Evidence from Mexico shows that job loss and employment instability – rather than high interest rates or minimum payment rules – are more important drivers of credit card default among new borrowers, suggesting that social protection may be more effective than contract regulation in promoting financial stability.

Financial inclusion through credit cards

In many developing countries, debt on a credit card is the first formal loan a person receives. In Mexico, credit cards are the first loan type for 74% of all formal sector borrowers; in Peru this figure is 83% and in Colombia it is 51%.[1] There has been a rapid expansion of credit to previously underserved populations, and while it may carry many benefits, it has also raised widespread concern about default among inexperienced borrowers.

A common policy response to this problem has been to regulate contract terms. Numerous countries – including Mexico, Taiwan, Canada, Chile, and Turkey – have imposed or proposed restrictions on interest rates or minimum payment requirements, hoping to shield new borrowers from over-indebtedness. Even in the US, such measures have been discussed as tools for alleviating consumer debt burdens. These policies rest on a seemingly reasonable premise: that high interest rates and lenient repayment terms are the primary drivers of default.

A growing body of research has examined the role of contract terms in loan default in various settings (Karlan and Zinman 2009, De Fusco et al. 2021, Indarte 2021), while other work on Mexico shows that loan design features such as disbursement speed (Burlando et al. 2025) and repayment frequency (DiTraglia et al. 2025) also matter. Our research asks a related but more pointed question: relative to the economic shocks borrowers face, how much can contract terms actually do?

A large-scale experiment with credit card borrowers in Mexico

To answer this question, we worked with one of Mexico’s largest banks to analyse a nationwide randomised experiment, conducted between 2007 and 2009 (Castellanos, Jiménez-Hernández, Mahajan, Prous, and Seira 2025). The experiment covered 144,000 existing credit card borrowers on a product that accounted for roughly 15% of all first-time formal sector loans in the country. About half of these borrowers were relatively new to formal credit.

The experiment randomly assigned borrowers to different contract terms. Annual interest rates ranged from 15% to 45% – a factor-of-three difference. Monthly minimum payments were set at either 5% or 10% of the outstanding balance. These variations far exceed any plausible policy change, providing an unusually clear test of how much contract terms matter.

Default was common. Among the newest borrowers – those with the bank for six to eleven months – 36% defaulted within two years, roughly twice the rate of those with longer banking relationships. It is precisely this pattern that motivates regulators to act.

Contract terms have surprisingly small effects

Our first finding was that reducing the annual interest rate by 30 percentage points – from 45% to 15% – decreased default by only 2.6 percentage points over 26 months, relative to a baseline default rate of 19%. Before we revealed our results, regulators at Mexico’s central bank predicted the effect would be 8.6 percentage points, while experts on the Social Science Prediction Platform guessed 5 percentage points. Both substantially overstated the actual impact.

More troubling, for the newest borrowers – those most at risk and most in need of protection – lowering interest rates had essentially no effect on default.[2]

The effects of raising minimum payments were similarly modest, with an important twist. Doubling minimum payments from 5% to 10% slightly increased default during the experiment, by 0.8 percentage points. The higher required payments strained borrowers’ budgets in the short run, pushing some over the edge. After the experiment ended and payments returned to normal levels, however, those who had faced higher minimums had lower default rates – the forced debt reduction had helped in the longer run (for those who did not default earlier). This double-edged quality of minimum payment requirements is exactly what simple economic reasoning would predict but had not been documented experimentally before.

Job loss as a driver of default

If contract terms explain little, what does drive default? By matching our experimental sample to Mexico’s social security records (IMSS), we could track each borrower’s formal employment history. Two facts stand out:

- Job loss is remarkably common: 42% of borrowers who had held formal employment experienced at least one spell without formal work during our study period.

- Newer borrowers face greater employment instability – those with less than a year of banking history were 1.34 times more likely to experience unemployment than borrowers with longer tenure.

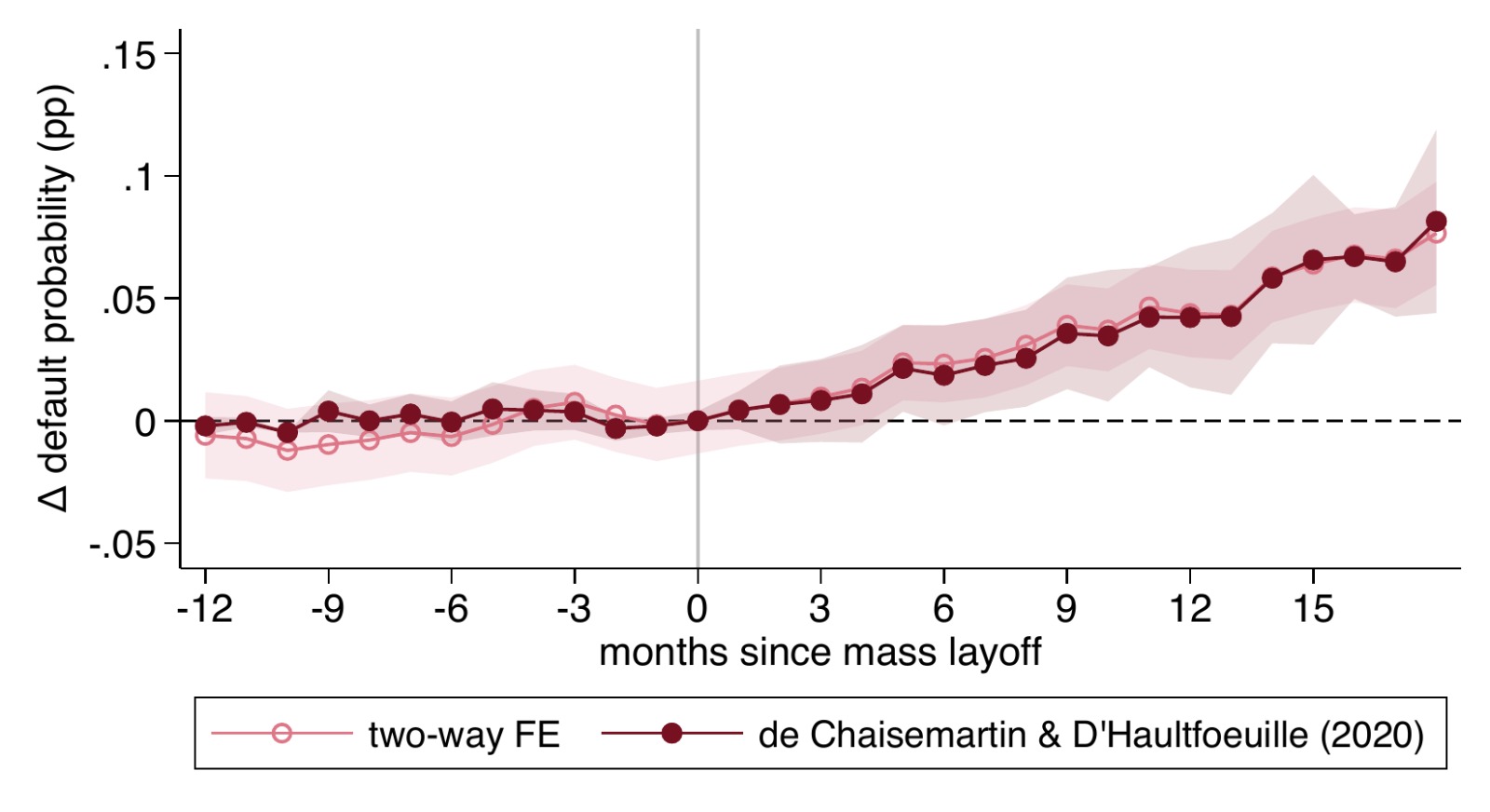

Using mass layoffs as a source of plausibly exogenous job loss, we estimate that displacement increases the probability of default by 6.1 percentage points within 18 months. Figure 1 shows the event-study estimates: default is flat before the mass layoff and then rises sharply. This is 2.4 times larger than the effect of a 30-percentage-point interest rate reduction and 7.6 times the magnitude of the minimum payment changes. In other words, losing a job swamps anything contract terms can do.

Figure 1: Experimental sample and default in experiment card

Why is the difference so large? The answer is straightforward: the cash flow impact of losing a job dwarfs the cash flow impact of any realistic change in contract terms. Borrowers are not insensitive to financial pressure – they simply face income shocks that are substantially larger than what contract term adjustments imply.

Policy implications

These findings have implications for how policymakers think about protecting new borrowers.

- Interest rate caps – among the most popular regulatory tools – do little to reduce default, especially for the most vulnerable borrowers. This is not an argument against financial regulation, but it suggests that the most common form of regulation addresses the wrong problem.

- Social protection mechanisms – unemployment insurance, income stabilisation programmes, or even temporary forbearance for borrowers who lose their jobs – may be more effective at sustaining financial inclusion than contract restrictions. For instance, Hsu et al. (2018) document that unemployment insurance expansions in the US reduced mortgage default precisely by maintaining loan affordability during income disruptions.

- Financial inclusion does not happen in a vacuum. Credit access matters, but so does the stability of borrowers’ economic circumstances. Expanding credit without addressing the employment volatility that new borrowers face may expose them to financial stress that no contract term adjustment can remedy. This is consistent with broader evidence that the benefits of financial access depend on complementary economic conditions (Bruhn and Love 2014, Dupas et al. 2018).

The appeal of contract term regulation is understandable – interest rate caps and minimum payment rules are straightforward to implement and intuitively compelling. But our evidence suggests that if policymakers want to help new borrowers succeed in formal credit markets, they should focus less on the price of credit and more on the economic stability in the lives of the people using it.

Authors' note: The views expressed herein are those of the authors and do not necessarily reflect the views of Banco de México, the Federal Reserve Bank of Chicago or the Federal Reserve System.

References

Banca de las Oportunidades (2016), "Financial inclusion report 2016."

Bruhn, M, and I Love (2014), “The real impact of improved access to finance: Evidence from Mexico,” Journal of Finance, 69(3): 1347–1376.

Burlando, A, M A Kuhn, and S Prina (2025), “Too fast, too furious? Digital credit delivery speed and repayment rates,” Journal of Development Economics, 174: 103427.

Castellanos, S G, D Jimenez-Hernandez, A Mahajan, E Alcaraz Prous, and E Seira (2025), “Contract terms, employment shocks, and default in credit cards,” Review of Economic Studies, rdaf079.

De Fusco, A, H Tang, and C Yannelis (2021), “Measuring the welfare cost of asymmetric information in consumer credit markets,” Journal of Financial Economics, 146(3): 821–840.

DiTraglia, F J, C McIntosh, I Meza, J Sadka, and E Seira (2025), “Structured payment in pawnshop borrowing: Mandates vs. choice,” Unpublished manuscript.

Dupas, P, D Karlan, J Robinson, and D Ubfal (2018), “Banking the unbanked? Evidence from three countries,” American Economic Journal: Applied Economics, 10(2): 257–297.

Hsu, J, D Matsa, and B Melzer (2018), “Unemployment insurance as a housing market stabilizer,” American Economic Review, 108(1): 49–81.

Indarte, S (2021), “Moral hazard versus liquidity in household bankruptcy,” Journal of Finance, 78(5): 2421–2464.

Karlan, D, and J Zinman (2009), “Observing unobservables: Identifying information asymmetries with a consumer credit field experiment,” Econometrica, 77(6): 1993–2008.