Index insurance can help smallholder farmers take on more productive risks, but its impacts remain modest, uncertain, and highly context dependent.

Editor's note: The authors have made slides available to accompany this research here.

Farmers worldwide are facing growing weather-related risks, especially in low- and middle-income countries where irrigation remains limited. As extreme weather events intensify, these risks are becoming more frequent and severe, threatening livelihoods and food security. Against this backdrop, index insurance has emerged to help smallholder farmers manage risks and boost their productive investments. According to Carter et al. (2017), it is ‘‘one of the most important current opportunities to designing new institutions that can help developing countries achieve the goal of increased investment in agriculture, accelerated growth, and poverty reduction’’.

Index insurance and its impacts in individual studies

Index insurance differs from traditional insurance, which compensates farmers for their specific losses. It pays out instead when an indicator – such as rainfall levels, average yields in a region, or satellite images of vegetation – shows that conditions have been bad. Because payouts are tied to an external and easily observable indicator that is correlated – but not identical – to individual losses, index insurance avoids many of the problems of traditional insurance, including high costs, moral hazard, and adverse selection. This makes it especially appealing in low- and middle-income countries, where smallholder farmers often cannot afford traditional insurance.

Results from impact evaluations of index insurance are accumulating, but key questions remain about their average effects and how to draw generalisable lessons. In recent work (Castaing and Gazeaud 2025), we take stock of this evidence using a Bayesian meta-analysis, combining micro-data from eight experiments and applying common estimation strategies. These eight experiments examine similar products across diverse settings: Bangladesh (Hill et al. 2019), Burkina Faso (Stoeffler et al. 2022), Ghana (Karlan et al. 2014), Kenya (Bulte et al. 2019), India (Cole et al. 2017), Mali (Elabed and Carter 2014), Mozambique and Tanzania (Boucher et al. 2024). All of which were implemented as randomised controlled trials, offering an ideal opportunity to pool evidence and assess external validity. Although their findings suggest that index insurance helps farmers take on more risk, each study is rooted in a specific context (period, location, population), raising questions about how far the results can be extrapolated.

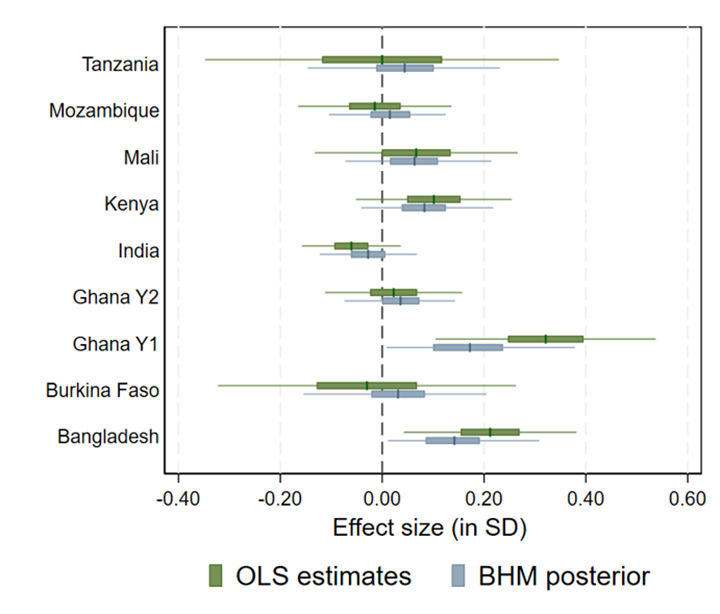

We look at effects on costly inputs that insurance could stimulate if it enables farmers to take on more risk: cultivated area, fertilisers, pesticides, and seeds. Figure 1 shows the effects in each individual study on fertiliser use. While most point estimates are positive, there is considerable variation in effects, ranging from -0.06 standard deviations (SD) in India to +0.32 SD in Ghana. It is not clear, however, how much of this variation reflects true differences in treatment effects versus random variation from different samples. As shown in Figure 1, most 95% confidence intervals overlap, making it difficult to exclude that these studies capture a common effect. To separate true variation in treatment effects from sampling variation, we pool information across settings using a Bayesian meta-analysis (Meager 2019). Interestingly, once information is pooled across studies (blue lines), the estimated effects converge and become more precise – showing smaller variation across settings. Averaged across all outcomes and studies, we find moderate pooling of information, with 61% of the observed variation in treatment effects stemming from sampling variation.

Figure 1: The effects of index insurance on fertiliser use across individual studies

Notes: The figure shows study-specific intent-to-treat (ITT) effects estimated with a Bayesian hierarchical model (BHM), alongside no-pooling OLS estimates for comparison. The Bayesian hierarchical model allows us to separate the genuine variation in treatment effects from the sampling variation. Thin (resp. thick) lines represent the 95% (resp. 50%) confidence/posterior intervals. All outcomes have been standardised using micro-data from the original studies.

Aggregating evidence across studies on index insurance

Our research also asks what the average effect of index insurance is across contexts, and whether the existing evidence can be used to predict its effect in a new country or setting.

Meta-analyses offer a powerful tool for answering these questions. However, meta-analyses have been criticised (e.g. Data Colada 2022) for combining studies that can be too different to be meaningfully averaged, treating studies as equally valid regardless of quality, and being vulnerable to publication bias – which can lead to misleading estimates of effects. To guard against these issues, we only selected studies that used similar insurance products, applied standard estimation strategies, and were implemented as randomised controlled trials. Crucially, we accessed the micro-data from each experiment, allowing us to harmonise outcomes and estimations to aggregate truly comparable effects. We also assessed the extent of publication bias using the AEA registry and find no indication of a sizable bias.

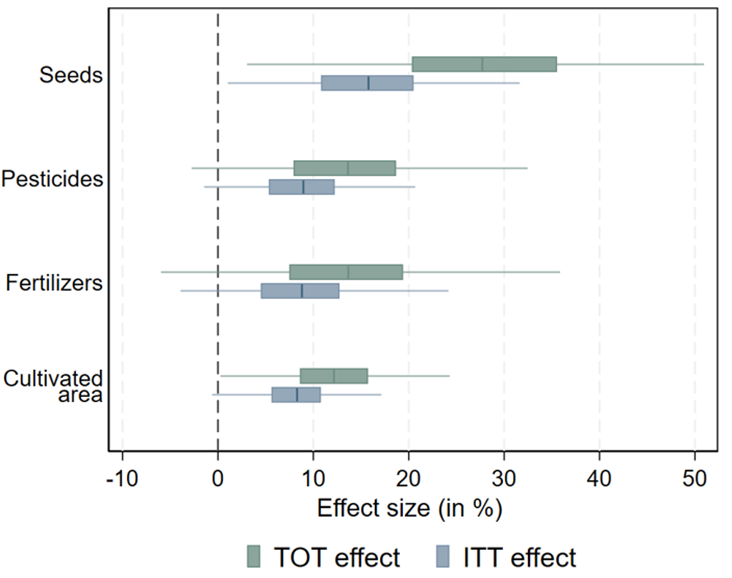

Figure 2: The average effect of index insurance on production decisions across settings

Notes: This figure presents evidence on the average intent-to-treat (ITT) effect of randomly assigned offers to take up index insurance, as well as effects on those who actually take up index insurance (treatment-on-the-treated or TOT effects). Effects are reported as percent changes relative to the control group mean. Study-specific TOT effects are derived using the random assignment to insurance offers as an instrument for actual take-up, and then aggregated using our Bayesian hierarchical model.

In Figure 2, we present average intent-to-treat (ITT) effects – that is, the effects of being offered insurance regardless of whether farmers subscribed. ITT effects are arguably the most relevant parameter for policymakers interested in the economy-wide impacts of index insurance programmes. We estimate sizable but somewhat imprecise effects: farmers offered insurance cultivate 8% more land, use 9% more pesticides, 9% more fertilisers, and 16% more seeds.[1] We also estimate the average impacts on those who actually take up insurance (treatment-on-the-treated or TOT effect), using the random assignment to the insurance offers as an instrument for actual take-up. These effects are larger – between 12% and 28% – but remain imprecise.

We conclude our analysis by using our model to predict the effect of index insurance in a new setting. We find that the posterior intervals of the predicted effects all comfortably include zero, which reflects the large uncertainty arising from variation in treatment effects. For example, we estimate that the treatment effect on fertiliser in a new context has a 50% chance of falling between 0 SD and 0.13 SD, 25% chance of being negative, and 25% chance of being larger than 0.13 SD.[2] None of the household characteristics we tested are associated with larger or more predictable effects. Overall, this suggests that the existing evidence base offers limited insights to predict the effects of index insurance in new settings, and that conducting new studies in such settings remains a worthwhile endeavour. Back-of-the-envelope calculations suggest that an inference about effects in a new setting will have the correct sign about 81% of the time, whereas prediction errors will be above 0.10 SD around 26% of the time and above 0.05 SD around 51% of the time.

The potential of the next generation insurance products

While sobering, our findings should not be taken as a reason to abandon efforts to promote index insurance. Rather, they suggest that index insurance can stimulate smallholders’ productive investments, though impacts are more muted and less certain than earlier studies implied. The substantial uncertainty around positive impacts, and the evidence on the limited uptake of products, calls for caution from governments and development agencies.

Nonetheless, recent innovations in the design and implementation of index-based insurance have raised hopes that newer products may address some of the challenges that limit the effectiveness of the first generation of products. For example, products taking advantage of the latest advances in remote sensing and digital technologies could further reduce transaction costs and basis risk.

More evidence is required before index insurance can be promoted as a cost-effective solution to help smallholder farmers manage risks at scale. At the same time, other tools – such as stress-tolerant crops, improved weather forecasting, and emergency credit lines – hold real promise. Assessing both their cost-effectiveness and complementarity with insurance products is a key direction for future research. In addition, more research is needed to understand the drivers of heterogeneity in effects – and we suspect learning, trust, and insurance quality may be important dimensions to consider.

References

Boucher, S R, M R Carter, J E Flatnes, T J Lybbert, J G Malacarne, P P Mareyna, and L A Paul (2024), “Bundling genetic and financial technologies for more resilient and productive small-scale farmers in Africa,” The Economic Journal: ueae012.

Bulte, E, F Cecchi, R Lensink, A Marr, and M Van Asseldonk (2019), “Do crop insurance certified seed bundles crowd-in investments? Experimental evidence from Kenya,” Journal of Economic Behavior and Organization.

Carter, M, A de Janvry, E Sadoulet, and A Sarris (2017), “Index insurance for developing country agriculture: A reassessment,” Annual Review of Resource Economics 9: 421–438.

Castaing, P, and J Gazeaud (2025), “Do index insurance programs live up to their promises? Aggregating evidence from multiple experiments,” Journal of Development Economics 175: 103501.

Cole, S, X Giné, and J Vickery (2017), “How does risk management influence production decisions? Evidence from a field experiment,” The Review of Financial Studies 30(6): 1935–1970.

Data Colada (2022), “Meaningless means: Some fundamental problems with meta-analytic averages.”

Elabed, G, and M Carter (2014), “Ex-ante impacts of agricultural insurance: Evidence from a field experiment in Mali.”

Hill, R V, N Kumar, N Magnan, S Makhija, F de Nicola, D J Spielman, and P S Ward (2019), “Ex ante and ex post effects of hybrid index insurance in Bangladesh,” Journal of Development Economics 136: 1–17.

Karlan, D, R Osei, I Osei-Akoto, and C Udry (2014), “Agricultural decisions after relaxing credit and risk constraints,” The Quarterly Journal of Economics 129(2): 597–652.

Meager, R (2019), “Understanding the average impact of microcredit expansions: A Bayesian hierarchical analysis of seven randomized experiments,” American Economic Journal: Applied Economics 11(1): 57–91.

Stoeffler, Q, M Carter, C Guirkinger, and W Gelade (2022), “The spillover impact of index insurance on agricultural investment by cotton farmers in Burkina Faso,” The World Bank Economic Review 36(1): 114–140.