Evidence from Mexico shows that extreme heat leads to increased delinquency rates, particularly among small and medium-sized enterprises. Policy must address these risks, coupling climate resilience with enhanced credit access for vulnerable firms.

Editors' note: This article originally appeared on VoxEU, where it was published in collaboration with the International Economic Associations’ Women in Leadership in Economics initiative, which aims to enhance the role of women in economics through research, building partnerships, and amplifying voices.

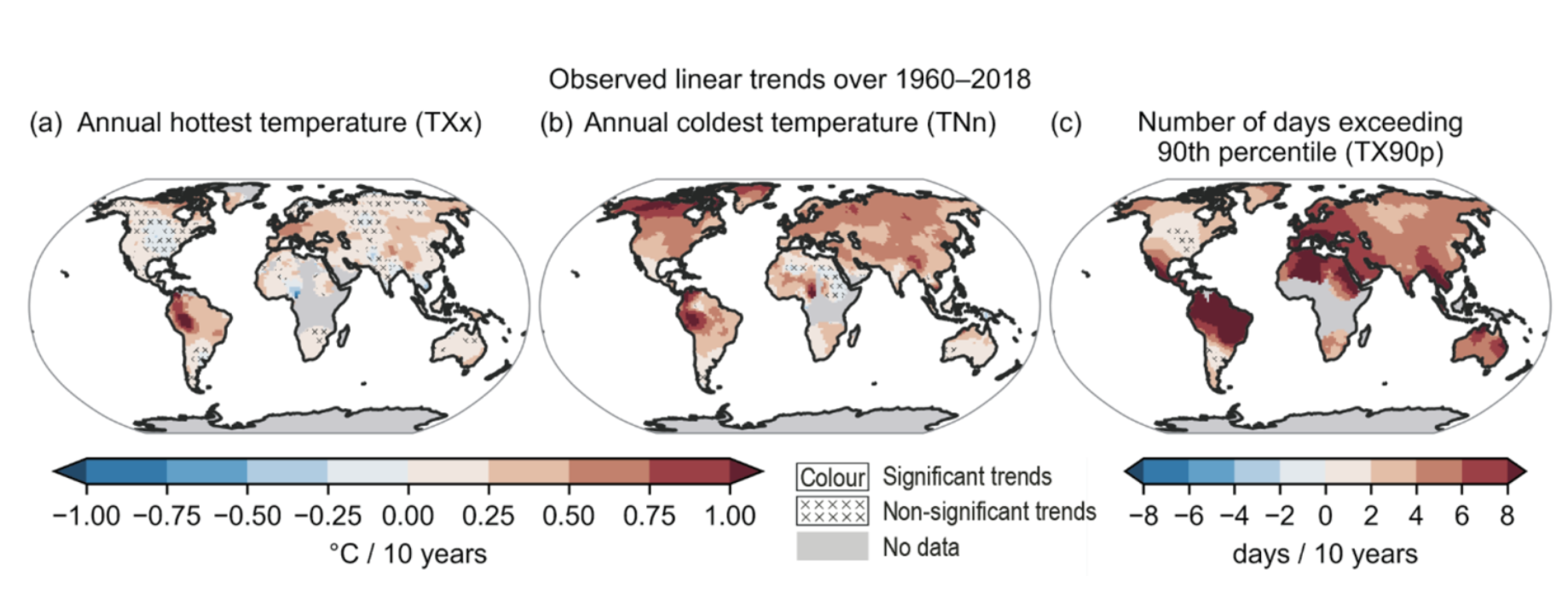

Climate change is expected to increase the frequency and intensity of extreme weather events. Heatwaves are a growing concern, each year breaking temperature records (IPCC 2021). Figure 1 displays analyses of the most recent assessment report of the International Panel on Climate Change (IPCC AR6). During the past half a century, there has been a consistent increase in the number of days above the 90th percentile of the local distribution. In agriculture, it will not come as a surprise that research has found that crop yields are negatively impacted by deviations from optimal conditions for plant growth. However, the economic impacts of a warming world extend beyond the agricultural sector: high temperatures make work unpleasant and make some goods and services more attractive than others. High temperatures also make people more aggressive and worse at making decisions. Economists have found that these impacts translate into firms’ profits through reduced labour productivity, increased worker absenteeism, and shifts in local demand. Operational costs also rise if firms spend resources to mitigate some of these impacts (for example, using more air conditioning and shorter shifts for exhausted workers). In a recent Vox column, Ponticelli et al. (2023) discuss empirical findings of plant productivity decreasing with temperature in the US, leading in the medium run to smaller plants closing, increasing concentration in the manufacturing sector.

Figure 1 Linear trends over 1960–2018 for three temperature extreme indices: Annual maximum daily maximum temperature (panel a), annual minimum daily minimum temperature (panel b), and annual number of days when daily maximum temperature exceeds its 90th percentile from a base period of 1961–1990 (panel c)

Source: IPCC (2021) Figure 11.9.

How will climate change impact firms in developing countries?

Central banks and other financial institutions are increasingly concerned about the impact of these shocks on the financial sector (Reinders et al. 2023). The effect of unfavourable weather on costs and demand may create liquidity shortages for firms that could cause solvency problems. In developing countries, several conditions suggest that firms may be more vulnerable. Suppose, for instance, the defaults generated by the shock increase lenders’ uncertainty about borrowers’ ability to repay their loans in the future. In that case, they might charge higher interest rates for new loans and reduce credit availability, increasing firms’ credit constraints. This is especially relevant for credit types for which the ability to repay is more uncertain, such as new small and medium-sized enterprises (SMEs) with scarce credit history, or for firms needing investment loans, which have longer maturity and higher uncertainty about future profits that the investment would generate. Overall, the impact of independent and identically distributed shocks could be longer-lived when hitting credit markets that deal less efficiently with informational asymmetries such as those in low- and middle-income economies.

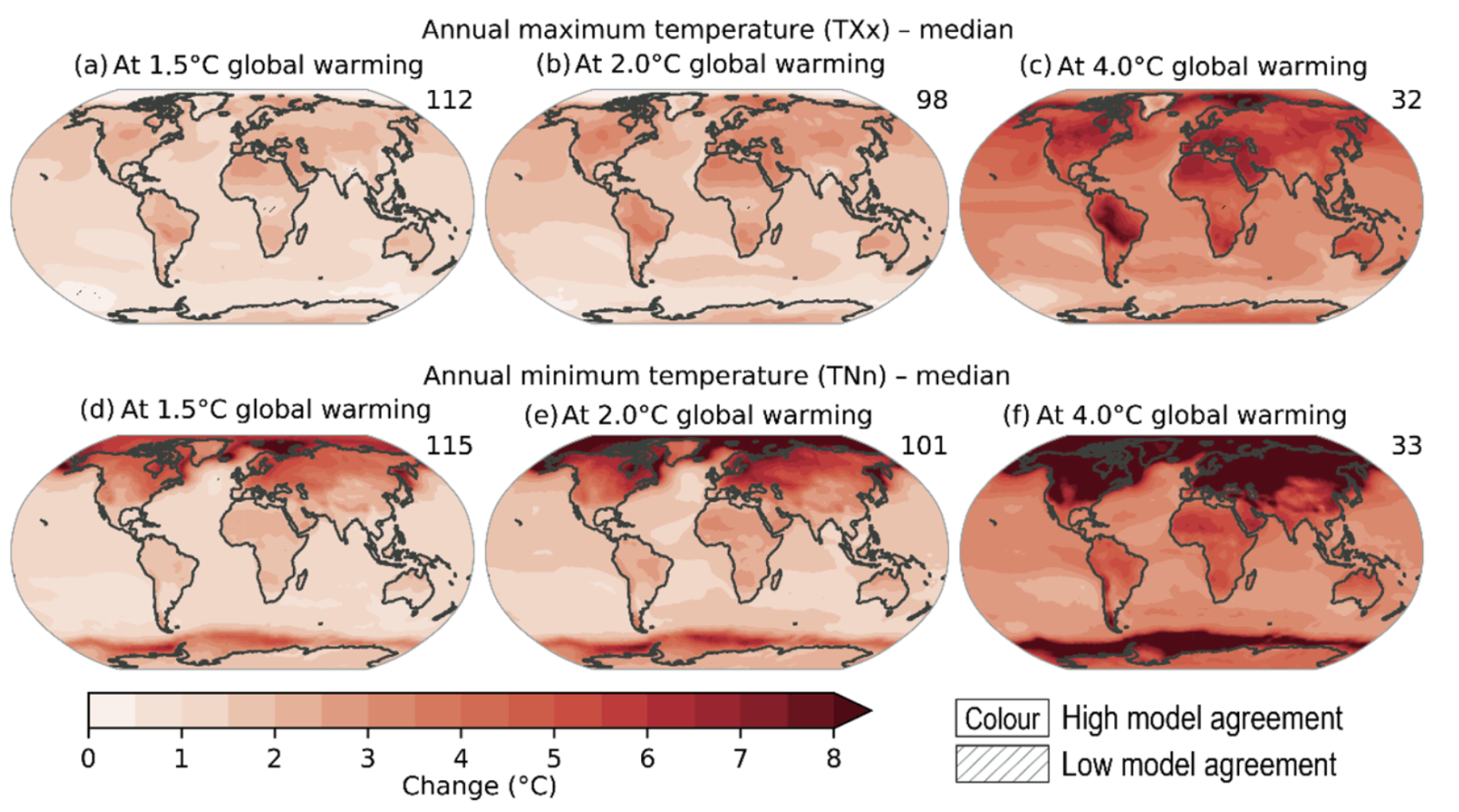

Moreover, it is important to note that warming is not projected to affect countries homogeneously. Most developing countries are in regions with higher baseline temperatures. Hence, even uniform warming could have disparate impacts due to hard biological limits for agricultural yield and human health. However, current models project significant heterogeneity in local warming, as shown in Figure 2. For all the reasons above, understanding the impacts of extreme weather events on the financial sector in developing countries is of high policy relevance.

Figure 2 Projected changes in annual maximum temperature (panels a to c) and annual minimum temperature (panels d to f) at 1.5°C, 2°C, and 4°C of global warming compared to the 1850–1900 baseline

Source: IPCC (2021) Figure 11.11.

In our recent study (Aguilar-Gomez et al. 2024), my co-authors and I employ a robust methodology and a comprehensive dataset encompassing information on all loans extended by commercial banks to private firms in Mexico over a span of nearly a decade. This allows us to delve into potential climate vulnerabilities within the Mexican financial system. Specifically, we estimate the impact of unexpected days above the 95th percentile of the temperature distribution on firms’ financial distress, with our primary focus on the delinquency rate, measured as the ratio of non-performing loans to total outstanding credit in a county.

Climate vulnerabilities within the Mexican financial system

Our study reveals three main findings:

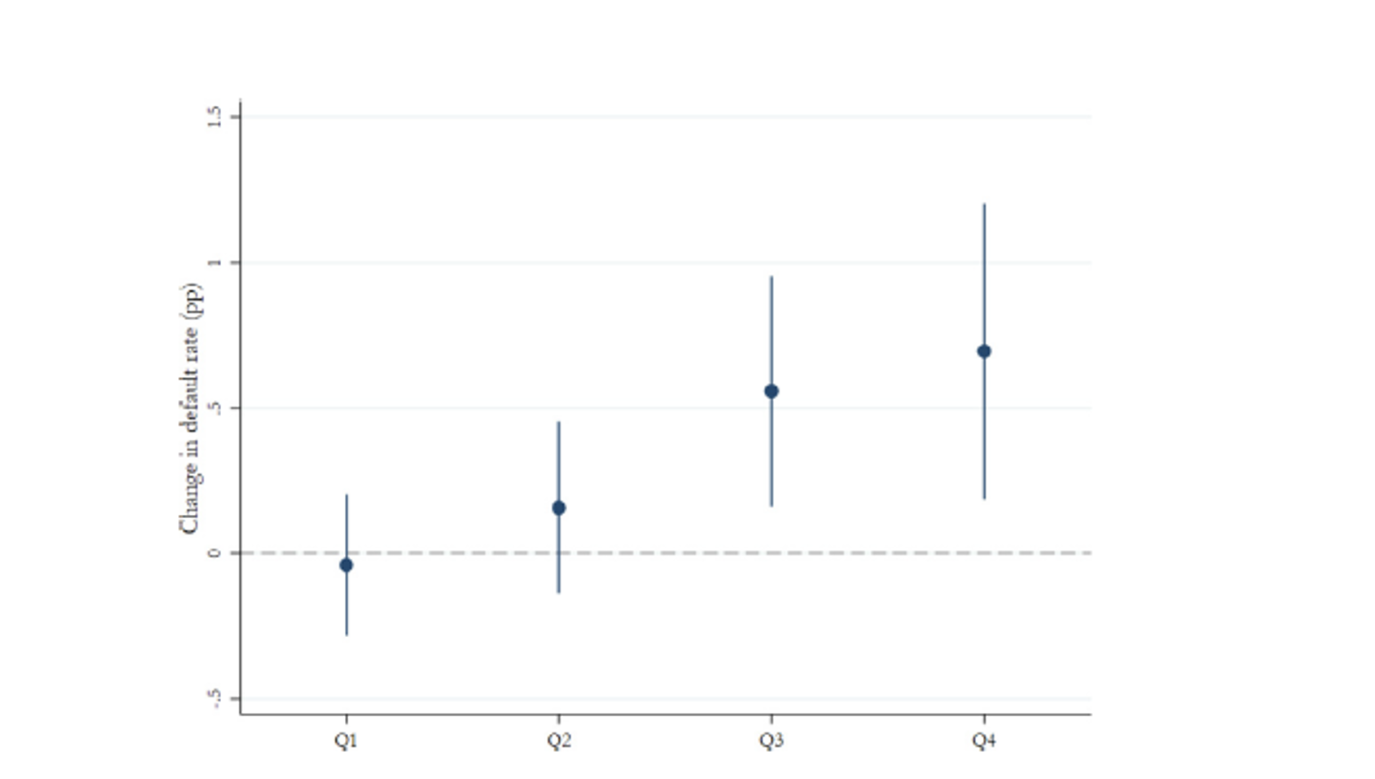

- Extreme heat in a municipality raises its credit delinquency rate, an effect driven entirely by small firms defaulting on their loans. In terms of magnitudes, ten unusual days of extreme heat during the previous three months increase the delinquency rate of SMEs by 0.17 percentage points, equivalent to 4.4% of the observed sample mean (3.9%). Figure 3 displays this phenomenon by plotting the relationship between the default rate and the days of extreme heat in the previous quarter. It also shows that the heatwave has to be long enough to cause significant damage (i.e. 11 days). This finding is consistent with the notion that SMEs in developing countries are less equipped to cope with extreme temperatures, making it more difficult to access further credit in times of financial stress. Consistent with theory and previous research (e.g. Schlenker and Roberts 2009, Blanc and Schlenker 2017), we find that the negative effect of extreme heat is stronger in agriculture.

- Regional economic composition matters. Extreme heat also has sizeable effects on non-agricultural industries in regions with a sufficiently large proportion of agricultural workers. Furthermore, effects in the non-agricultural sector are concentrated in services and retail, that is, non-tradable sectors that rely heavily on local demand. The findings suggest that adverse conditions in agriculture lead to reduced local spending, causing spillover effects into non-agricultural industries.

- By employing diverse market integration measures in agriculture production, we find that weather shocks have a stronger effect on credit default among agricultural firms in more integrated markets. This result is consistent with the notion that a price surge partially offsets a decrease in local production caused by extreme weather in more isolated markets. Interestingly, this evidence implies that financial institutions may be less vulnerable to temperature shocks in relatively isolated markets.

- One might be less concerned about these results if our data indicated that firms recover and do not carry longer-run implications of short-run shocks. We find that temperature shocks reduce the number of firms with access to credit in the affected municipality for some time. Credit composition also changes after the weather shock: we find a decrease in credit for investments and new firms, along with a rise in interest rates for new loans. Specifically, exposure to extreme heat translates into increased interest rates for new loans within the same firm, heightened collateral requirements, and declined credit access. Together, the firm- and market-level results show that in response to shocks, banks tighten credit for two to three quarters, hindering access to financial flexibility when firms most need it. These findings contrast with those found in advanced economies, particularly the US, where the evidence suggests that firms use credit lines to manage liquidity during extreme weather (Brown et al. 2021, Collier et al. 2020). Mexican SMEs seem unable to use new loans similarly.

Figure 3 Effects of extreme temperatures on delinquency rates

Notes: The figure shows the results separating quarterly days of exposure to extreme heat into four quartiles. The categorization is as follows: the first quartile encompasses days with extreme heat ranging from 1 to 3 days (Q1), the second quartile includes 4 to 10 days (Q2), the third quartile covers 11 to 31 days (Q3), and the fourth quartile comprises more than 31 days (Q4). The point estimates measure the effect of exposure to certain number days of extreme heat with respect to the base category (0).

Conclusion and policy recommendations

Our findings provide empirical support to the concerns regarding the potential effects of extreme weather on the financial system described, for instance, in Reinders et al. (2023). In response to accumulating evidence, regulatory authorities, and central banks worldwide are calling for improvements in measuring and monitoring climate risks, such that relevant actors can manage such risks (Litterman et al. 2020). One policy implication of our results is that policies seeking to reduce direct exposure to climate shocks in banks’ balance sheets would ideally be implemented along with other complementary policies, especially in developing countries. Such policies could compensate for unintended consequences by deepening small and medium firms’ access to credit, especially when firms are coping with the impact of weather shocks.

References

Aguilar-Gomez, S, E Gutierrez, D Heres, D Jaume and M Tobal (2024), “Thermal stress and financial distress: Extreme temperatures and firms’ loan defaults in Mexico”, Journal of Development Economics 168, 103246.

Blanc, E and W Schlenker (2017), “The Use of Panel Models in Assessments of Climate Impacts on Agriculture”, Review of Environmental Economics and Policy 11(2): 258–279.

Litterman, R, C E Anderson, N Bullard et al. (2020), Managing climate risk in the US financial system, U.S. Commodity Futures Trading Commission.

IPCC (2021), Climate Change 2021: The Physical Science Basis. Contribution of Working Group I to the Sixth Assessment Report of the Intergovernmental Panel on Climate Change, Cambridge University Press

Ponticelli, J, Q Xu and S Zeume (2023), “Temperature and local manufacturing concentration”, VoxEU.org, 9 October.

Reinders, H J, D Schoenmaker and M V Dijk (2023), “Climate risk stress tests underestimate potential financial sector losses”, VoxEU.org, 28 June.

Schlenker, W and M J Roberts (2009), “Nonlinear temperature effects indicate severe damages to U.S. crop yields under climate change”, Proceedings of the National Academy of Sciences 106(37): 15594–15598.