In Uganda, digital cash transfers had contrasting effects on women’s empowerment: mobile money boosted women’s personal income and decision-making power, while jointly disclosed cash transfers reduced intimate partner violence by fostering trust and increasing shared earnings – highlighting an important trade-off between individual autonomy and household harmony.

Editor’s note: For a broader synthesis of themes covered in this article, check out Issue 2 of our VoxDevLit on Mobile Money.

Cash transfers are a key component of social safety nets worldwide (Crosta et al. 2025). Beyond reducing poverty, cash transfers are expected to enhance women’s empowerment by giving them greater autonomy and decision-making power. While research generally finds that cash transfers improve women’s decision-making power, their impact on intimate partner violence (IPV) is less conclusive (Hidrobo and Roy 2019, Baranov et al. 2021, Buller et al. 2018).

The rise of mobile money makes cash transfers more attractive by lowering transfer costs, but it also raises new questions: do digital payments enhance women’s financial control (Aker et al. 2016, Riley et al. 2024), or risk undermining trust if men feel excluded (Field et al. 2021)? While privacy of information is often cited as a potential mechanism, based on evidence of its role in decision making, there is little research examining this in the context of cash transfers (Ashraf 2009, Castilla and Walker 2013). To study this, we conducted a field experiment in Uganda assessing how transfer modality (cash versus mobile money), and privacy of information (whether the beneficiary’s spouse was informed) affected women’s empowerment and IPV.

In Uganda, digital financial services such as mobile money are increasingly integrated into aid delivery. Digital transfers promise convenience, security, and autonomy – but they may also reshape household relationships in unexpected ways, especially in patriarchal settings where men traditionally control finances. Evidence from a new randomised controlled trial (Greco, Gulesci, Prabhakar and Sulaiman 2025) sheds light on this by directly comparing the effects of digital versus cash-based transfers on women’s economic empowerment and IPV.

Studying different modes of delivering cash transfers

We partnered with BRAC to deliver one-off unconditional transfers of around US$50 to 1,600 married women across 200 communities in Uganda, using a 2×2 design with community-level randomisation. Transfers varied by:

- Mode of transfer: physical cash versus mobile money.

- Privacy of information: whether the beneficiary’s husbands were informed (‘joint’) or not (‘private’).

These four treatment groups (Figure 1) – joint cash, private cash, joint mobile money, and private mobile money – are compared with a control group of 400 women from 50 communities. In the private arms, women were informed individually without their husbands present; while in the joint arms, women were informed jointly with their husbands about the transfer. In all cases, the transfer was explicitly described as being made to the woman herself. All participants owned a mobile phone and a registered mobile money account. Outcomes were measured 8 to 9 months later, focusing on women’s earnings, decision-making power, marital trust, and experiences of IPV.

Figure 1: Cash versus mobile money transfers

The mode of cash transfer delivery matters for women’s empowerment

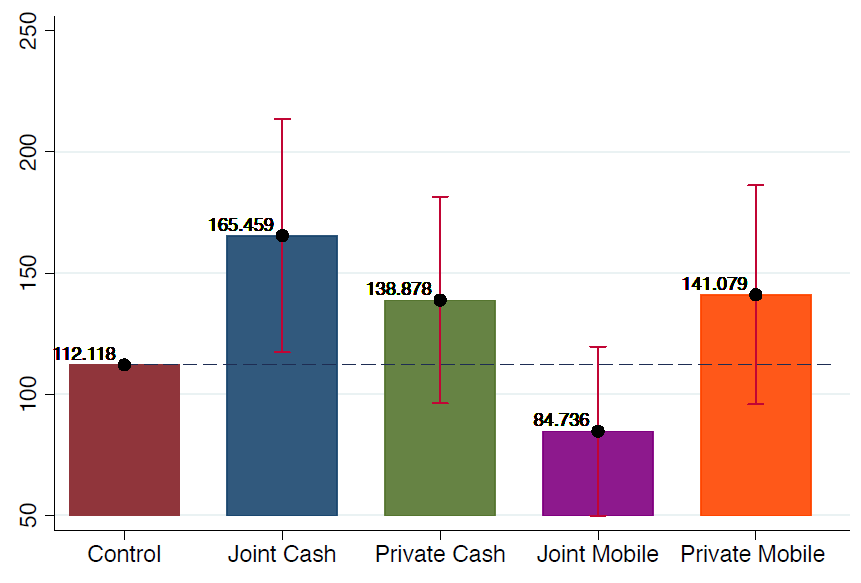

1. Digital transfers boost women’s personal income and autonomy, while cash strengthens joint activities. To assess income impacts, we separated women’s individual earnings from those generated jointly with their husbands. While some activities, such as wage work, are typically individual, farming or livestock rearing may be managed either alone or together. This distinction proved critical: mobile money transfers increased income from women’s personal activities (Figure 2A), while cash transfers raised earnings from joint activities with husbands (2B). Women receiving digital payments also reported greater say in household decisions, especially around children’s education and health, whereas cash transfers boosted shared earnings but did less to strengthen women’s independent control.

Figure 2A: Personal earning from activities done by the women herself

Figure 2B: Earning from activities done by the women jointly with husband

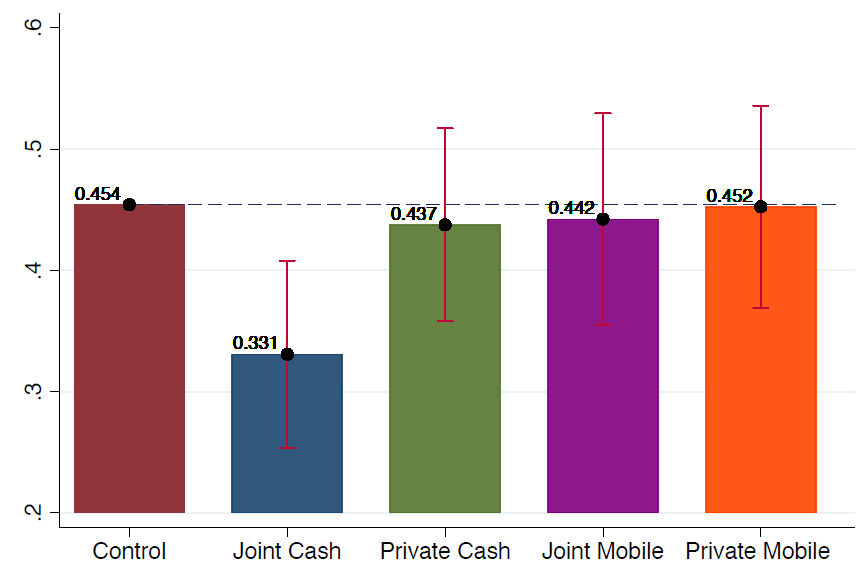

2. Only joint cash transfers reduced IPV. We find that transfers reduced IPV only in the joint cash arm, with no reduction in any of the other treatment groups compared to the control group (Figure 3). While 45% of women in the control women reported experiencing any form of violence in the past 12 months, the rate was substantially lower at 33% for the joint cash group. The rates for the other three treatment groups remained unaffected.

Figure 3: Any type of IPV experienced by the women in the past year

3. Joint cash transfers foster trust by supporting shared earnings, whereas other modalities fail to strengthen marital cooperation. We find marital trust and reductions in husbands’ controlling behaviour as potential mechanisms for the decline in IPV. Cash transfers, particularly when jointly disclosed, fostered greater trust and cooperation, supporting household harmony more effectively than digital payments. By contrast, mobile money shifted financial dynamics within couples, reducing income sharing, not enhancing marital trust, and increasing husbands’ controlling behaviours. In other words, cash promoted cooperation and reduced intra-household conflict in ways that mobile money did not.

Regarding the role of privacy, contrary to expectations, whether husbands were informed or not did not systematically strengthen the outcomes. This suggests that the benefits of mobile money arise less from privacy of information and more from women’s practical ability to control and use funds. For instance, both joint and private mobile money transfers increased women’s earnings from independent activities. At the same time, the protective effect against IPV was concentrated in joint cash transfers, which reduced all forms of violence; however, making the cash transfer private did not lower IPV.

Policy implications: Cash transfers and women’s empowerment

Our findings underscore an important trade-off: digital transfers can empower women by enhancing their autonomy and individual economic activity, while cash transfers – particularly when both spouses are informed – can be more effective in reducing intimate partner violence. For policymakers and NGOs, this means that a shift toward full digitalisation should not occur in isolation but rather accompanied by supportive measures such as couple-based training, community dialogue on gender norms, and IPV prevention services.

Programme design should also reflect context-specific priorities: whether the primary goal is to maximise women’s economic independence or reduce household conflict. Hybrid models that combine digital payments with complementary interventions – or allow flexibility in transfer modality – may offer a practical way to balance these competing objectives.

Cash transfers are more than a financial transaction: they reshape household power and relationships. As governments and aid agencies increasingly adopt digital payments, our research emphasises the need for nuanced design. Delivering funds digitally can empower women economically but may risk triggering backlash at home, while cash-based transfers may promote harmony but less autonomy. The challenge for policymakers is not whether to use cash transfers, but how to deliver them in ways that balance women’s empowerment with their safety.

References

Aker, J C, R Boumnijel, A McClelland, and N Tierney (2016), “Payment mechanisms and antipoverty programs: Evidence from a mobile money cash transfer experiment in Niger,” Economic Development and Cultural Change 65(1): 1–37.

Baranov, V, L Cameron, D C Suarez, and C Thibout (2021), “Theoretical underpinnings and meta-analysis of the effects of cash transfers on intimate partner violence in low- and middle-income countries,” The Journal of Development Studies 57(1): 1–25.

Buller, A M, A Peterman, M Ranganathan, A Bleile, M Hidrobo, and L Heise (2018), “A mixed-method review of cash transfers and intimate partner violence in low- and middle-income countries,” The World Bank Research Observer 33(2): 218–258.

Castilla, C, and T Walker (2013), “Is ignorance bliss? The effect of asymmetric information between spouses on intra-household allocations,” American Economic Review 103(3): 263–268.

Crosta, T, D Karlan, F Ong, J Rüschenpöhler, and C R Udry (2025), “Unconditional cash transfers: A Bayesian meta-analysis of randomized evaluations in low and middle income countries,” NBER Working Paper.

Field, E, R Pande, N Rigol, S Schaner, and C Troyer Moore (2021), “On her own account: How strengthening women’s financial control impacts labor supply and gender norms,” American Economic Review 111(7): 2342–2375.

Greco, G, S Gulesci, P Prabhakar, and M Sulaiman (2025), “Digital cash transfers, privacy and women’s empowerment: Evidence from Uganda,” CEPR Discussion Paper.

Hidrobo, M, and S Roy (2019), “Cash transfers and intimate partner violence,” VoxDev.

Riley, E (2024), “Resisting social pressure in the household using mobile money: Experimental evidence on microenterprise investment in Uganda,” American Economic Review 114(5): 1415–1447.