Peer-led endorsement doubled mobile banking uptake and increased formal savings among women in Ghana.

Editor’s note: For a broader synthesis of themes covered in this article, check out our VoxDevLits on Microfinance and Mobile Money.

In the last decade, bank account ownership worldwide has increased dramatically—from 50% to 76% of adults (Demirgüç-Kunt et al. 2021). Yet in many rural areas, actively using these accounts remains difficult due to the high time and travel costs of visiting physical bank branches (Dupas et al. 2018, Dupas and Robinson 2013). Digital financial services such as mobile banking offer a promising way to reduce these barriers, but adoption remains limited.

One approach to boosting adoption is to offer small financial incentives that encourage individuals to try new digital tools (Bryan et al. 2014, Cole et al. 2011, Dalton et al. 2024, Meriggi et al. 2021, Gertler et al. 2023). However, incentives alone may not be enough to generate continued use. Research highlights the crucial role of peers in encouraging the sustained adoption of new technologies, often through ‘passive learning’ where individuals observe others (Conley and Udry 2010, Griliches 1957). However, this organic diffusion can be slow, sometimes taking years due to gradual knowledge spread and a lack of direct incentives for early adopters to share their expertise. Can active encouragement from peers, combined with incentives, accelerate the adoption process for novel digital financial services?

We answer this question through a field experiment with microfinance groups in rural Ghana (Riley, Shonchoy, and Osei 2025). We compare the effects of small financial incentives against peer-led endorsement for the adoption of mobile banking services. While incentives alone increased mobile banking adoption, the peer-led approach was far more effective: when women were encouraged and supported by trained microfinance group leaders, adoption of mobile banking more than doubled, and formal savings rose by nearly a third.

Mobile banking for microfinance clients

Our research took place in partnership with Opportunity International Savings and Loans (OISL), Ghana's largest microfinance provider. OISL offers microfinance loans to low-income women through village-based groups. Each group has a designated group leader who helps organise regular meetings, during which cash repayment for the loan are made to a credit officer. All loan recipients, by default, receive a bank account at OISL.

OISL had recently launched a mobile banking platform that allowed clients to deposit or withdraw funds from their bank accounts using their mobile phones, avoiding long and costly trips to bank branches. The mobile banking platform was designed for low-income microfinance clients: It operated in a similar manner to mobile money—a service that most women were already familiar with—without the need for a smartphone or internet. There was a fixed cost for conducting a transaction of only US$0.16. This was substantially lower than the average of US$2.40 typically spent on transportation, along with nearly an hour of travel time, required for in-person deposits. Despite these substantial reductions in transaction costs, few women had used mobile banking to manage savings.

Studying the impact of incentives and peer endorsement

We randomly assigned 115 microfinance groups to one of three arms:

- Control: Standard information about mobile banking.

- Incentive: Standard information plus a one-time cash reward for making a mobile banking transaction during a one-month period.

- Endorsement: The same one-time cash reward as the Incentive arm plus:

- A half-day training for group leaders on how to use and explain mobile banking.

- Referral incentives for leaders based on how many group members used the platform.

This design allowed us isolate the effect of peer endorsement and training, beyond just financial incentives.

We tracked mobile banking transactions and bank account saving balances using high-frequency administrative data for six months during and after the inventions. An endline survey with 400 women from these groups, conducted one-month post-intervention, allowed us to explore underlying mechanisms such as knowledge, trust, fraud concerns, peer interaction, and digital payment preferences.

Peer endorsement substantially increased mobile banking adoption and savings

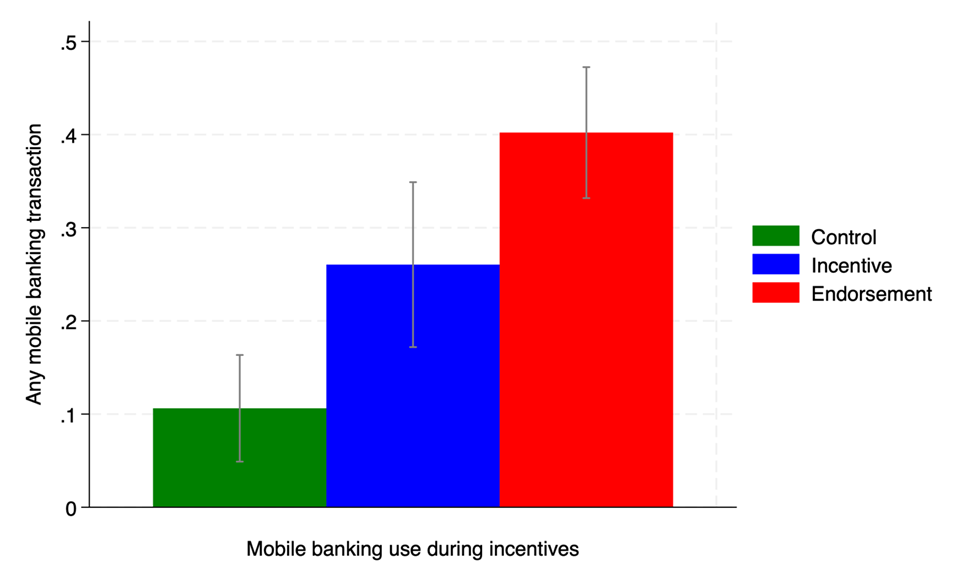

In the month when incentives were active, mobile banking usage in the Incentive group rose to 26%–more than double the 10% seen in the control group. Usage in the Endorsement group was even higher, with 40% making a mobile banking transaction during the month.

Figure 1: Likelihood of making any mobile banking transaction during the month that incentives were active

Note: Mean and 95% confidence interval.

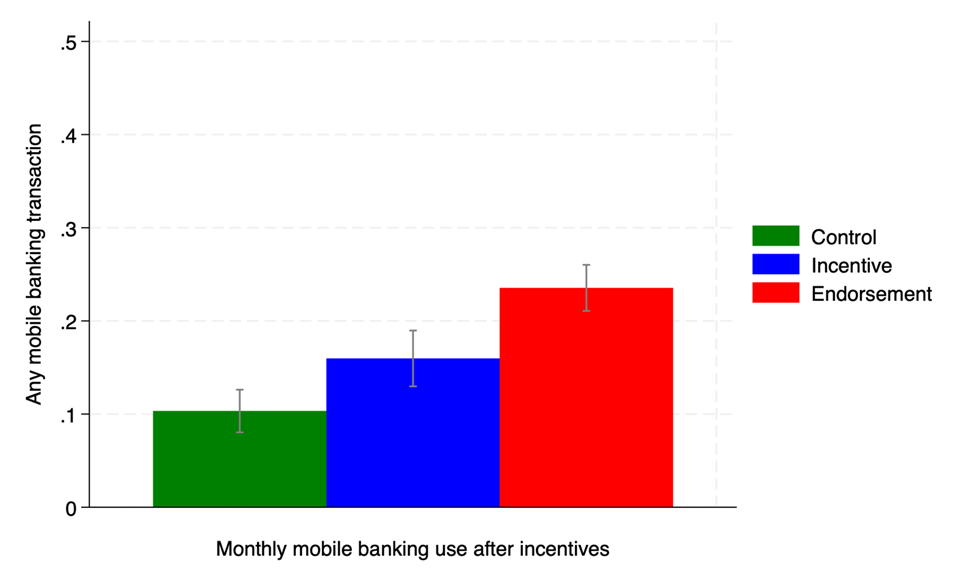

These positive effects on mobile banking use persisted for six months after the end of the interventions: mobile banking use in the Incentive treatment remained 50% higher than in the control group. Use in the Endorsement arm remained more than double that in the control group each month. Mobile banking was mainly used for deposit transactions into the linked bank account.

Figure 2: Monthly likelihood of making any mobile banking transaction

Notes: Average for the six months after the incentives ended. Mean and 95% confidence interval.

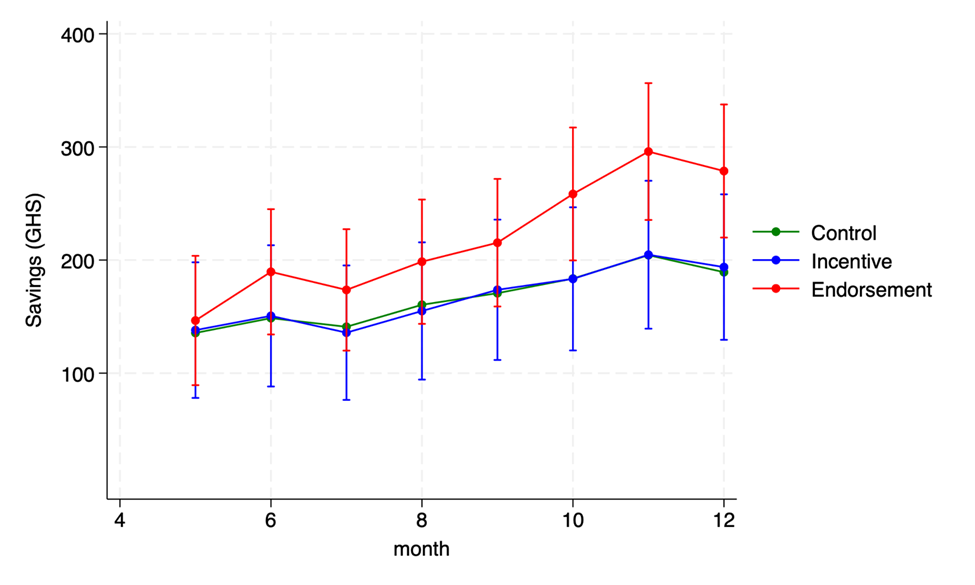

This use of mobile banking for bank deposits led to increased saving in the linked bank account. Women in the Endorsement group increased their formal bank savings by 30% over six months. By contrast, those in the Incentive group showed no significant savings increase. While we cannot say for sure if the saving increase in the Endorsement arm crowd-out or are in addition to other forms of saving, evidence from our endline survey suggests total savings increased in the short term.

Figure 3: Average end of month saving balance in all OISL accounts by month (in GHS)

Notes: Incentives were offered during month 6. Mean and 95% confidence interval for each treatment arm.

Why peer endorsement worked: Knowledge, interaction, and fraud confidence

Endline survey data indicates that peer endorsement increased women’s mobile banking usage by enhancing knowledge, boosting confidence in handling fraud and conducting transactions safely, and fostering interaction and support within their microfinance groups. We observed no impact of endorsement on trust in the technology, as it was already high. The incentives alone only led to a small increase in knowledge about mobile banking. This suggests that peer endorsement was essential to encouraging active learning and addressing concerns about fraud, leading to greater adoption and continued use.

The Endorsement intervention combined two components for the microfinance group leader: intensive training and referral incentives. Evidence suggests that providing group leaders with intensive training was the primary driver of the intervention’s effectiveness. Leaders who received training were far more effective at encouraging adoption among their members. This highlights the vital role of a knowledgeable, trusted resource within the group–someone who can offer direct help and build confidence. While the referral incentives may have provided additional motivation, they did not appear to be sufficient without the leader also receiving training.

Policy takeaways: Leveraging existing networks to encourage technology adoption

Our results offer three key takeaways for policymakers and practitioners:

- Use existing social infrastructure: Microfinance groups, savings groups, churches, and cooperatives often have trusted leaders who can be trained to support digital finance adoption.

- Invest in peer-led support: Small financial incentives can prompt trial, but peer encouragement enhances learning and sustained use.

- Address confidence in handling risks: Even when overall trust in a technology is high, specific concerns like fraud can deter adoption. Interventions should actively build users' knowledge and confidence in detecting and mitigating fraud, a role effectively fulfilled by trained peer leaders.

References

Bryan, G, S Chowdhury, and A M Mobarak (2014), “Underinvestment in a profitable technology: The case of seasonal migration in Bangladesh,” Econometrica, 82(5): 1671–1748.

Cole, S, T Sampson, and B Zia (2011), “Prices or knowledge? What drives demand for financial services in emerging markets?” The Journal of Finance, 66(6): 1933–1967.

Conley, T G and C R Udry (2010), “Learning about a new technology: Pineapple in Ghana,” American Economic Review, 100(1): 35–69.

Dalton, P S, H Pamuk, R Ramrattan, B Uras, and D van Soest (2024), “Electronic payment technology and business finance: A randomized, controlled trial with mobile money,” Management Science, 70(4): 2590–2625.

Demirgüç-Kunt, A, L Klapper, D Singer, and S Ansar (2022), "The Global Findex Database 2021: Financial inclusion, digital payments, and resilience in the age of COVID-19," World Bank.

Dupas, P, D Karlan, J Robinson, and D Ubfal (2018), “Banking the unbanked? Evidence from three countries,” American Economic Journal: Applied Economics, 10(2): 1–54.

Dupas, P and J Robinson (2013), “Saving constraints and microenterprise development: Evidence from a field experiment in Kenya,” American Economic Journal: Applied Economics, 5(1): 163–192.

Gertler, P, S Higgins, A Scott, and E Seira (2023), “Using lotteries to attract deposits,” Unpublished manuscript.

Griliches, Z (1957), “Hybrid corn: An exploration in the economics of technological change,” Econometrica, 25(4): 501–522.

Meriggi, N F, E Bulte, and A M Mobarak (2021), “Subsidies for technology adoption: Experimental evidence from rural Cameroon,” Journal of Development Economics, 153: 102710.

Riley, E, A S Shonchoy, and R D Osei (2025), “Incentives and endorsement for technology adoption: Evidence from mobile banking in Ghana,” Journal of Development Economics, 176: 103511.