Low prices paid to suppliers in global supply chains can raise concerns about unequal sharing of gains from exporting. New research on India’s garment sector shows that these low prices can reflect both mutually beneficial agreements and surplus capture from exporters’ bargaining leverage – knowing the relative contribution of each is essential for effective policy design.

In many export-oriented supply chains, a few large exporters purchase inputs from numerous suppliers (Zavala 2022, Dominguez-Iino forthcoming). This imbalance in the number and size of buyers (the exporters) vis-à-vis suppliers raises a natural concern: suppliers receive low prices, so gains from exporting do not reach up the supply chain (Boudreau et al. 2023, Goldberg and Larson 2023). I (Morton 2026) show how low prices can arise from two distinct forms of buyer power, both of which emerge from buyers’ responses to poorly functioning markets. Distinguishing between these sources of buyer power matters because they imply different buyer-supplier sharing of gains and different policy remedies.

First, large buyers mitigate market frictions through agreements with suppliers. For example, if suppliers face challenges accessing formal credit markets, the buyer might provide trade credit instead. Then, input prices can be low because they combine the payment for the input with interest on trade credit. Similarly, if the buyer provides insurance, input prices combine payment for the input with an insurance premium. While these discounts still technically reflect buyer market power (as the input price can fall below the input’s value to the buyer), they are not purely extractive: discounts compensate the buyer for the surplus created inside the agreement.

Second, when markets function poorly, buyers often respond by producing inputs in-house alongside external sourcing (partial vertical integration). Integration can strengthen the buyer’s bargaining position: the buyer can threaten replacement with in-house production unless suppliers accept lower prices. Resulting discounts represent surplus capture: surplus reallocated to the buyer.

I quantify these two sources of buyer power, studying a large export-oriented Indian garment manufacturer that built a substantial in-house mill providing approximately 20% of its fabric. Although this setting seems favourable for surplus capture through replacement threats, I find that discounts instead reflect surplus created through insurance. Nevertheless, the buyer retains the majority of agreement surplus created (~60%).

Buyer-supplier partnerships and partial vertical integration in Indian fabric sourcing

The Indian garment manufacturer sources fabric from three supplier groups:

- Long-term agreements with 19 regular suppliers (~25% of fabric).

- Two internal fabric suppliers, with one built in the middle of the timeframe studied (~20% of fabric each).

- Over 400 occasional suppliers with no partnership agreement with the buyer (the remainder). These are ‘spot’ suppliers: they sell ‘on the spot’ at the market price, without any agreement for insurance or trade credit.

Buyer-supplier agreements feature a discount in exchange for insurance. Garment manufacturing involves unpredictable, variable order sizes (and suppliers cannot share orders because fabric within one order must be perfectly identical). When orders are too large, suppliers face high costs, such as overtime wages for overnight production. Alternatively, when orders are too small, revenue may not cover fixed bills like payroll. This profit volatility is challenging for suppliers, especially those that cannot access financial institutions to use savings and borrowing as a buffer. I refer to suppliers’ valuation of profit stability as ‘preferences for smooth profits’.

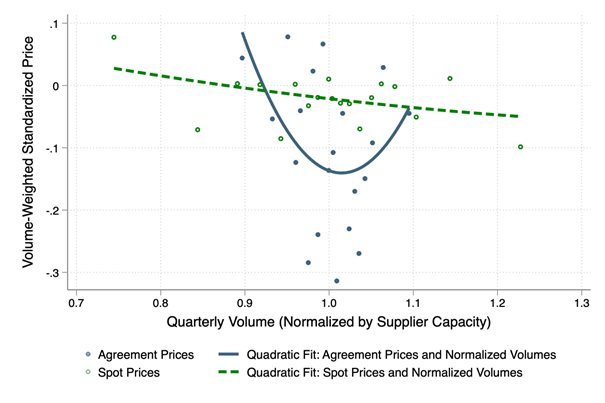

In addition to quantity insurance, agreements provide profit insurance through price adjustments. Suppliers offer a discount on average in exchange for higher prices in unprofitable periods – for both large and small orders. Specifically, prices are U-shaped with respect to supplier capacity: high at both low volumes (covering fixed costs, like payroll) and high volumes (covering high variable costs, such as overtime), but low for medium orders. In effect, the discount on average that suppliers offer serves as their insurance premium.

The buyer faces a different problem: spot suppliers charge very high prices – about 7% over costs. These high prices reflect that once end clients such as Gap or Old Navy approve a garment prototype (a ‘sample’), the buyer must return to the same fabric supplier for the entire order. Switching suppliers risks a fabric mismatch and order rejection. Spot suppliers know the buyer is locked in and set prices accordingly. Agreements benefit regular suppliers through insurance and the buyer through discounts.

Figure 1: U-shaped agreement prices, but flat spot prices

Note: The figure shows binned prices and quantities, normalised for interpretation, using 20 quantiles.

Why integration need not enable surplus extraction

At first glance, building an in-house mill not only enables sourcing at low cost but also gives the buyer additional leverage: a new replacement threat against regular suppliers. However, my model of buyer-supplier agreements shows how spot suppliers restrain that threat.

When the buyer threatens a regular supplier to cut prices or face replacement, the supplier leaves the agreement if it values insurance less than the price reduction. Then, the agreement dissolves; the supplier switches to other buyers, who are readily available, as the buyer studied purchases less than 0.5% of Indian fabric. Once an agreement breaks, the buyer must increase spot sourcing, without any discount. The buyer cannot source more from regular suppliers, as agreements mandate stable quantities, nor its own mill, as producing over capacity is costly.

Therefore, the buyer chooses not to make replacement threats to preserve the agreement discount, unless the supplier values insurance enough to accept lower prices. This restraint on replacement threats differs from settings without a spot market. For example, replacement threats have large price effects in negotiations between US hospitals and insurance companies (Ho and Lee 2019). Importantly, this coexistence of spot, integrated, and agreement sourcing is likely especially common in settings with weak market institutions.

Quantifying surplus creation and capture

Using detailed data on ~35,000 fabric purchases (worth ~$180 million annually), I decompose discounts into surplus creation and capture. The central measurement challenge is that average prices reflect two different forces: i) supplier preferences for smooth profits, and ii) bargaining positions that shape surplus sharing. To separate these two, I estimate supplier preferences for smooth profits. These preferences determine both i) how much surplus the agreement creates, and ii) whether the supplier values insurance enough for the buyer to leverage replacement threats to push down prices.

I develop a new approach to measure these preferences by examining how prices adjust to different order volumes, reflecting shifts in demand from Gap, Old Navy, and other clients. Prices for suppliers who value insurance move with order size (the U-shape), whereas prices for suppliers who do not value insurance remain flat. After ‘netting out insurance value’, the remaining discount reveals the buyer’s surplus share.

I find that agreement discounts entirely reflect surplus creation from insurance, not capture from replacement threats. This result arises because observed agreement suppliers are large with limited preferences for smooth profits.[1] Therefore, the buyer cannot make replacement threats without breaking agreements.

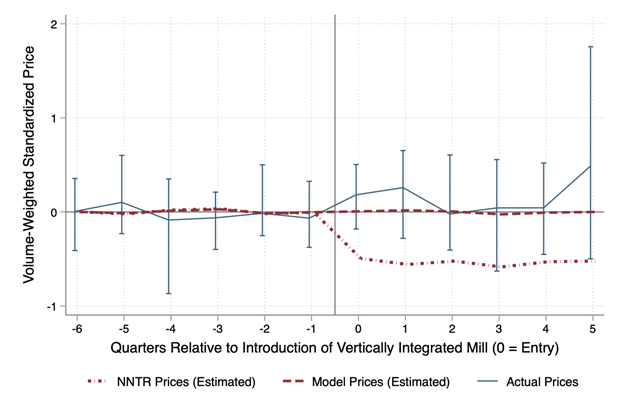

A distinct second test further establishes the lack of surplus capture from replacement threats. Specifically, when the buyer built a large internal fabric mill, increasing the buyer’s ability to make replacement threats, prices to agreement suppliers did not fall. Instead, the buyer reduced purchases from spot suppliers – the high-price ‘suppliers of last resort’. This result differs from a standard model of replacement threats – Nash-in-Nash with Threats of Replacement (‘NNTR’) – that predicts large price reductions. The key difference is that the standard model (NNTR) considers a setting without spot suppliers.

Figure 2: Agreement prices do not respond to increased integration (unlike an NNTR model)

Note: The figure shows the causal effects of increased integration on prices. Estimates compare prices for agreement suppliers exposed to the new mill, based on the fabrics they sell before the mill is constructed, to agreement suppliers unexposed to the mill before and after the mill is built (i.e., a difference-in-differences design). Treatment effects are shown for: 1) prices estimated from an NNTR model, 2) prices estimated from my model, and 3) actual prices.

But what about really small suppliers?

While the suppliers I observe are relatively large, policymakers might worry about smaller suppliers: for example, 95% of Indian manufacturing firms have 10 employees or fewer. Small suppliers are also the firms with the largest benefits from insurance, trade credit, and other support that a buyer can provide.

For these very small suppliers, my model implies a different story: their need for stable profits allows the buyer to leverage replacement threats to capture surplus. Their discounts reach up to 6.7% of spot prices – larger than India's value-added tax on clothing at the time (5%) and nearly as large as the spot market markup (7%).

Policy lessons: The source of market power reveals the remedy

These findings suggest rethinking conventional emphasis on increased buyer competition to support small suppliers. In my model, more competition has minimal effect on the smallest suppliers: their discount drops from 6.73% to 6.67% of spot prices.

Instead, the most effective policies help small suppliers smooth profits, such as:

- Better access to credit and savings (enabling self-insurance)

- Cooperatives that pool risk or protect prices

- Financial products that protect against volatility

These policies target the source of the buyer’s market power: its role as the monopolist insurance provider because insurance only emerges within an agreement. (Similarly, the buyer is typically the monopolist credit provider when agreements incorporate trade credit).

More broadly, these results suggest that helping small firms smooth profits can advance two goals at once. Not only does profit smoothing improve efficiency – the standard argument for insurance – but it can also further equity by strengthening small firms’ bargaining positions. Smoothing profits can be especially challenging for small firms in low- and middle-income countries facing substantial uninsured risk: Banerjee and Duflo (2011) describe these firms as low-income ‘hedge fund managers’ in Poor Economics.

References

Banerjee, A, and E Duflo (2011), "Poor economics: A radical rethinking of the way to fight global poverty," PublicAffairs.

Boudreau, L, J Cajal-Grossi, and R Macchiavello (2023), "Global value chains in developing countries: A relational perspective from coffee and garments," Journal of Economic Perspectives, 37(3): 59–86.

Dominguez-Iino, T (forthcoming), "Efficiency and redistribution in environmental policy: An equilibrium analysis of agricultural supply chains," Journal of Political Economy.

Goldberg, P, and G Larson (2023), "The unequal effects of globalization," Unpublished manuscript.

Ho, K, and R Lee (2019), "Equilibrium provider networks: Bargaining and exclusion in health care markets," American Economic Review, 109(2): 473–522.

Morton, R (2026), "Value creation and value capture in Indian garment sector bargaining," Unpublished manuscript.

Zavala, L (2022), "Unfair trade? Monopsony power in agricultural value chains," Unpublished manuscript.