Disaster relief can discourage people from adapting to future disasters – for example, by reducing incentives to relocate. But in low-income settings, cash relief can also ease liquidity constraints and enable adaptation. Evidence from Pakistan’s 2010 floods shows that both of these forces exist but that they offset each other, so that cash relief does not cause more people to stay in disaster-prone areas.

Editor’s note: For a broader synthesis of themes covered in this article, check out our VoxDevLit on Climate Adaptation.

Extreme weather events are expected to intensify with climate change (IPCC 2021). In response, governments are expanding disaster relief programmes. Cash transfers are administratively efficient, cost-effective and thus easier to scale quickly compared to in-kind support. Recent evidence shows that the speed at which cash transfers are delivered is key to their positive effects on wellbeing and reduced costly coping strategies (Pople et al. 2024, Pople et al. 2025).

However, there is a concern that if households expect repeated compensation in high-risk areas, they may invest less in avoiding risk. Such behaviour, often described as ‘moral hazard’ by economists, has been observed in the context of floods in the US (Henkel et al. 2024, Pang and Sun 2022) as well as sea wall construction in Indonesia (Hsiao 2025). This concern is particularly relevant in the case of migration away from disaster-prone areas – a key margin of adaptation.

Another mechanism that could potentially work in the opposite direction is the liquidity effect. Migration is expensive and risky; in low-income contexts, many households are living close to subsistence, making them liquidity constrained and risk averse. A cash transfer can finance transport, job search, and serve as a financial cushion if migration fails. In such circumstances, cash transfers can enable migration by easing liquidity and risk constraints (Bryan et al. 2014, Tiwari and Winters 2019, Gazeaud et al. 2023, Diop 2025).

Hence, in a disaster setting, it is theoretically ambiguous how cash relief will affect migration. In recent work (Bin Khalid and Mattsson 2025), we empirically study the effect of cash relief on migration using the context of the 2010 floods in Pakistan.

Pakistan’s Watan Card programme

In 2010, Pakistan experienced one of the worst floods in its history, affecting over 20 million people. In response, the government launched the Watan Card programme, which delivered cash transfers through debit cards.

The programme ran in two phases: initially, households in villages designated ‘calamity-affected’ received PKR 20,000; later, households identified as damaged in a follow-up survey received PKR 40,000 more. The total transfer (PKR 60,000) was roughly equivalent to 3.2 months of average rural household income, and about 56% of the damage suffered by the average household in a flooded village.

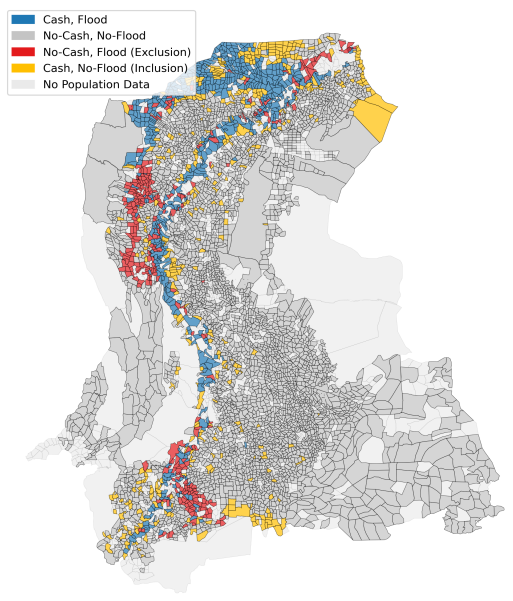

A key feature of the programme for the purposes of our research is that targeting was imperfect. Although villages should have qualified if more than 50% of their land area was submerged, implementation relied on local visual assessments and was vulnerable to errors and political interference. An independent evaluation concluded that fewer than half of potentially eligible households received a card (Hunt et al. 2011). Using satellite flood maps, we estimate that 38% of villages that received relief were not more than 50% flooded (inclusion error), while 34% of villages that were more than 50% flooded were excluded (exclusion error).

These errors create useful comparison groups. Some non-flooded villages received cash transfers, and some flooded villages did not. Comparing non-flooded villages with and without cash transfers, and flooded villages with and without transfers, allows us to estimate the effect of relief while holding flood exposure constant.

Figure 1: Floods and cash relief

To measure the long-run effect of the cash relief programme, we assemble a new village-level panel dataset for Sindh, Pakistan’s second-most populous province. We digitised village boundary maps and historical census records, linking them to assemble a panel dataset spanning 1961–2023 comprising demographic and infrastructure variables.[1] We combined this data with satellite-derived flood exposure and official notification of villages included in the programme, allowing us to track the effect of the cash transfers on population change for both flooded and non-flooded villages, using a difference-in-differences framework.

What happened to village populations

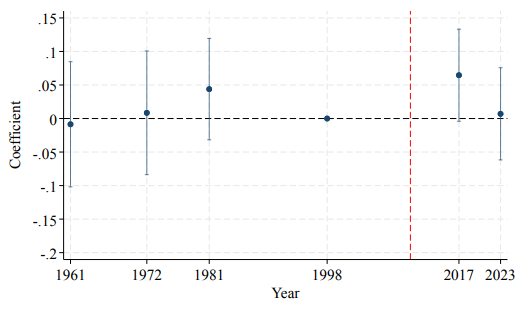

We first show that flooding itself is associated with a population decline (or a smaller population increase): heavily inundated villages experienced about a 17% decrease in population in later censuses relative to villages not experiencing floods.

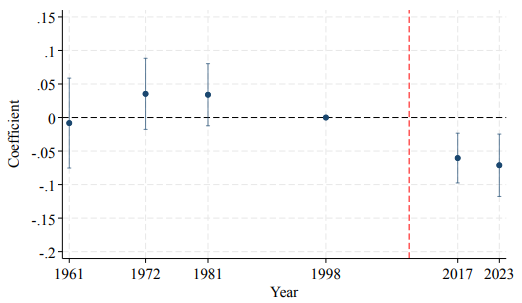

Figure 2: The effect of cash relief on population

(a) Flooded areas

(b) Non-flooded areas

The more surprising result is what happens where flooding did not occur. In non-flooded villages that nevertheless received cash transfers, the population is about 7% lower in the long run compared with non-flooded villages that did not receive cash. Because our outcome is the village population recorded in censuses, this is best interpreted as a large increase in permanent out-migration. Furthermore, the explanation for this decline, most consistent with our own data as well as the existing evidence, is that the cash transfers increased households’ liquidity, which allowed more of them to move permanently, most likely to cities or towns.

In flooded villages, by contrast, there is no net population effect of cash relief, consistent with two forces pulling in opposite directions and roughly cancelling out: cash makes moving easier, but it also raises the value of staying (through expected future support and the ability to rebuild locally). Cash transfers increase the value of staying in more flooded areas, given the higher probability of future flooding, and subsequent payments and benefits of in-situ adaptation.

Why migration effects differ between flooded and non-flooded areas

To understand the cancellation in flooded areas, we pair a simple conceptual framework with survey evidence.

First, cash relief changes beliefs about the state. Using the Pakistan Rural Household Survey (two years after the 2010 floods) and a World Bank survey after the 2022 floods, we find that recipients of the cash transfers are about six to seven percentage points more likely to expect government help in the case of future shocks and floods.

Second, relief facilitates in-situ adaptation: recipients are 33 percentage points more likely to report upgrading housing quality (for example moving to bricked construction) after the flood.

Third, the salience of risk is higher in flooded places. Households that experienced flooding in their surroundings are 27 percentage points more likely to believe that a similarly severe flood will occur again. When perceived risk is high, the benefits of rebuilding and the option value of staying (given expected future support) become more salient. In that case, the ‘stay’ forces strengthened by relief counterbalance the liquidity channel that encourages migration.

In non-flooded villages, perceived risk is lower. The belief and rebuilding channels are weaker, but the liquidity channel remains. The result is that the cash transfers cause a net increase in out-migration.

Implications for designing disaster relief

Two lessons follow for policy:

- Moral hazard is real, but it is not a sufficient reason to hold back cash transfers in low-income settings. In our setting, liquidity constraints are strong enough that relief can enable people to move even when it raises the payoff to staying. If policymakers worry that relief discourages relocation, they should also consider that relocation may be inefficiently low because households cannot finance it and that relief, especially in the form of cash, may enable relocation.

- Design choices can shift the balance between liquidity and moral hazard. Our framework implies that moral hazard concerns will likely be stronger when relief is provided in-kind (which offers less liquidity), so cash relief has the additional advantage of lower moral hazard on top of other well documented benefits.

References

Bin Khalid, M, and M Mattsson (2025), “The effect of disaster relief on climate adaptation: Evidence from floods in Pakistan,” Unpublished manuscript.

Bryan, G, S Chowdhury, and A M Mobarak (2014), “Underinvestment in a profitable technology: The case of seasonal migration in Bangladesh,” Econometrica, 82: 1671–1748.

Diop, B Z (2025), “Upgrade or migrate: The effects of fertilizer subsidies on rural productivity and migration,” Unpublished manuscript.

Gazeaud, J, E Mvukiyehe, and O Sterck (2023), “Cash transfers and migration: Theory and evidence from a randomized controlled trial,” Review of Economics and Statistics, 105: 143–157.

Henkel, M, E Kwon, and P Magontier (2024), “The unintended consequences of post-disaster policies for spatial sorting,” Unpublished manuscript.

Hsiao, A (2025), “Sea level rise and urban adaptation in Jakarta,” Unpublished manuscript.

Hunt, S, D Glyn, et al. (2011), “Evaluation of the Pakistan Watan Card programme,” Unpublished manuscript.

IPCC (2021), "Climate change 2021: The physical science basis."

Pang, X, and P Sun (2022), “Moving into risky floodplains: The spatial implication of flood relief policies,” Unpublished manuscript.

Pople, A, R Hill, S Dercon, and B Brunckhorst (2024), “The importance of being early: Anticipatory cash transfers for flood-affected households,” Unpublished manuscript.

Pople, A C, P Premand, S Dercon, M Vinez, and S Brunelin (2025), “The earlier the better? Cash transfers for drought response in Niger,” Unpublished manuscript.

Tiwari, S, and P C Winters (2019), “Liquidity constraints and migration: Evidence from Indonesia,” International Migration Review, 53: 254–282.

World Bank (2010), "Pakistan floods 2010: Preliminary damage and needs assessment."