3–4): 323–338.

Best, M, L Caloi, F Gerard, E Kresch, J Naritomi, and L Zoratto (2025), “Greener on the other side: Inequity and tax compliance,” Unpublished manuscript.

Hoy, C (2025), “How does progressivity impact tax morale? Experimental evidence across developing countries,” Journal of Development Economics 172: 103398.

Hoy, C, F Mager (2021), “Why are relatively poor people not more supportive of redistribution? Evidence from a randomized survey experiment across ten countries,” American Economic Journal: Economic Policy 13(4): 299–328.

Hoy, C, Y Kim, M Nguyen, M Sosa, and S Tiwari (2026), “Attitudes towards reducing fossil fuel subsidies: Evidence across 12 middle-income countries,” Journal of Development Economics 178: 103612.

International Telecommunication Union (ITU) (2025), "Measuring digital development: Facts and figures 2024," ITU, Geneva.

Jensen, A, A Brockmeyer, and L Gadenne (2024), “Taxation and Development,” VoxDevLit 12(1).

Lustig, N, C Mariotti, and C Sánchez-Páramo (2020), “The redistributive impact of fiscal policy indicator: A new global standard for assessing government effectiveness in tackling inequality within the SDG framework,” World Bank Blogs.

Luttmer, E, and M Singhal (2014), “Tax morale,” Journal of Economic Perspectives 28(4): 149–168.

Prichard, W, A Custers, R Dom, S Davenport, and M Roscitt (2019), Innovations in Tax Compliance: Conceptual Framework, Policy Research Working Paper No. 9032, World Bank.

Prichard, W, A Custers, R Dom, S Davenport, and M Roscitt (2022), Innovations in Tax Compliance: Building Trust, Navigating Politics, and Tailoring Reform, World Bank, Washington, DC.

Stantcheva, S (2021), “Understanding tax policy: How do people reason?” Quarterly Journal of Economics 136(4): 2309–2369.