Implementation of the Extractive Industries Transparency Initiative (EITI) led to sustained improvements in tax revenue in resource-rich developing countries, particularly as countries progressed from commitment to full EITI compliance.

Editor’s note: For a broader synthesis of themes covered in this article, check out our VoxDevLit on Taxation.

Mobilising tax revenues to finance development priorities remains a persistent challenge in many low-income countries (Besley and Persson 2011, Bachas et al. 2022, Jensen et al. 2024). In resource-rich contexts, this challenge is exacerbated by the so-called ‘resource curse’ (Sachs and Warner 2001), often rooted in opaque governance and weak institutions.

Moreover, windfall revenues from natural resources can reduce the incentive for governments to strengthen domestic tax systems and uphold fiscal discipline. When public budgets are largely financed through resource rents rather than broad-based taxation, citizens—relieved of direct tax burdens—may become less vigilant when it comes to demanding democratic accountability (McGuirk 2013, Ross 2012, Bates and Lien 1985).

As this dynamic undermines the fiscal contract between the state and its citizens, it weakens the motivation for civic engagement and oversight in public finance, further entrenching the opacity of fiscal governance (Ross 2001 2004, Timmons 2005).

To break this vicious cycle, over 50 countries have embraced the Extractive Industries Transparency Initiative (EITI), founded in 2003. This global standard fosters collaboration between governments, extractive companies, and civil society to enhance transparency and accountability. EITI requires the disclosure of key information—including licenses, production volumes, tax payments, and revenue allocations—related to the extraction of oil, gas, and mineral resources.

From transparency to tax gains: Why does the EITI work?

My research (Kinda 2024) examines whether implementing the Extractive Industries Transparency Initiative (EITI) enhances the ability of resource-rich developing countries to increase their domestic tax revenues. By requiring transparency, the EITI helps strengthen public revenue management, build investor confidence, improve access to concessional loans, reduce corruption, and enable citizens to hold governments accountable (EITI 2021, Villar 2022, Corrigan 2014, Le Billon et al. 2011). Together, these effects reinforce the fiscal contract between citizens and the state, supporting more effective and sustainable tax collection.

My analysis draws on data from 83 countries over the period 1995–2017. I mainly employ two empirical approaches: propensity score matching (PSM) and difference-in-difference (DID) estimation in designs with multiple groups and periods. These approaches ensure that the comparison is made between countries (EITI and control group) with similar observable characteristics, isolating the causal impact of EITI membership on domestic revenue mobilisation. EITI's staged approach—moving from commitment to candidacy to full compliance—offers a unique natural experiment to measure its fiscal effects over time.

Does transparency lead to improved fiscal performance in resource-rich governments?

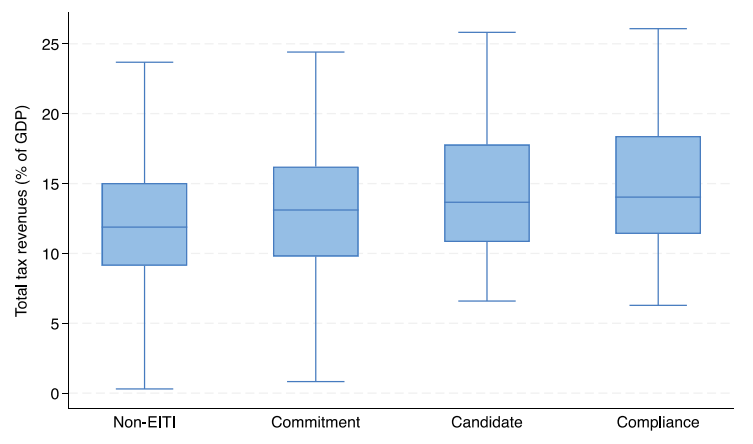

Descriptive statistics (Figure 1) reveal a clear pattern: tax-to-GDP ratios improve steadily as countries progress through the stages of EITI implementation, from commitment to candidacy and then full compliance.

Figure 1: Distribution of total tax revenues according to EITI implementing stages

The empirical results demonstrate a clear and consistent pattern: EITI implementation is associated with significant increases in total and sector-specific tax revenues, particularly when countries reach full compliance. These gains, ranging from 0.06 to over 1 percentage point of GDP, reflect improved enforcement, reduced leakages, and greater fiscal legitimacy. These effects are not only statistically significant but also economically meaningful in settings where domestic fiscal space is limited and revenue volatility is high. These patterns highlight that genuine institutionalisation of transparency—not just symbolic adoption—is what delivers lasting fiscal benefits.

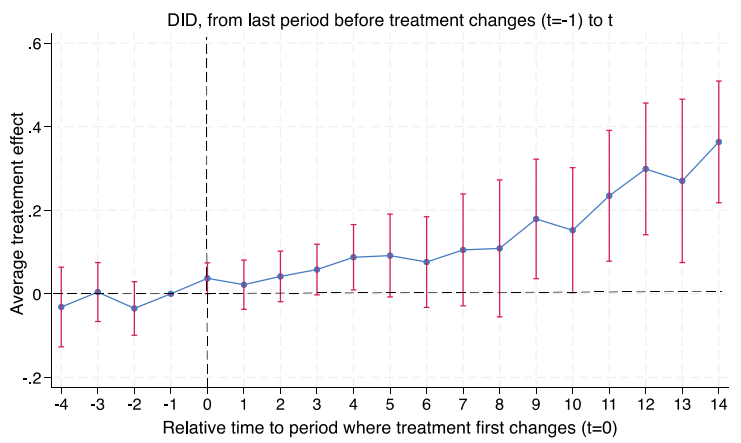

The good news? The dynamic effects of EITI implementation suggest that the benefits of transparency accumulate over time. As shown in Figure 2, countries that sustain their commitment to the initiative witness increasing treatment effects on total tax revenue. Starting from the period immediately following adoption (t=0), the average treatment effect becomes progressively larger and more statistically significant over the subsequent years. This trajectory suggests that EITI reform is not a one-off intervention but rather a catalyst for long-term institutional change.

Figure 2: The dynamic treatment effect of EITI implementation on total tax revenues

The upward trend in the estimated effects implies that transparency reforms can have self-reinforcing impacts—through improved revenue forecasting, more effective auditing of extractive revenues, better public spending scrutiny, and increased public trust. For countries that ‘stay the course’, the dividends include higher and more stable revenue streams, reduced reliance on volatile natural resource rents, and a stronger fiscal foundation for inclusive development.

The disaggregated analysis adds depth to these findings. Increases in non-resource tax revenues, such as value-added and income taxes, reach up to 0.22 percentage points, indicating that EITI may improve general fiscal capacity, not just resource-related revenues. These findings align with recent evidence which suggests that revenue-sharing from natural resources leads to better education and labour outcomes in non-extractive regions (Bancalari and Rud 2025). Thus, with the EITI, governments, under strengthened public control, are encouraged to mobilise and spend revenues responsibly, leading to positive spillover effects on the non-resource tax base.

The most substantial improvements are observed in resource-specific tax revenues, which rise by more than 1 percentage point of GDP on average, highlighting EITI's role in reducing opacity and underreporting. Direct taxes—including income, profit, and capital gains taxes—improve by up to 0.44 percentage points, likely reflecting enhanced enforcement mechanisms and increased taxpayer confidence in public institutions resulting from improved fiscal governance and transparency.

These gains are consistently amplified in countries with higher institutional quality, particularly where control of corruption, government effectiveness, and rule of law are stronger. This suggests an important interaction effect: EITI can serve as a catalyst but its impact is conditional on the broader governance ecosystem.

Policy implications: EITI

My findings confirm that transparency, when institutionalised, enhances domestic revenue mobilisation in resource-rich countries. Yet, symbolic membership is insufficient—substantial gains arise from full compliance, public reporting, and integration into budget systems. Policymakers should leverage the EITI as a launchpad for broader reforms, including modernising tax administrations, linking disclosures to public finance management, and enhancing civil society oversight. Countries that stay the course benefit from higher, more predictable revenues and stronger governance foundations.

References

Bachas, P, M Fisher-Post, A Jensen, and G Zucman (2022), “Capital taxation, development, and globalization,” NBER Working Paper.

Bancalari, A, and JP Rud (2025), “How Peru transformed natural resource wealth into local development,” VoxDev.

Bates, RH, and DHD Lien (1985), “A note on taxation, development, and representative government,” Politics & Society 14(1): 53–70.

Besley, T, and T Persson (2011), “Pillars of prosperity: The political economics of development clusters,” Princeton University Press.

Corrigan, CC (2014), “Breaking the resource curse: Transparency in the natural resource sector and the extractive industries transparency initiative,” Resources Policy 40: 17–30.

EITI (2021), “EITI standard 2019: The global standard for the good governance of oil, gas and mineral resources.”

Jensen, A, A Brockmeyer, and L Gadenne (2024), “Taxation and development,” VoxDevLit 12(1).

Kinda, H (2024), “Driving fiscal growth: The impact of EITI membership on tax revenue mobilization in resource-rich developing countries,” Oxford Development Studies 53(1): 66–85.

Le Billon, P, P Lujala, and SA Rustad (2021), “Transparency in environmental and resource governance: Theories of change for the EITI,” Global Environmental Politics 21(3): 124–146.

McGuirk, E (2013), “The illusory leader: Natural resources, taxation and accountability,” Public Choice 154: 285–313.

Villar, PF (2022), “An assessment of the Extractive Industries Transparency Initiative (EITI) using the Bayesian corruption indicator,” Environment and Development Economics 27(5): 414–435.

Ross, ML (2001), “Does oil hinder democracy?” World Politics 53(3): 325–361.

Ross, ML (2004), “What do we know about natural resources and civil war?” Journal of Peace Research 41(3): 337–356.

Ross, ML (2012), “The oil curse: How petroleum wealth shapes the development of nations,” Princeton University Press.

Sachs, JD, and AM Warner (2001), “The curse of natural resources,” European Economic Review 45(4–6): 827–838.

Timmons, JF (2005), “The fiscal contract: States, taxes, and public services,” World Politics 57(4): 530–567.