In fragile and conflict-affected situations (FCS), weak institutions, chronic instability, and repeated shocks have stalled growth for many years. With bold reforms and sustained global backing, FCS economies could harness untapped resources and demographic potential to drive lasting, inclusive development.

Persistent fragility and conflict are pushing FCS economies further behind

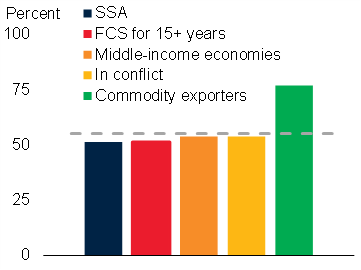

The 39 economies classified as being in fragile and conflict-affected situations (FCS) span all regions and income groups, but share common vulnerabilities: chronic instability, weak institutional capacity, exposure to severe shocks – and, in many cases, widespread conflict and violence. About half are in sub-Saharan Africa, with the majority relying heavily on commodity exports. A comparable share is currently experiencing conflict and has been classified as FCS for at least 15 years (Figure 1). Since 2000, per capita incomes of FCS economies have not just lagged – they have fallen further behind other emerging markets and developing economies (EMDEs), as well as advanced economies – especially since the COVID-19 pandemic (World Bank 2025).

Figure 1: Features of FCS economies

Source: World Bank. Note: FCS = fragile and conflict-affected situations; SSA = Sub-Saharan Africa. Sample includes the 39 economies classified as FCS in 2025. ‘FCS for 15+ years’ refers to economies that remain in FCS status for 15 years or more since 2006, when the World Bank’s current FCS classification system was established.

Conflicts have surged to multi-decade highs, leaving a deep human toll and lasting economic scars

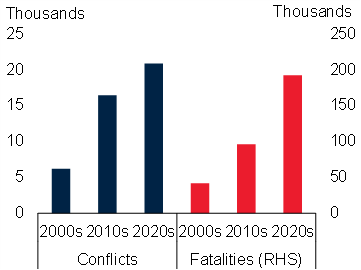

Since the early 2000s, the number of conflicts and related fatalities has more than tripled, with most of the increase occurring after 2010 (Figure 2). These conflicts are often protracted, with many countries experiencing repeated or overlapping episodes of violence. Recent conflicts, including those in Europe, sub-Saharan Africa, and the Middle East, have caused tens of thousands of deaths and widespread destruction.

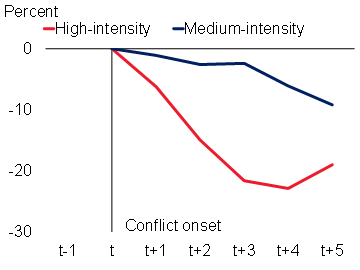

Conflict destroys infrastructure, deters investment, displaces labour, and erodes both human and physical capital (Novta and Pugacheva 2021). The impacts extend beyond borders: neighbouring countries face higher security costs, disrupted trade, and refugee inflows that strain public services – and can themselves become more vulnerable to violence. Conflicts are associated with large output losses, with the most severe episodes leading to a 20% decline in per capita GDP after five years of onset. In FCS economies in particular, a 1% increase in conflict-related fatalities per million population is estimated to reduce per capita GDP by 3.7% after five years (World Bank 2025).

Figure 2: Global conflict, fatalities, and economic losses

Panel A: Global conflict and fatalities

Panel B: Cumulative loss of per capita GDP (median) following the onset of medium and high-intensity conflicts

Sources: Uppsala Conflict Data Program (database), World Bank. Note: EMDEs = emerging market and developing economies; FCS = fragile and conflict-affected situations. Panel A: Average number of annual conflicts and conflict-related fatalities, calculated as a simple average per period indicated. The Uppsala Conflict Data Program defines a conflict ‘event’ as an incident in which armed force was used by an organised actor against another organised actor, or against civilians, resulting in at least one direct death. Last observation is December 2024. Sample includes up to 82 economies. Panel B: Medium- (high-) intensity conflicts involve at least 50 (150) fatalities per million at onset, with no exceedance of that threshold in the four prior years. Lines show the average cumulative gap between forecasted and actual per capita GDP following high-intensity conflict. Forecasts are from Global Economic Prospects one year before onset. Sample includes 14 conflicts in 14 EMDEs (3 not currently FCS) from 2006–23.

Poverty and food insecurity are becoming increasingly concentrated in FCS economies

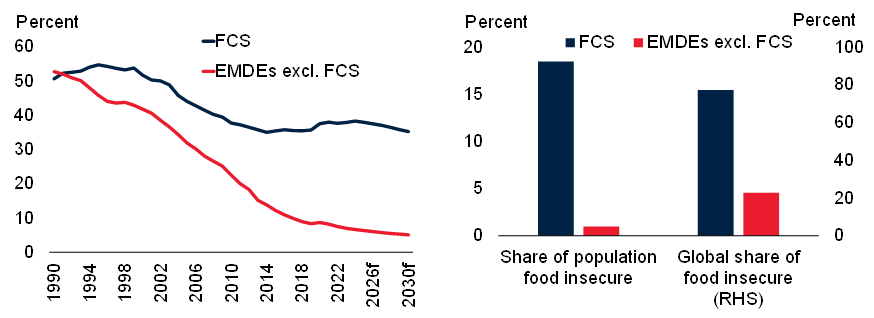

Nearly 40% of the population in FCS economies lives in extreme poverty (Figure 3). By 2030, more than 435 million people – almost 60% of the global poor – are projected to reside in these economies. Acute food insecurity has also surged alongside rising conflict, now affecting nearly one in five people in FCS economies (FSIN and GNAFC 2024). Conflict, violence, and chronic instability – compounded by years of underinvestment in health, education, infrastructure, and social protection – have left poverty and hunger deeply entrenched, with slow, erratic, and weak growth potential offering little prospect for improvement.

Figure 3: Poverty and food insecurity in FCS economies

Sources: Mahler et al. (2022); World Bank; World Bank Poverty and Inequality Platform (database). Note: EMDEs = emerging market and developing economies; f = forecast; FCS = fragile and conflict-affected situations. The FCS group is based on the current World Bank classification. Extreme poverty is defined as living on less than $3 per day in 2021 purchasing power parity (PPP). The observation for 2024 is estimated; data from 2025 onward are forecasts. Sample includes 154 EMDEs, of which 39 are FCS.

Macroeconomic pressures are intensifying

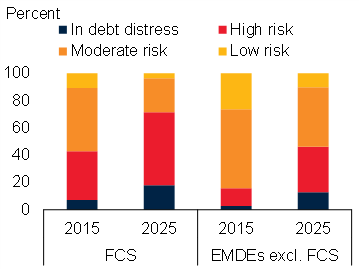

Compounding their challenges, public finances are under severe strain in FCS economies, with around 70% of them currently in, or at high risk of, debt distress (Figure 4). Weak revenue collection and high borrowing costs leave little fiscal space and constrained policy options. External shocks – from commodity price volatility to exchange rate swings – have added to economic instability. At the same time, structural transformation has lagged: industrial and services sectors remain underdeveloped, human capital is weak and underutilised, capital formation is low, and financial systems are shallow – further undermining growth prospects.

Figure 4: Risk of debt distress

Sources: World Bank-IMF Debt Sustainability Framework; World Bank. Note: EMDEs = emerging market and developing economies; FCS = fragile and conflict-affected situations. The FCS group is based on the current World Bank classification. Sample covers economies where the Joint World Bank-International Monetary Fund Debt Sustainability Framework for Low-Income Countries is applied, as of end-March 2025, including 67 EMDEs, of which up to 28 are FCS.

With the right reforms, FCS economies can transform resource wealth and demographic tailwinds into sustained development

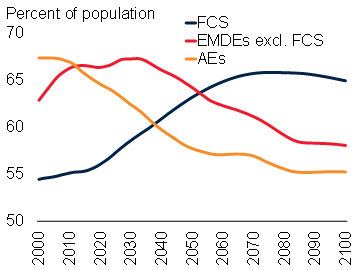

FCS economies suffered some of the sharpest contractions and weakest recoveries among EMDEs in the wake of the pandemic – setbacks many are unlikely to reverse for years. Yet, expanding working-age populations offer a demographic opportunity, if paired with investments in education, healthcare, and infrastructure to spur job creation (Figure 5, Development Committee 2025). Many FCS economies are also rich in natural resources, including minerals essential to the global energy transition, agricultural land, and, in some cases, tourism potential once conflict subsides. Harnessing this potential will require capable institutions, transparent governance, and greater investment in infrastructure and human capital, alongside conflict-prevention policies that address the root causes of violence and strengthen early-warning systems. Sustained global support is also crucial for FCS economies to secure lasting peace, strengthen resilience, and advance development (World Bank 2024a, 2024b).

Figure 5: Working-age population

Sources: UN World Population Prospects (database); World Bank. Note: AEs = advanced economies; EMDEs = emerging market and developing economies; FCS = fragile and conflict-affected situations. The FCS group is based on the current World Bank classification. Lines show working-age population as a share of the total population. Sample includes 38 advanced economies and 150 EMDEs, of which 36 are FCS.

Authors’ note: The findings, interpretations, and conclusions expressed in this column are entirely those of the authors. They do not necessarily represent the views of the World Bank, its Executive Directors, or the countries they represent.

References

Development Committee (2025), "2025 Development Committee communiqué."

FSIN (Food Security Information Network) and GNAFC (Global Network Against Food Crises) (2024), "Global report on food crises 2024."

Mahler, D G, N Yonzan and C Lakner (2022), “The impact of COVID-19 on global inequality and poverty,” World Bank.

Novta, N and E Pugacheva (2021), “The macroeconomic costs of conflict,” Journal of Macroeconomics 68 (June): 103286.

World Bank (2024a), “Learning from the evidence on forced displacement: Program brief.”

World Bank (2024b), "Empowering fragile states: IDA’s strategic role in conflict-affected areas and vulnerable countries."

World Bank (2025), "Global economic prospects."