Senegal enters 2026 with a soaring public debt and very limited degrees of freedom. So, what should the government do?

Editor’s note: This article is an adapted, shortened version of the Finance for Development Lab’s Policy Note: A Strategic Compass for Navigating Senegal's Debt Crisis.

The situation in Senegal is likely to be the next major test for the international financial system. With public debt at around 130% of GDP, avoiding a dramatic crisis will require considerable international support.

Senegal’s secret deficit has caused an unexpected debt crisis

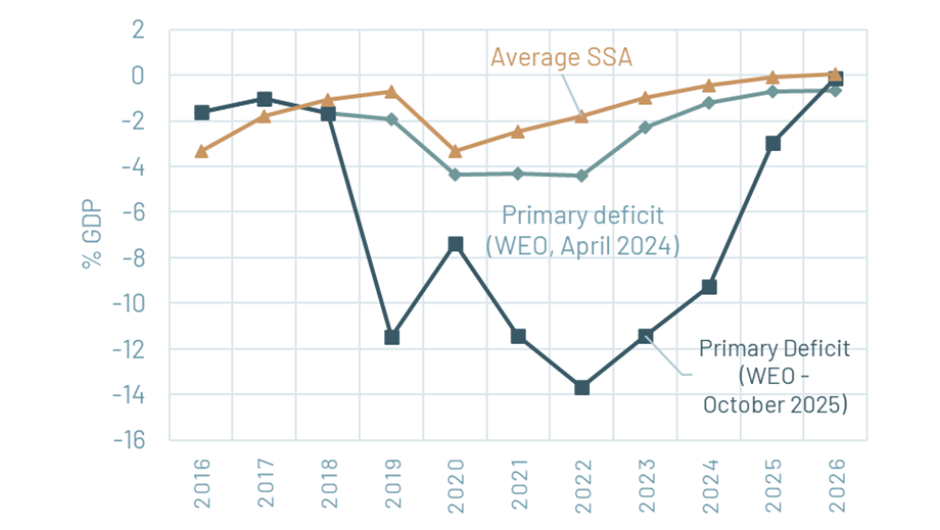

In mid‑2024, Dakar was jolted by an announcement from the incoming administration: fiscal deficits and public debt had been materially underreported for several years. In February 2025, a report by the Court of Auditors[1] estimated that ‘hidden’ deficits averaged about 5.5% of GDP between 2019 and 2023, which implies average overall deficits of about 11% of GDP, and that public debt in 2023 was about 25 percentage points of GDP higher than previously reported, at around 100% of GDP. Over the course of 2025, this number was further revised: the current official estimate of public debt at the end of 2024 was FCFA 23,667 billion, or 119% of GDP.[2] IMF estimates, which consolidate additional public‑sector liabilities, including some SOE debt and domestic expenditure arrears, place total public-sector debt at about 132% of GDP at end‑2024.[3]

Figure 1: Primary deficit in Senegal, before and after the debt discovery

Source: IMG World Economics Outlook, April 2024 and October 2025.

Senegal’s debt, previously assessed at ‘moderate’ risk of debt distress under the IMF–World Bank framework, rapidly shifted to a higher-risk position, although it took a few months for markets and observers more broadly to start fearing a default. Following the announcement, the IMF suspended disbursements under its programme while it investigated the misreporting and assessed the implications for debt sustainability and programme conditionality. This had direct implications for other multilateral lenders, with loans by the World Bank and the African Development Bank declining and net transfers becoming negative for the first time in years. On the private side, Eurobond prices fell sharply but did not indicate distress concerns until October 2025. However, Senegal effectively lost access to international capital markets and became increasingly reliant on domestic and WAEMU regional market financing to cover large gross financing needs. While some international banks continued to fund the government, the terms were rather opaque and included collateralised debt.

What is the cost and structure of Senegal's debt?

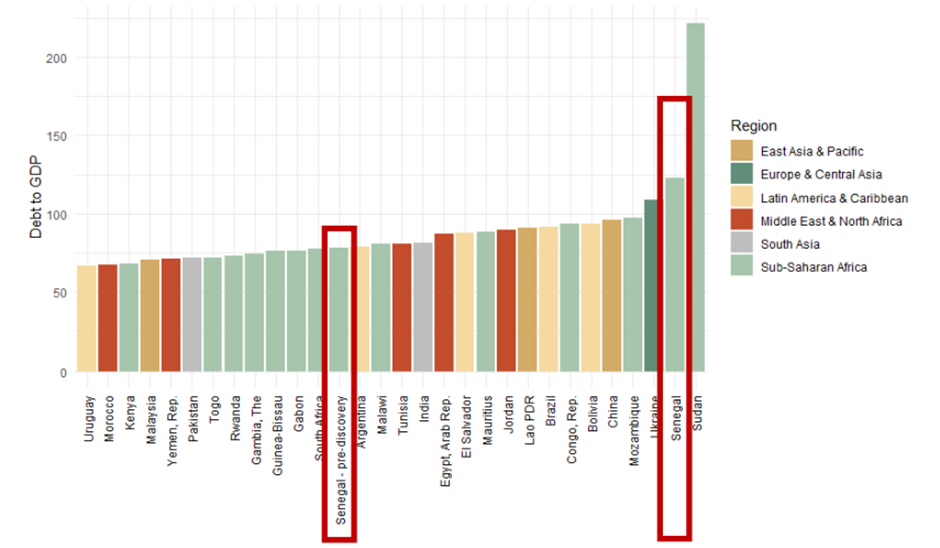

Senegal’s debt, at 132% of GDP, is a rare outlier among developing countries. While high-income economies with large domestic markets and, in some cases, reserve asset status manage to sustain very high debt levels, developing countries are rarely able to do so. Whether due to ‘debt intolerance’ (Reinhart et al. 2003) or inequalities inherent to the global financial architecture (Gallagher and Koczul Wright 2022), or both, there is a limit set on debt levels that developing countries can manage. Currently, Senegal ranks second in debt levels. Apart China and Brazil, all low- and middle-income countries with debt-to-GDP ratios above 90% are in debt distress or currently undergoing restructuring.

Figure 2: Public debt to GDP in low- and middle-income countries, 2025

Source: IMF WEO, October 2025. We remove high-incomes and countries with populations of less than a million in 2025.

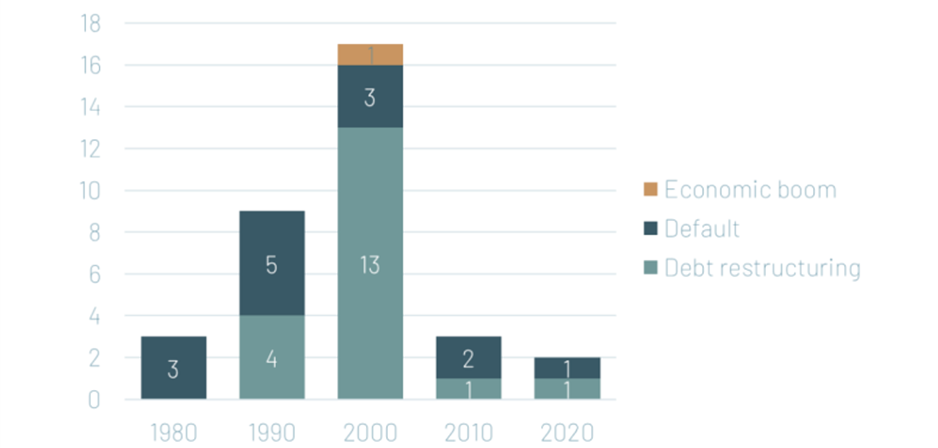

We have identified 36 episodes in which developing countries have had a debt ratio above 100% of GDP for several years. All, except one of them, were resolved through a debt restructuring and/or a default: only Antigua and Barbuda, in 2001-2004, lowered its ratio thanks to fast economic growth.[4]

Figure 3: Debt resolutions for countries with debt above 100% of GDP

Source: WEO, October 2025, Asonuma Trebesch (2016 and 2023 update), various IMF documents.

There are no ‘good’ options left on the menu

Senegal faces two possible paths.

The first is to avoid restructuring and attempt to refinance at scale while sustaining an exceptionally tight fiscal stance for an extended period.

The second is to pursue an IMF-supported restructuring of bilateral and private external claims under the Common Framework, to reduce near-term debt service and make the required fiscal adjustment less self-defeating, while seeking to shield regional lenders and the WAEMU financial system from destabilising losses.

The ‘no-restructuring’ path

The ‘no-restructuring’ path should be viewed as a narrow corridor rather than a robust strategy. Even if it can be made to work under favourable assumptions, it requires simultaneously (i) a consolidation large enough to reassure creditors without undermining growth and revenues, and (ii) sizeable refinancing at unusually low rates from partners willing to take sovereign risk at scale; conditions that may prove politically difficult to sustain. The rollover calendar also makes delays costly. External payments begin to come due in concentrated fashion; starting with the Eurobond amortisation in March 2026; and continued reliance on short maturities and collateralised structures risks tightening the sovereign–bank relationship and shifting the problem onto the regional balance sheet.

And the consolidation required to meet sustainability criteria would be very hard to achieve. Cutting 10 percentage points of primary deficit in three years has rarely been done, outside the context of countries with huge benefits from natural resources, much larger than Senegal’s oil and gas revenues. It would also need to be maintained in the long run: few countries, and none in West Africa, have been able to maintain primary surpluses over several years as would be required.

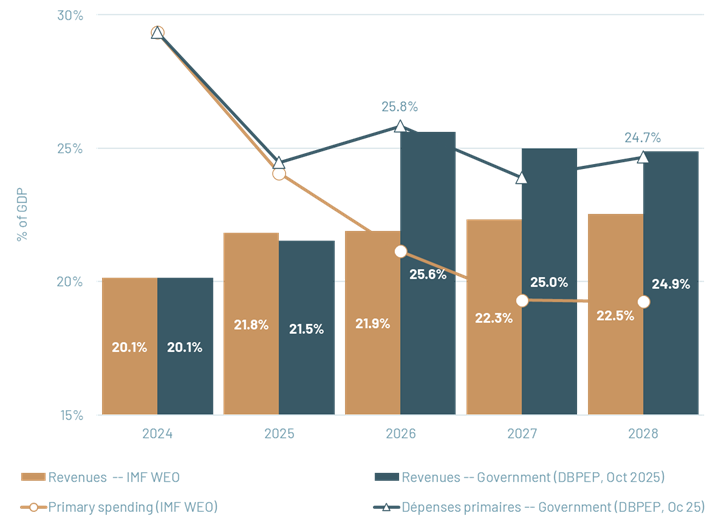

Figure 4: Consolidating would require major changes in expenditure and/or revenues

The IMF path

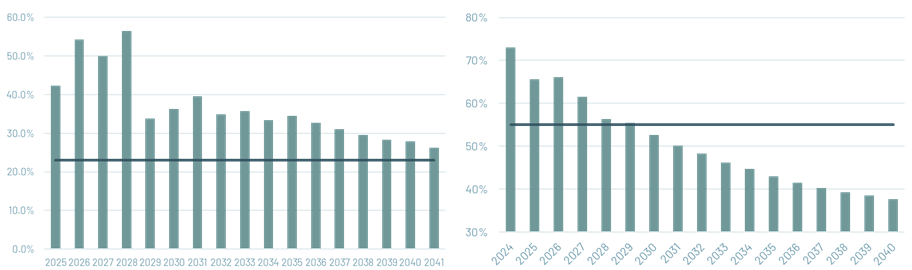

Finding cheap financing is difficult. The IMF is key here: it provides budget support at a 0% interest rate, and it unlocks budget financing from other (bilateral and multilateral) institutions. Obtaining an IMF programme would require convincing the IMF that debt is sustainable, but the criterions it uses for Debt Sustainability Analysis make it very unlikely. Under a realistic scenario, external debt service to revenues is above 50% from 2026 to 2028, whereas the level deemed ‘safe’ is 23%. Senegal stays above that threshold for the entire projection period, until 2040. Other options would be to turn to generous bilateral lenders, but few would be willing to take such risks in the long run without major compensations, such as privatisations (or land sales, like in Egypt).

Figure 5: Debt Sustainability indicators

(a) External public debt service to revenues (b) External debt stock (present value) to GDP

If debt treatment is pursued, the central lesson from recent crises is to aim for an early and comprehensive resolution, rather than ‘too little, too late’. A key strategic choice in this path is the debt restructuring perimeter. Preserving domestic-currency liabilities held within WAEMU is not merely a distributional preference; it is rather a macro-financial imperative to prevent regional contagion and a broader credit crunch that would ultimately worsen outcomes for Senegal and its external creditors.

To work, such strategy will require support from international partners: the main two bilateral creditors, France and China, should commit, at a high level, to deliver fast and comprehensive debt treatment from the official sector in order to unlock IMF financing, using procedural innovations introduced recently. It should also implicate the private sector as early as possible. This treatment should be a test that the Common Framework is able to deliver. The IMF should design its programme to limit the impact on essential spending, including investment in human capital, priority infrastructure and security.

Restructuring public debt is never easy, and creates considerable uncertainties, but it can lead to recovery. This would lead to a rating in ‘default’ by rating agencies, and a temporary exclusion from Eurobond market, but those ratings are lifted relatively rapidly if the debt treatment is deep enough and restores future prospects (as was the case in Ghana). During those negotiations, Senegal would be eligible for budget financing from the IMF (under the ‘lending into arrears’ policy) and other multilaterals.

While there are considerable uncertainties for pursuing both options, the economic literature tells us that ‘gambling for redemption’ by borrowing the way out of a crisis rarely works. And the human costs of debt crises materialise whether or not a country formally defaults – the longer Senegal waits, these costs become larger.

References

Cour des Comptes du Sénégal (2025), “Audit du rapport sur la situation des finances publiques: Gestions de 2019 au 31 mars 2024.”

Ndiaye, A, and M Kessler (2026), “A strategic compass for navigating Senegal’s debt crisis,” Finance for Development Lab.

Reinhart, C M, K S Rogoff, and M Savastano (2003), “Debt intolerance,” Brookings Papers on Economic Activity, 34: 1–74.

République du Sénégal (2025), “Stratégie de gestion de la dette à moyen terme.”

Robinson, M (2024), “Breaking the cycle of debt in small island developing states (SIDS): The Antigua and Barbuda experience,” ODI and Resilient Sustainable Islands.