The introduction of mobile money promoted migration out of rural areas by easing long-distance transfers and increasing resilience

M-PESA is the most popular mobile money platform in Africa. It was launched in Kenya in March 2007 and quickly became a viral success. The so-called ‘mobile money revolution’ that followed has since attracted substantial attention from economists and policymakers, as described by Suri (2017).

Mobile money as an opportunity for financial inclusion

Financial inclusion is an important driver of economic development. It remains a challenge in many parts of the world, however, and sub-Saharan Africa (SSA) is no exception. Despite the improvements made in recent years, access to financial services in SSA is still limited. Only around one third of the adult population in the region had a bank account in 2017.1 In addition, the costs and risks associated with money transfers in this region are substantial. The average cost of sending remittances to countries in the SSA is higher than anywhere else in the world, and the top ten most expensive remittance corridors in the world are all within Africa.2

At the same time, mobile phone usage in SSA has skyrocketed in the past decades and its potential in areas as diverse as financial inclusion, healthcare, and agricultural modernisation is revolutionising the African landscape. Mobile money is a transformative idea as it makes use of basic mobile phone technology already owned by most of the poor in the world, while also providing a simple way to perform financial transactions without the need for formal bank accounts.

The economic impact of mobile money

A body of evidence has recently been produced on the economic impacts of mobile money, linking it to consumption smoothing and risk sharing (Jack and Suri 2014, Riley 2018, Lee et al. 2021), and reduced poverty and occupational change, particularly for women (Suri and Jack, 2016). Mobile money has also been documented to promote educational enrolment, agricultural modernisation, and private sector development (Jack and Habyarimana 2018, Bastian et al 2018, Batista et al. 2019, Aggrawal et al. 2020, Batista and Vicente 2020). In different settings, Blumenstock et al. (2018) showed that mobile salary payments can increase savings due to default enrolment; however, De Mel et al. (2020) found that offering reduced fees to make mobile deposits did not increase household savings.

In a recent paper (Batista and Vicente 2021), we measure the economic impact of introducing a mobile money service in rural areas of southern Mozambique. The paper presents, to the best of our knowledge, the first experimental evidence on the impact of introducing access to mobile money in rural locations that previously had no formal financial services available.

Methodology

The field experiment followed 102 rural enumeration areas in the provinces of Maputo-Province, Gaza, and Inhambane in southern Mozambique. The experimental intervention was implemented in half of these villages, which were chosen at random. The intervention included the recruitment and training of one mobile money agent in each treatment location, explanations of mobile money services given to the local population through performances at community theatres and meetings, and a set of individual dissemination activities, which included support to individuals as they registered themselves for mobile money services and made trial transactions.

The outcomes of the experiment were measured using a three-year panel of administrative data, including all mobile money transactions performed by individuals in treatment and control locations, geo-referenced evapotranspiration data to measure village flood shocks, a panel of household surveys conducted before and after the baseline, and behavioural data purposely designed to predict the adoption of mobile money as a transfer and savings mechanism.

Findings

Mobile money adoption

We find significant levels of adoption of the mobile money service among rural households in treatment locations: nearly 87% of the treated individuals in our sample used the service in the three years after it was introduced, compared to only 1.8% of control individuals. Three years after the intervention, 53% of treated individuals were still conducting mobile money transactions. The most common transactions were buying airtime and receiving transfers – although payments also became more frequent towards the end of our measurement period.

Mobile transfers and migrant remittances

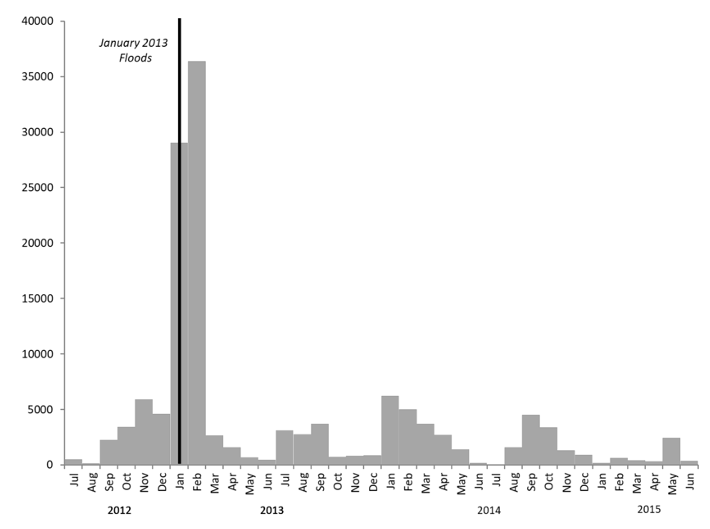

Figure 1 displays the striking positive response of mobile money transfers received by treated rural households in our sample after large floods affected two-thirds of the villages in our sample six months after the introduction of mobile money services.

Figure 1 Total value of monthly mobile money transfers received by all sampled households (in Mozambican meticals)

Source: Administrative data provided by the mobile money operator.

Treated households affected by idiosyncratic shocks also received increased mobile transfers relative to those in the control group. This positive effect of both village-level and household-level idiosyncratic shocks on mobile transfers was even larger for overall migrant remittances received by rural households in villages with access to mobile money services. In addition, over time, there was also an increase in migrant remittances received by treated households unaffected by negative shocks.

Consumption expenditure

Access to mobile money translated into insurance against both aggregate shocks (village-level floods) and idiosyncratic shocks (household-level health, death and unemployment). Although mobile money availability did not significantly affect the consumption expenditure of households unaffected by negative shocks, it increased the consumption expenditure of households coping with the additional expenses incurred because of floods, illnesses, and funerals. This stronger resilience to negative shocks translated into lower vulnerability, particularly to hunger episodes, and significant positive effects on subjective wellbeing.

Productive activity and investment

We find evidence of reduced agricultural activity and investment in households with access to mobile money, with some business activity also being negatively affected. These negative effects were particularly strong in the second year after the introduction of mobile money.

Migration out of rural areas

We observe an increase in migration out of rural areas when mobile money is available. While this migration is concentrated in areas that suffered from village-level floods in the first year after mobile money was made available, this effect is strengthened in the second year, also in treated areas not affected by floods.

This result is consistent with the fact that mobile money reduced the transaction costs of immediate long-distance transfers, thereby improving the possibility of long-distance insurance, and allowing household members to invest in migration instead of in less productive activities such as subsistence agriculture.

Lessons from this mobile money experiment in Mozambique

Overall, our experimental evidence shows that providing access to mobile money in poor rural areas may open the door to household migration with the objective of taking higher productivity occupations outside of rural areas, instead of investing in (subsistence) agriculture. In this sense, our work shows how financial inclusion can accelerate urbanisation and structural change as a path for improved welfare.

Rural areas of Mozambique are still considerably underserved in terms of financial services and subsistence agriculture is dominant. While there are many similar regions in sub-Saharan Africa where our findings are likely to be relevant, it will be interesting to evaluate whether this same mechanism holds in different parts of the world at different stages of development.

References

Aggarwal, S, V Brailovskaya and J Robinson (2020), “Cashing in (and out): Experimental evidence on the effects of mobile money in Malawi”, AEA Papers and Proceedings 110: 599-604.

Bastian, G, I Bianchi, M Goldstein and J Montalvao (2018), “Short-term impacts of improved access to mobile savings, with and without business training: Experimental evidence from Tanzania”, Center for Global Development Working Papers 478.

Batista, C and P C Vicente (2020), “Improving Access to Savings through Mobile Money: Experimental Evidence from African Smallholder Farmers”, World Development 129, 104905.

Batista, C and P C Vicente (2021), "Is mobile money changing rural Africa? Evidence from a field experiment", Nova SBE and NOVAFRICA, mimeograph.

Batista, C, S Sequeira and P C Vicente (2019), “Closing the Gender Gap in Financial Management and Performance: Evidence from an Experiment on Training and Mobile Savings”, Nova SBE and LSE, mimeograph.

Blumenstock, J, M Callen and T Ghani (2018), “Why do defaults affect behavior? Experimental evidence from Afghanistan”, American Economic Review 108(10): 2868-2901.

De Mel, S, C McIntosh, K Sheth and C Woodruff (2020), “Can Mobile-Linked Bank Accounts Bolster Savings? Evidence from a Randomized Controlled Trial in Sri Lanka”, Review of Economics and Statistics, 1-45.

Jack, W and T Suri (2014), “Risk sharing and transactions costs: Evidence from Kenya's mobile money revolution”, American Economic Review 104(1): 183-223.

Lee, J N, J Morduch, S Ravindran, A Shonchoy, and H Zaman (2021), “Poverty and migration in the digital age: Experimental evidence on mobile banking in Bangladesh”, American Economic Journal: Applied Economics 13(1): 38-71.

Riley, E (2018), “Mobile money and risk sharing against village shocks”, Journal of Development Economics 135: 43-58.

Suri, T and W Jack (2016), “The long-run poverty and gender impacts of mobile money”, Science, 354(6317): 1288-1292.

Suri, T (2017), “Mobile money”, Annual Review of Economics 9: 497-520.

Endnotes

1 According to the World Bank’s Global Findex database.

2 According to the World Bank’s Remittance Prices Worldwide database.