The 1997 Thai financial crisis had far longer lasting consequences for financial access than aggregate measures suggest, driven by bank branch closures that were never reversed even after the broader economy recovered.

Editor’s note: The authors have made slides available here.

Financial crises can create massive liquidity issues and financial losses for banks. This can lead banks to close some of their worst-performing branches, even those that are profitable in the long term. At the same time, physical proximity to bank branches is an important determinant of credit access, particularly in rural areas in developing countries.

The 1997 financial crisis and branch closures in Thailand

In our research, we explore the effect of the 1997 Thai financial crisis on credit access through the branching channel (Rysman, Townsend, and Walsh 2026). From 1985 to 1996, Thailand was one of the fastest-growing economies in the world, with an annual rate of 7.5–9%. But in 1997, it experienced a major financial crisis, plunging the country into a deep recession. Based on macro-aggregate measures, Thailand appears to have recovered within two to three years. Interest rates and the national unemployment rate returned to pre-crisis rates, and GDP growth was at a healthy 4.5–5%

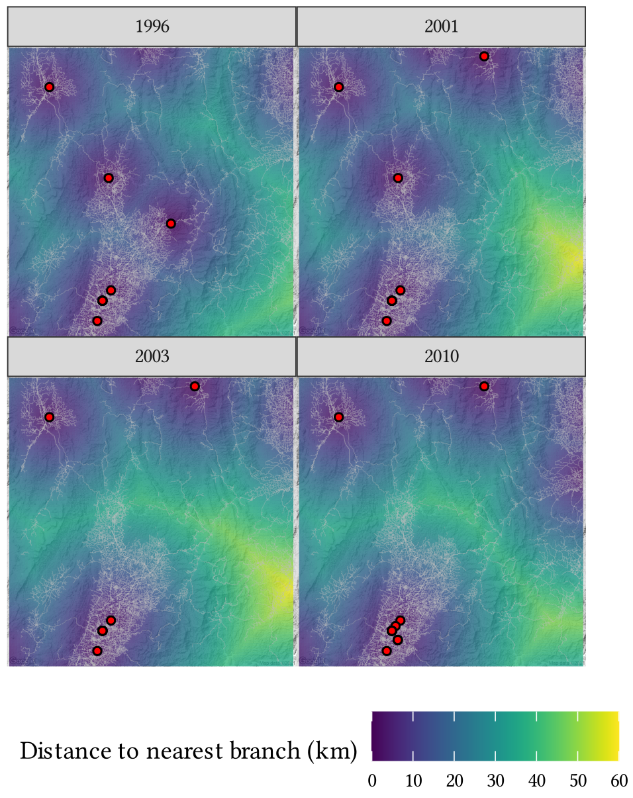

However, when we look at areas with branch closures during the crisis, many did not see their branches replaced when the local economy recovered. In Figure 1, we show an example of such an area in Northern Thailand. The first panel shows the situation before the crisis in 1996. The remaining panels show the same area in the years during and after the crisis. We can see that some branches closed in the centre of the figure, leaving that area very far away from the nearest branch (up to 50km as the crow flies). These branches were not replaced by the end of our sample period in 2010, even though national GDP was higher by that point.

Figure 1: Distance to the nearest branch in the Phrae province, Northern Thailand

Note: The red dots represent the bank branches, the grey lines the road network, and the heatmap colours show the distance to the nearest branch.

We argue that these closures were a direct result of the financial crisis, as opposed to being replaced by digital banking or informal credit. During the early 2000s, internet penetration in Thailand was under 10% nationally, and even lower in rural areas. Moreover, our branch data goes back to 1927, and we observe no closures at all until the crisis period. The turning point for salient digitisation came relatively late in 2017 with the introduction of the PromptPay system (Bank of Thailand 2018). Rural areas still suffer from spotty internet and more intensive use of currency.

The main goal of our research is to quantify the impact of the crisis on financial access through the branching channel. Because it is impossible to do this using experimental methods, we build and estimate a model of branch network expansion and use this to predict how the branch network would have evolved in the absence of the crisis.

A structural model of bank branch networks

In our model, banks optimally choose to open and close branches in different local markets throughout the country. The profitability of a branch location depends on local demand, the level of competition from rival commercial and government bank branches, and how much a branch cannibalises profits from the bank’s existing branches. Banks are forward-looking, taking into account how local demand will evolve over time and how opening a branch will boost local demand growth. Banks also anticipate how rival banks will respond to their entry. In the model, the crisis arrives unexpectedly and generates large losses and liquidity issues for the bank. Thus, the crisis can cause closures beyond what would be predicted just by changes in local demand or long-term branch profitability. The crisis also shifts banks’ expectations of future local growth rates.

We use two main data sources to estimate our model. The first is data on the geographic coordinates and dates of all branch openings and closings throughout the country. The second is local demand data. Thailand does not publish administrative local GDP at a fine geographic level, so we construct local demand from satellite data, measuring nighttime light intensity, which we then calibrate inter-temporally using provincial GDP data.

We find that bank entry deters rivals despite the positive effect on local demand. Our model estimates show that opening a branch entails a significant investment cost, which can explain why banks did not reopen branches in many locations after the crisis. Before the crisis, local GDP growth was high, and these expectations of future growth made it optimal to enter despite the large entry cost. After the crisis, even though the level of local GDP was higher than pre-crisis levels, the lower growth rate made entry prospects less favourable. Banks were hence less likely to reopen these branches – even though the branches that closed were now more profitable than before the crisis. Thus, our dynamic model can explain why banks opened these branches before the crisis but did not reopen them after the crisis.

Simulating a world without the crisis

With the estimated model, we simulate how the branch network would have evolved in the absence of the crisis. One approach would be to assume the economy continued along its pre-crisis trend. However, the high growth rate before the crisis was arguably unsustainable. Instead, we assume that GDP grew the same amount over our sample period (1992–2009) as in the data, but in a smooth way, without the large recession and liquidity issues for the banks. In this scenario, there is less pre-crisis entry compared to the baseline scenario, but it avoids the large number of branch closures when the crisis arrives. By 2007, ten years after the crisis, there are 7.2% more branches and 4.8% more markets served by at least one branch.

We then calculate the distance to the nearest branch for each village under both scenarios. We combine this with estimates from Ji et al. (2023), who report estimates of the impact of distance to the nearest branch on financial access using Thai data from our sample period. We find that financial access would have been 7.4 percentage points higher in the absence of the crisis, against a baseline of 43.6% in 1996.

We also use our model to estimate the impact of a reasonably sized branch subsidy for banks operating in vulnerable markets. We classify a market as vulnerable if it has only one bank branch and falls within the lowest income quintile. We find that the subsidy increases the number of branches by 1.8%, and the share of markets served by at least one branch by 3.3%.

Policy implications for financial crises

Our results highlight the value of government intervention to moderate the effects of financial crises. An important lesson of our research is that branch closures in rural areas during a crisis can have long-lasting consequences for financial access and development, potentially extending the impact of a crisis long after the economy as a whole has appeared to recover.

References

Bank of Thailand (2018), "2017 Payment Systems Report."

Ji, Y, S Teng, and R M Townsend (2023), "Dynamic bank expansion: Spatial growth, financial access, and inequality," Journal of Political Economy, 131: 2209–2275.

Rysman, M, R M Townsend, and C Walsh (2026), "Bank branching strategies in the 1997 Thai financial crisis and local access to credit," Journal of the European Economic Association, jvag007.