The majority of households in rural Uganda are involved in agriculture but have no insurance against crop failure or price shocks. Evidence suggests that awareness programmes that help farmers understand potential negative outcomes—perhaps through simulations or testimonials from peers who have experienced losses—could increase formal insurance uptake.

Editors' note: This column is published in collaboration with the International Economic Association’s Women in Leadership in Economics initiative, which aims to enhance the role of women in economics through research, building partnerships, and amplifying voices.

Poor households in low-income countries face numerous risks, from extreme weather events to illness and crop failure. With limited savings and assets, even small shocks can have devastating consequences on welfare. While formal insurance products can potentially help mitigate these risks, their uptake remains remarkably low among rural smallholder farmers, who instead primarily rely on informal risk-sharing networks. This pattern persists despite evidence suggesting that informal insurance mechanisms provide incomplete coverage against shocks. These shocks translate into shortfalls in income and consumption (Karlan et al. 2014, Morduch 1999).

Studying the impact of insurance on farmers’ economic behaviour

In Nanyiti and Pamuk (2025), we focus on smallholder farmers in rural Uganda and examine how different insurance arrangements affect their economic behaviour and decision-making. Uganda provides an ideal setting to explore these questions, as only 1% of adults have formal insurance coverage, despite 67% of households depending on agriculture for their livelihoods. By comparing behaviour under formal insurance (provided by registered companies) versus informal insurance (peer-to-peer transfers), we gain insights into why formal insurance uptake remains low and how farmers respond to different risk management options.

Using a real effort task experiment, we investigate whether the incentives created by these different insurance arrangements influence productivity and risk management decisions. Our findings reveal important behavioural responses that help explain observed patterns in insurance uptake and suggest potential approaches for improving the design and adoption of formal insurance products. We find that farmers exerted less effort under informal insurance but not under formal insurance coverage, and increased their level of formal insurance coverage after experiencing a bad outcome.

While rural households rely on informal insurance–typically in-kind or cash peer-to-peer transfers–to mitigate the shortfalls (Arnott and Stiglitz 1991, Nanyiti et al. 2019), these mechanisms provide limited cover. Formal insurance, provided by registered companies, requires users to pay a premium every period and receive a pay-out in the event of a bad outcome.

However, formal insurance uptake remains low among smallholder farmers, and there is an ongoing debate about how to increase adoption (Berg et al. 2022, Ceballos and Kramer 2019, Dercon et al. 2014, Karlan et al. 2014, Kramer et al. 2022, Osiemo et al. 2025, Rudramuni 2024, Vargas and Viceisza 2012).

Most households in rural Uganda depend on agriculture, but have no formal insurance

Most households in Uganda (67%) depend on agriculture as their main livelihood (NPA 2020), engaging in livestock production and crop cultivation. These households face various risks, including agricultural produce price fluctuations, crop failures due to floods or droughts, and injury, illness, or death of a household member.

Evidence suggests that most households have no formal insurance against crop failure or price shocks, while few households have savings to cope with these shocks (Finscope 2018). The number of households covered by formal insurance is negligible. Only 1% of the Ugandan adult population had formal insurance coverage as of 2018 (Finscope 2018).

Efforts to advance insurance products in Uganda are in the pilot stage (Agro Consortium 2020, eLEAF 2022), but even for the beneficiary communities, uptake is low due to high premiums. Lack of familiarity and understanding of these products also limits their uptake (Ackah and Owusu 2012, Belissa et al. 2019, Eschborn 2021, Liu et al. 2019, World Bank, 2019).

The majority of households rely on informal insurance networks such as savings and loan associations and credit cooperatives. Many are also members of Village Savings and Loan Associations (VSLAs) and burial societies; others borrow money from friends, relatives, and lenders to cope with shocks (Finscope 2018).

Using a task experiment to study different insurance arrangements

We used a real effort task experiment with good and bad outcomes. Participants were assigned to one of two groups: the formal insurance group (120 participants) and the informal insurance group (160 participants).

The formal insurance group members had access to an insurance product for which they paid a premium every round and received a payment in rounds when they experienced a bad outcome. Members played three versions of the experiment: the no insurance, compulsory insurance, and voluntary insurance case.

Each informal insurance group member was paired with another informal insurance group member. Each round, members with good outcomes made transfers to partners with bad outcomes. These members also played three versions of the experiment.

Our results show that effort under voluntary informal insurance was lower than that under no insurance. Under voluntary informal insurance, participants follow the norms and share their earnings with peers with bad outcomes. The effort under compulsory informal insurance, compulsory formal insurance, and voluntary formal insurance was the same as under no insurance.

Awareness programmes on the potential gains of insurance may increase uptake

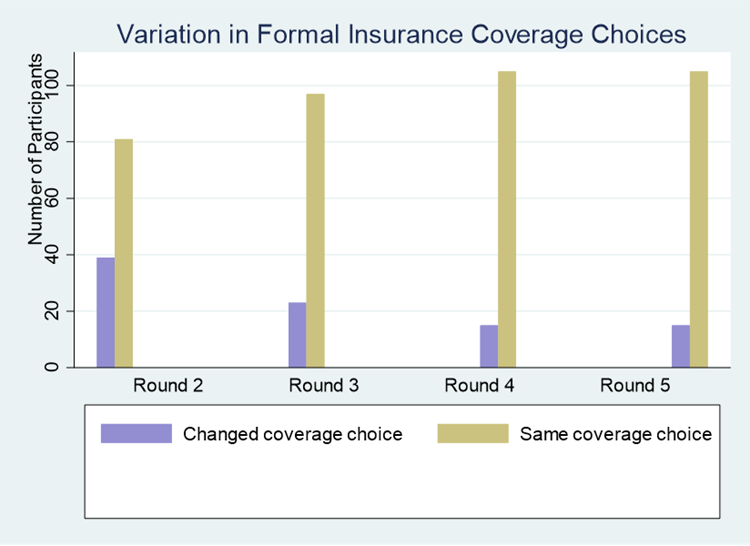

For the voluntary formal insurance, we find that participants increased their level of formal insurance coverage after experiencing a bad outcome. Coverage choices varied considerably across rounds. Experiencing low earnings due to a bad outcome makes the risk in the effort task more understandable to participants, causing them to choose high coverage levels in later rounds.

Figure 1: Variation in coverage choices under the voluntary formal insurance treatment

Implications for agricultural policy in developing countries

Our findings illuminate the complex relationship between insurance mechanisms and economic behaviour in rural Uganda. Most notably, we find that farmers exerted less effort under informal insurance arrangements but maintained their effort levels under formal insurance. Interestingly, we also observed that farmers increased their formal insurance coverage after experiencing negative outcomes. This learning process indicates that first-hand experience with risk may be a powerful driver of insurance demand. The considerable variation in formal insurance coverage choices across experimental rounds suggests that farmers are actively adjusting their risk management strategies based on their experiences.

These results have important policy implications. They suggest that awareness programmes that help farmers understand potential negative outcomes—perhaps through simulations or testimonials from peers who have experienced losses—could increase formal insurance uptake. Financial education that makes their risks more tangible and understandable may be more effective than traditional information campaigns alone.

More broadly, our research contributes to the ongoing debate on how to improve formal insurance adoption among smallholder farmers in developing countries. It suggests that policy interventions should consider not only the economic but also the behavioural factors that influence insurance decisions. As climate change increases the frequency and severity of agricultural shocks, developing effective and widely adopted risk management tools for smallholder farmers becomes increasingly crucial for sustainable rural development.

References

Ackah, C and A Owusu (2012), “Assessing the knowledge of and attitude towards insurance in Ghana”, Unpublished manuscript.

Agro Consortium (2020), “To what extent are smallholder farmers being protected against weather and climate related shocks?”.

Arnott, R and J E Stiglitz (1991), “Moral hazard and nonmarket institutions: Dysfunctional crowding out of peer monitoring?”, American Economic Review, 81(1): 179–190.

Belissa, T, E Bulte, F Cecchi, S Gangopadhyay, and R Lensink (2019), “Liquidity constraints, informal institutions, and the adoption of weather insurance: A randomized controlled trial in Ethiopia”, Journal of Development Economics, 140: 269–278.

Berg, E, M Blake, and K Morsink (2022), “Risk sharing and the demand for insurance: Theory and experimental evidence from Ethiopia”, Journal of Economic Behavior & Organization, 195: 236–256.

Ceballos, F and B Kramer (2019), “From index to indemnity insurance using digital technology: Demand for picture-based crop insurance”, Unpublished manuscript.

Dercon, S, R V Hill, D Clarke, I Outes-Leon, and A S Taffesse (2014), “Offering rainfall insurance to informal insurance groups: Evidence from a field experiment in Ethiopia”, Journal of Development Economics, 106: 132–143.

eLEAF (2022), “Index insurance in Uganda”.

Hazell, P, A Jaeger, and R Hausberger (2021), "Innovations and emerging trends in agricultural insurance for smallholder farmers: An update", GIZ.

Finscope (2018), "Report on uptake of insurance services in Uganda", Financial Sector Deepening Uganda.

Karlan, D, R Osei, I Osei-Akoto, and C Udry (2014), “Agricultural decisions after relaxing credit and risk constraints”, Quarterly Journal of Economics, 129(2): 597–652.

Kramer, B, P Hazell, H Alderman, F Ceballos, N Kumar, and A G Timu (2022), “Is agricultural insurance fulfilling its promise for the developing world? A review of recent evidence”, Annual Review of Resource Economics, 14: 291–311.

Liu, X, Y Tang, J Ge, and M J Miranda (2019), “Does experience with natural disasters affect willingness-to-pay for weather index insurance? Evidence from China”, International Journal of Disaster Risk Reduction, 33: 33–43.

Morduch, J (1999), “Between the state and the market: Can informal insurance patch the safety net?”, World Bank Research Observer, 14(2): 187–207.

Nanyiti, A, H Pamuk, and E Bulte (2019), “Tied labour, savings and rural labour market wages: Evidence from a framed field experiment”, Journal of African Economies, 28(4): 435–454.

Nanyiti, A and H Pamuk (2025), “Moral hazard incentives under formal insurance and informal insurance: Evidence from a framed field experiment”, Journal of African Economies, 34(1): 80–115.

National Planning Authority (2020), "Third National Development Plan (NDPIII) 2020/21–2024/25", Government of Uganda.

Osiemo, J, F Cecchi, E Bulte, and C Mwongera (2025), “Experiential learning, narrative-based learning, and insurance adoption: Experimental evidence from Kenya”, American Journal of Agricultural Economics (forthcoming).

Rudramuni, P (2024), “Digitizing crop insurance: Unveiling opportunities, obstacles, and charting the future of crop insurance”, Journal of Philanthropy and Marketing, 4(1): 464–471.

World Bank (2019), "Towards a scale-up and sustainable agricultural finance and insurance in Uganda".

Vargas, R and A H Viceisza (2012), “A field experiment on the impact of weather shocks and insurance on risky investment”, Unpublished manuscript.