Discrimination in consumer lending seems to come largely from biased male officers; combatting it may require cultural changes at the institutional level

Are women discriminated against in consumer lending? Answering this question involves normative considerations that transcend social science. In economics, understanding the degree of gender discrimination and its mechanisms is critical for conducting an accurate welfare analysis of the consumer credit market. For instance, statistical discrimination has been argued to be an optimal (efficient) response to an asymmetric information problem between loan officers and applicants (Phelps 1972, Arrow 1973), whereas discrimination stemming from taste-based gender preferences held by loan officers leads to welfare losses (Becker 1957).

Clearly identifying gender discrimination is difficult since the data requirements to make ceteris paribus comparisons across male and female borrowers are extensive. A natural solution is an audit/correspondence study, which has become the gold standard strategy to identify discrimination in labor markets (Neumark 1996, Bertrand and Mullainathan 2004, Oreopoulos 2011), housing markets (Yinger 1986, Christensen and Timmins 2018), in the marketplace (List 2004), or in online platforms (Pope and Sydnor 2011). This approach requires sending gender-randomised loan applications to loan officers and testing whether the resulting approval rates differ by gender. However, this is usually unfeasible in practice since the lending process typically starts by checking the applicant's identity through credit reporting bureaus such as Experian, TransUnion, or Equifax, which allows loan officers to easily identify false loan requests.

The study

In a recent paper (Montoya et al. 2020), we overcome this limitation through the implementation of a correspondence study with more than 400 Chilean loan applicants where instead of manipulating applicant gender, we randomly assign loan requests to a gender-balanced pool of prospective borrowers, who then submitted the assigned requests to randomly assigned loan officers drawn from a representative sample of loan officers working in Chilean banks. The loan requests created for the study randomly varied by amount (ranging between US$1,500 and $13,500) and term (12 to 60 months). We thus ensure by design that loan request, applicant, and loan officer characteristics are all statistically identical across applicant gender.

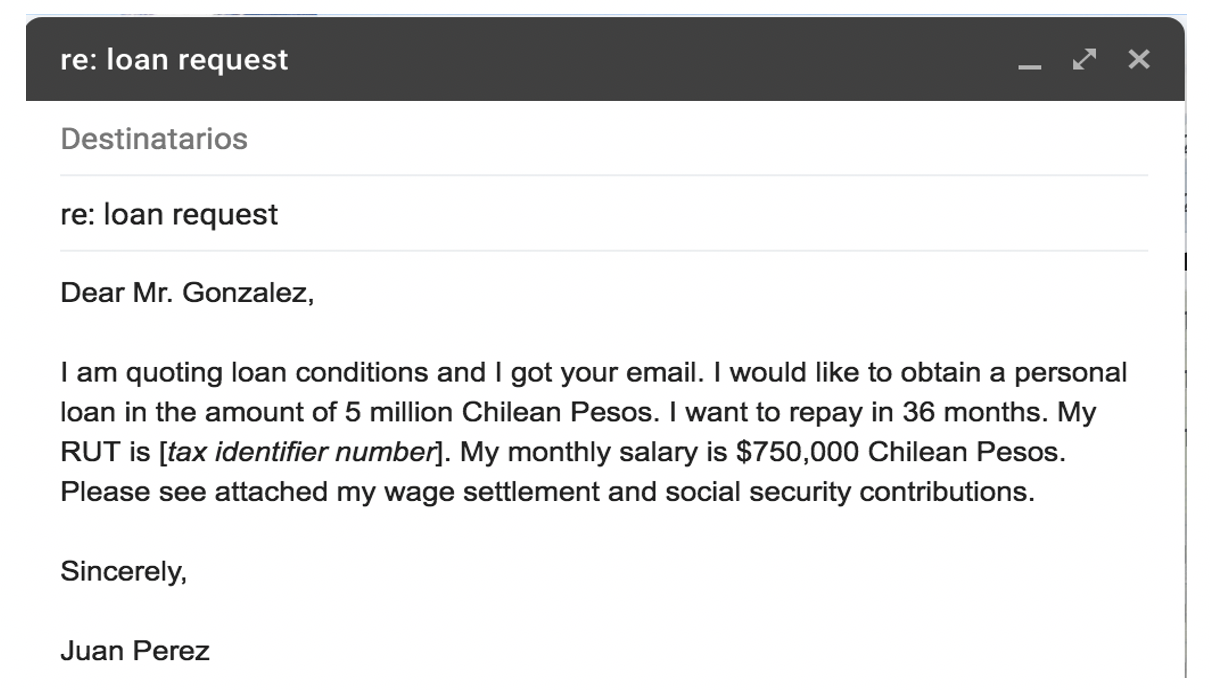

Each applicant was mandated to quote four loan requests from four different loan officers, for a total sample of 1,616 loan requests. A standard way to apply for a consumer loan in Chile is by sending an email directly to a loan officer. In our experiment, applicants had to copy and paste a standardised text containing their assigned loan request, and use their personal email account to send it to the assigned loan officer’s email account. A sample application is shown below.

In addition to a novel design where borrowers and officers interact in a real-world setting to obtain market-level causal estimates of gender discrimination, our study combines the elicitation of loan officers’ gender preferences with an informational experiment to test whether gender differences are grounded on taste-based or statistical sources of discrimination (or a combination of both).

Main findings

Our experiment yields four main results:

- First, we find that the approval rate of loan requests submitted by female borrowers is 18% lower than the approval rate (35%) of otherwise identical loan requests submitted by men. The effect is sizable: it is equivalent to the difference in approval rates between borrowers whose incomes are in the 4th and 7th deciles of the income distribution. This gender discrimination results in median forgone profits of $1,785 per loan, almost one-quarter of the median loan size. Since female borrowers account for one-third of the Chile’s $159 billion consumer loan market, simple extrapolation suggests that gender discrimination is barring Chilean women from $12 billion in credit.

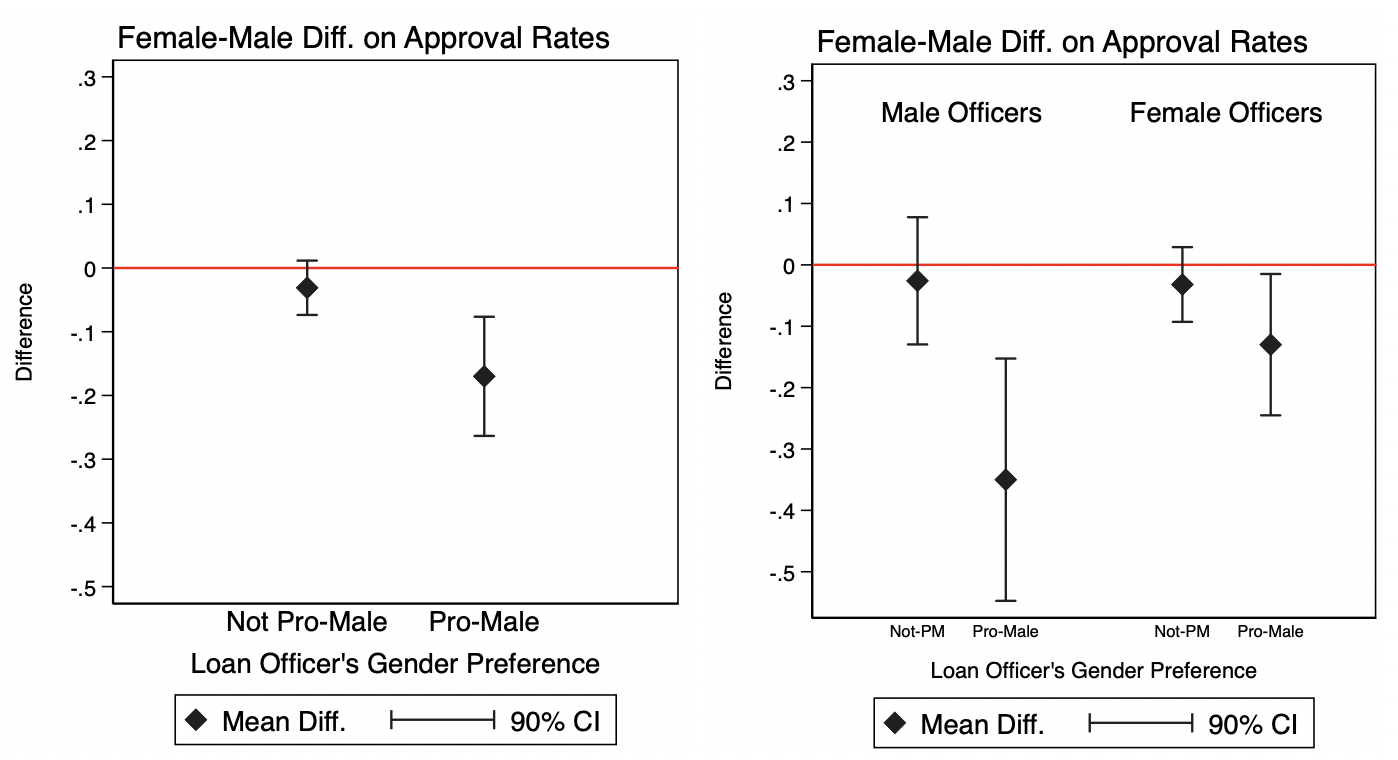

- Second, loan officers were surveyed at baseline through a collaborative agreement with the National Authority of Banking Regulation. The survey includes a battery of subjective measures and experimental tests aimed at eliciting officers’ gender preferences, which allows us to examine the role of taste in gender discrimination. We show that officers whose preferences are not biased against women (i.e. gender-neutral or pro-female) do not discriminate either for or against female borrowers. In contrast, among pro-male officers, approval rates for women are 54% lower relative to approval rates for men, suggesting that gender discrimination against female borrowers is due to taste-based sources. Moreover, the bulk of the effect comes from male loan officers who are pro-male (see Figure 1).

Figure 1 Gender discrimination and loan officer’s gender preferences

- Third, we find bias against women despite official statistics showing that women have higher repayment rates than men, suggesting that (inaccurate) statistical discrimination might also be at work. We test for this by implementing an informational experiment designed to “correct” potentially biased beliefs held by loan officers regarding the repayment performance of male and female borrowers. Half of our sample of loan officers was randomly assigned a message informing them that female borrowers perform better than men in terms of repayment rates. Relative to the control group, we find no reduction in gender discrimination. Further, among pro-male officers, those who received the treatment rejected more female applicants compared to their control counterparts, a result that again suggests discriminatory preferences.

- Finally, we find that female-male differences in approval rates tend to be larger in municipalities with higher levels of market concentration, but this is only the case for loan requests submitted to pro-male loan officers. This result is consistent with Arrow (1973)’s theory of discrimination in that anti-women attitudes become less and less profitable with increasing competition, so taste-based discriminators are eventually competed out of the market.

Policy implications

At least for the case of the Chilean consumer credit market, our evidence suggests that gender discrimination against female applicants does exist and is significant, with most of it coming from gender-biased officers, particularly male officers. This is bad business for both banks and clients. Banks could benefit from implementing better screening processes when hiring loan officers. Since information campaigns aiming to reduce discrimination seem to be ineffective, cultural changes at an institutional scale may be required. On the regulation side, increasing market competition may be a promising way to tackle gender discrimination and should not be overlooked.

References

Arrow, K (1973), “The Theory of Discrimination”, Discrimination in Labor Markets 9: 3–33.

Bertrand, M and S Mullainathan (2004), “Are Emily and Greg more Employable than Lakisha and Jamal?: A Field Experiment on Labor Market Discrimination”, American Economic Review 94: 991–1013.

Becker, G (1957), The Economics of Discrimination, University of Chicago Press.

Christensen, P and C Timmins (2018), “Sorting or Steering: Experimental Evidence on the Economic Effects of Housing Discrimination”, NBER Working Paper No. 24826

List, J A (2004), “The Nature and Extent of Discrimination in the Marketplace: Evidence from the Field”, The Quarterly Journal of Economics 119(1): 49–89

Montoya, A, E Parrado, A Soli and R Undurraga (2020), “Bad Taste: Gender Discrimination in Consumer Credit Markets”, IDB Working Paper Series No. 1053

Neumark, D, R Bank, and K Van Nort (1996), “Sex Discrimination in Restaurant Hiring: An Audit Study”, Quarterly Journal of Economics 111: 915–941.

Oreopoulos, P (2011), “Why Do Skilled Immigrants Struggle in the Labor Market?: A Field Experiment with Thirteen Thousand Resumes”, American Economic Journal: Economic Policy 3: 148–171.

Phelps, E (1972), “The Statistical Theory of Racism and Sexism”, American Economic Review 62: 659–661.

Pope, D and J Sydnor (2011), “What’s in a Picture? Evidence of Discrimination from Prosper.com", Journal of Human Resources 46: 53–92.

Yinger, J (1986), “Measuring Racial Discrimination with Fair Housing Audits: Caught in the Act”, American Economic Review 76(5): 881-93