A long-run study tracking students nine years after a school financial education programme finds lasting reductions in expensive credit use, improved loan repayment, and a shift towards entrepreneurship. This suggests that well-designed curricula can reshape both financial and occupational decisions.

As access to credit expands in many countries, policymakers face a growing concern: are individuals equipped to use financial products wisely? Governments have responded by introducing financial education into school curricula, yet it remains unclear whether these programmes change behaviour over time.

A recent meta-analysis concludes that school financial education programmes have strong effects on financial knowledge and weaker effects on behaviour (Kaiser and Menkhoff 2020). However, most studies measure outcomes shortly after the intervention, often within a year, but the consequences of financial literacy (or lack thereof) often unfold much later, when individuals begin working and running businesses (Entorf and Hou 2018).

Three studies look at longer-run effects of financial education for students. First, Frisancho (2023) tracks the effects of a 2016 programme in Peruvian high schools up to three years later using credit bureau data. She finds no overall effect on credit use, though borrowers in arrears saw a 20% reduction. Second, in ongoing work, Frisancho et al. (2025) use administrative data to measure the effects of the Peruvian programme for up to seven years, focusing on credit behaviour during the COVID-19 pandemic. Third, Horn et al. (2023) examine financial education in Ugandan youth clubs. Using self-reported data from a five-year follow-up, the authors find that the programme increased savings and income, mainly from informal sources, with no effect on borrowing.

Studying students’ financial behaviour in the real world

We contribute to the evidence base on the long-run impacts of financial education, by revisiting a large randomised controlled trial conducted with approximately 25,000 students in 892 public high schools in Brazil. The intervention ran from 2010 to 2011, during the last two years of high school. It integrated financial education into existing classroom curricula such as mathematics and science.

Bruhn et al. (2016) used surveys, conducted right after the programme ended, to measure its short-run effects, showing improved financial knowledge, as well as better savings and budgeting behaviour, but also an increase in credit use.

We now draw on administrative data housed at the Central Bank of Brazil to track outcomes for up to nine years after the programme ended and students graduated high school (Bruhn, Garber, Koyama, and Zia 2025). This facilitates tracking students over time at a relatively low cost and allows us to observe real behaviour rather than relying on self-reported outcomes.

We link students from the original intervention to administrative records using taxpayer IDs (CPFs). Because CPFs were missing for most students, we reconstructed them via a name-based matching algorithm applied to the Federal Government Revenue Service registry, using additional information on age to improve accuracy. After removing ambiguous matches, we obtain a preferred sample of approximately 16,000 students with reliably identified CPFs, with robustness checks using a broader matching approach yielding similar results.

Financial education reduces reliance on expensive credit and improves repayment

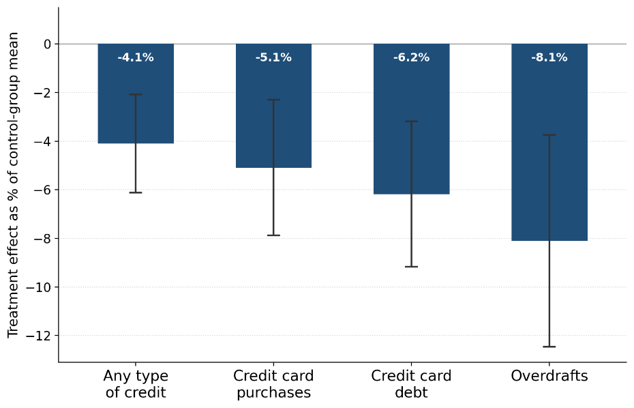

The most striking finding is that financial education leads to more prudent borrowing decisions in the long run. Students exposed to the programme were less likely to use credit overall, and especially less likely to rely on the most expensive forms, such as credit card debt and overdrafts, which carry very high interest rates in Brazil (Figure 1). The percentage of students with credit card debt decreased by 6.2%, going from 23% to 21.5%, while the percentage of students with overdrafts declined by 8.1%, from 11.1% to 10.2%. The programme also improved repayment outcomes. In the long run, participants are less likely to have loans with delayed repayments compared to those in the control group.

Figure 1: Long-term effects of school financial education on credit usage

Notes: This figure shows effects of the programme on the probability that students have credit in the four categories shown on the x-axis, up to nine years after they left high school. Bars show the treatment effect divided by the control-group mean. Whiskers are 95% confidence intervals scaled by the same means. All effects are significant at p<0.01.

Interestingly, the long-term results contrast with the short-term findings that students were more likely to use credit, possibly reflecting experimentation with newly learned financial tools. A plausible mechanism is experiential learning: students test financial products early on, learn from mistakes, and adjust their behaviour accordingly.

Effects extend beyond finance: More formal entrepreneurship

Perhaps the most surprising result is that the programme affects occupational choices. Eight to nine years after graduation, participants are 10.2% more likely to own a microenterprise and 4.8% less likely to hold a formal salaried job. This shift likely reflects the programme’s broader curriculum which included modules on work and entrepreneurship.

There is also some evidence that financial education increases participation in informal economic activity. This may reflect individuals starting small, unregistered businesses that are common in many developing economies. While informality can be associated with lower income and benefits, entrepreneurship can also offer flexibility and autonomy. The net welfare implications are therefore ambiguous.

Encouragingly, we find no evidence that the programme reduces income overall, suggesting that these occupational shifts do not come at a clear economic cost.

Is financial education cost-effective?

A simple cost-benefit calculation suggests the programme is economically viable. By reducing reliance on high-interest credit, participants save about BRL 46 on interest payments per year on average. These savings accumulate to offset the cost of the programme (BRL 206 per student) after approximately five years.

Policy implications for financial education

What do these results imply for policymakers?

- School financial education has lasting effects. Contrary to common scepticism, school-based financial education can influence real financial behaviour years later, especially when delivered at scale and integrated into curricula.

- Financial education can strengthen consumer protection. Reducing the use of expensive sources of credit is desirable from a financial consumer protection perspective due to the high interest rates in Brazil. While this goal may be achieved via interest rates caps, these can distort lenders’ credit decisions. By reducing long-run reliance on expensive credit, financial education can help protect consumers from costly debt in a market-friendly and cost-effective way.

- Comprehensive curricula matter. The shift towards entrepreneurship highlights that financial education can shape labour market decisions, not just financial choices. And that including entrepreneurship alongside financial literacy may amplify broader economic effects.

- Short-term evaluations may underrate impact. Programmes that appear ineffective in the short run may yield substantial benefits over time. Evaluations should, wherever possible, track longer-term outcomes.

- Administrative data facilitates long-run evaluation. Administrative data allows researchers and policymakers to track outcomes over time and assess long-term impacts at relatively low cost compared to surveys. Strong record-keeping, reliable identification systems, and collaboration across stakeholders are key for linking data across sources and enabling such analysis.

References

Bruhn, M, L de Souza Leão, A Legovini, R Marchetti, and B Zia (2016), "The impact of high school financial education: Evidence from a large-scale evaluation in Brazil," American Economic Journal: Applied Economics, 8(4): 256–295.

Bruhn, M, G Garber, S Koyama, and B Zia (2025), "The long-term impact of high school financial education: Evidence from Brazil," Review of Economics and Statistics.

Entorf, H, and J Hou (2018), "Financial education for the disadvantaged? A review," SAFE Working Paper No. 205.

Frisancho, V (2023), "Is school-based financial education effective? Immediate and long-lasting impacts on high school students," Economic Journal, 133(651): 1147–1180.

Frisancho, V, A García, E Ventura, and J C Chong (2025), "Lasting lessons: The long-term impacts of school-based financial education," Mimeo.

Horn, S, J C Jamison, D Karlan, and J Zinman (2023), "Five-year impacts of group-based financial education and savings promotion for Ugandan youth," Review of Economics and Statistics, 1–23.

Kaiser, T, and L Menkhoff (2020), "Financial education in schools: A meta-analysis of experimental studies," Economics of Education Review, 78: 101930.