Many formal firms in sub-Saharan Africa only register after operating informally for a few years in order to grow and overcome financial constraints. Evidence from Nigeria suggests that taxes and enforcement – rather than registration costs alone – are the most effective levers for reducing informality without harming aggregate output.

Editor’s note: For a broader synthesis of themes covered in this article, check out Issue 2 of our VoxDevLit on Informality.

Informality is large and persistent in low- and middle-income countries. Economists and policymakers care about informality because of its detrimental effects on taxes and public goods provision, social safety nets, market efficiency, and allocation of resources (La Porta and Shleifer 2014, 2008, Levy 2008, Maloney 2004, Farrell 2004). A vast evidence base has endeavoured to understand informality, but it is mostly treated as a static and permanent state. Yet many formal firms start life informally.

A missing margin: Formal firms that started out informal

In Nigeria, nearly one in three formal firms (about 31%) report that they were not registered at the start but formalised later. These ‘switchers’ account for over a quarter of employment among micro, small and medium-sized formal firms. They start smaller, grow somewhat more slowly, and face tighter access to bank credit than firms that were registered from day one. Switching is common across sub-Saharan Africa, where switchers exceed 10% of formal firms in 27 countries and more than 20% in 10 of them. The share of switchers tends to be higher in countries with more severe financial constraints and lower where taxes are higher. In recent work (Adom 2026), I study who switches, as well as when, why, and how different policies can affect the creation of new formal firms and the formalisation of existing informal firms.

Modelling informality as a stepping stone

I built a forward-looking model in which entrepreneurs choose each period to operate formally or informally, subject to financial constraints and enforcement risk that increases with firm size. Formal firms pay recurrent taxes and enjoy looser collateral constraints, while informal firms avoid taxes but face a rising probability of detection and fines as they scale. Formalisation is a one-off decision with a sunk cost.

For many capable but asset-poor entrepreneurs, informality is a stepping stone. They start small and off the books, accumulate assets, then formalise when the costs of staying informal outweigh the costs of being formal. Others never switch because they remain too unproductive or cash‑constrained. When calibrated to Nigeria’s data, the model shows that absent financial constraints most productive entrepreneurs would formalise early and the transition margin becomes quantitatively negligible.

Assessing different formalisation policies

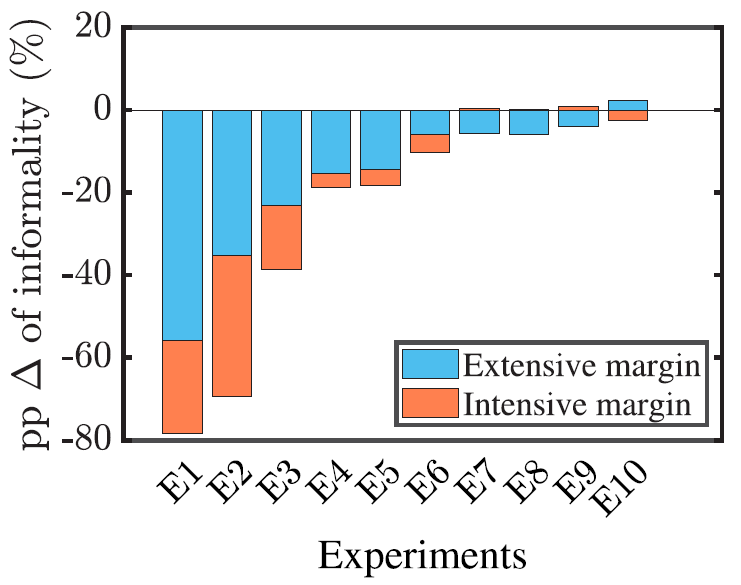

The calibrated model is used to quantitatively assess many experiments. The results are summarised in Figure 1.

- Cutting taxes. Taxes are certainly the most important cost of formality. Unlike formalisation costs, taxes are recurrent and the entrepreneur commits to paying them in future. What if taxes were lower? Would most firms register from the start or would existing ones formalise? In the model, halving profit taxes reduces informality by 39 percentage points (p.p.), with 23 p.p. from formal entry and 16 p.p. from switching. Output rises by 33% as the economy shifts significantly from informality, and government revenue increases by about 8 p.p. of GDP, assuming that all formal firms comply with taxes.

- Enforcement. It has been argued in the evidence base that enforcement is the most effective, if not the only, way to significantly curb informality. But it may induce production loss (Ulyssea 2018). In this analysis too, perfect detection cuts informality by 69 p.p., with no negative effect on GDP. It can still hurt those entrepreneurs who would be better off under informality.

- Lower cost registration. Reducing one-time registration costs by 10% barely affects informality. General equilibrium effects on factor prices offset initial gains.

- Easing finance. Removing financial constraints for formal firms reduces informality by about 6 p.p. and raises output by 64%. Removing them for informal firms lowers informality by about 3 p.p.

- Productivity. What if entrepreneurs were more productive? Doubling average productivity reduces informality by around 18 p.p. and raises output and government revenue significantly. But informality persists unless enforcement improves. Therefore, the experiment suggests that informality will not resolve by itself even as development unfolds and aggregate productivity increases as conjectured in La Porta and Shleifer (2008, 2014).

Figure 1: Extensive and intensive margins of informality

Notes: Figure shows the contribution of the extensive margin (i.e. creation of new formal firms) and the intensive margin (i.e. transition of existing informal firms to formality) under different policy experiments: E1 Doubling Avg. productivity & perfect enforcement, E2 Perfect enforcement, E3 Reduction of revenue tax by half, E4 Doubling fines on caught informal firms, E5 Doubling average productivity, E6 Reduction of payroll tax by half, E7 No financial constraints, E8 No financial constraints only for formal firms, E9 No financial constraints only for informal firms, E10 Reduction of formalisation cost by 10%.

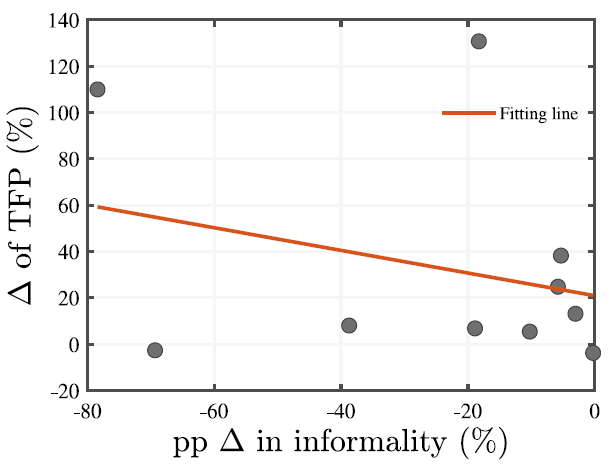

Informality and productivity

In most experiments, the informality rate decreases while aggregate TFP increases, confirming a negative relationship between informality and aggregate TFP as shown in Figure 2. But the correlation is far from perfect. The effect of a change in informality on TFP seems to depend on the underlying reason for the change in informality. Enforcement significantly affects informality but has limited impact on TFP. On the other hand, easing financial constraints can have a modest impact on informality but a significant effect on TFP.

Figure 2: Effect of change in informality on aggregate TFP

Policies for the informal sector

The results of the model show that informality may be reduced mainly through the creation of new formal firms but also through the formalisation of existing informal ones. Popular policies like the reduction of formalisation costs and efforts to support access to financing have less impact on informality. Slashing informality will require reweighting trade-offs significantly in favour of formality through either stricter enforcement or tax reduction. Existing research has highlighted the importance of enforcement in curbing informality but cautions against a potential negative impact on aggregate production (de Andrade et al. 2016, Ulyssea 2018). Tax reductions can also be daunting because of fear of revenue loss.

Interestingly, none of these perceived costs are supported in my research. In the scenario of perfect enforcement, aggregate production does not decrease while government tax revenue increases, as it does in the scenario of tax reduction. Nevertheless, it is important to acknowledge that enforcement against informality can face social acceptability challenges and may be less politically attractive as a result. Therefore, a gradual and persistent mix of productivity-enhancing efforts and enforcement may be an effective and more balanced option.

Author's note: The views expressed here are those of the author and do not necessarily represent the views of the IMF, its Executive Board, or IMF management.

References

Adom, I M (2026), “A structural analysis of firms’ transition from informality to formality in Nigeria,” Journal of Development Economics, 179: 103684.

de Andrade, G H, M Bruhn, and D McKenzie (2016), “A helping hand or the long arm of the law? Experimental evidence on what governments can do to formalize firms,” World Bank Economic Review, 30(1): 24–54.

Farrell, D (2004), “The hidden dangers of the informal economy,” McKinsey Quarterly, (3).

La Porta, R, and A Shleifer (2008), “The unofficial economy and economic development,” Brookings Papers on Economic Activity, 2008: 275–352.

La Porta, R, and A Shleifer (2014), “Informality and development,” Journal of Economic Perspectives, 28(3): 109–126.

Levy, S (2008), “Investment and growth under informality,” in Good intentions, bad outcomes, Brookings Institution Press.

Maloney, W F (2004), “Informality revisited,” World Development, 32(7): 1159–1178.

Ulyssea, G (2018), “Firms, informality, and development: Theory and evidence from Brazil,” American Economic Review, 108(8): 2015–2047.

Ulyssea, G, M Bobba, L Gadenne, and M Harari (2025), “Informality,” VoxDevLit, 6(2).