Hometown auditors report lower suspicious expenditures, implying that social ties are associated with greater leniency

Government investment provides essential (and potentially very productive) public amenities, such as transport infrastructure and schools. At the same time, public investment may be prone to corruption, with corrupt officials siphoning off funds or awarding procurement contracts on the basis of whoever offers the biggest bribe (Tanzi 1998).

One common prescription to limit theft from and mismanagement of public projects is the threat that misdeeds will be uncovered via audits, which would prevent officials from behaving badly in the first place. There is, of course, the age-old question of “who watches the watchers?”1 This concern may be particularly severe if the watchers are somehow connected to those they are meant to be watching, and hence willing to turn a blind eye to their transgressions. Conflict-of-interest rules – common to any audit relationship – limit the most obvious relationships between monitor and target. Our children, for example, couldn’t hire us to audit their workplace behaviour. But less visible – and less obvious – connections may nonetheless compromise the objectivity of oversight.

Auditing municipal governments in China: ‘Hometown connections’

We document one such case in audits of municipal governments in China by provincial auditors, by using a widely recognised form of social tie and source of favour exchange in Chinese society and elsewhere, namely, ‘hometown connections’ (Fisman et al. 2018, Hodler and Raschky 2014). Municipal audits in China are overseen to a large extent by provincial audit departments which are headed by a single chief auditor. We conjecture that this top auditor, when scrutinising public expenditures in his own hometown, may be more willing to show leniency towards municipal officials.

We explore this hypothesis of ‘hometown favouritism’ towards local officials by examining the outcomes of audits in 277 Chinese prefectures during the years 2006-2016 (Chu et al. 2020). The interested reader can learn more of the details of Chinese audit rules and regulations in our paper. For our purposes, we summarise by observing that audits of many municipal expenditures (e.g. very large infrastructure projects) are directly overseen by provincial audit departments. And even when a city’s own audit department carries out inspections, the provincial audit department still has a supervisory role, as the city chief auditor’s boss is the provincial chief auditor. In summary, the provincial chief auditor wields considerable power in how audits are conducted throughout their domain.2

Identifying the consequences of hometown ties

A key feature of Chinese audits and the audit bureaucracy helps us in identifying the consequences of hometown ties. Like many top officials in China, provincial chief auditors are frequently rotated amongst jobs (such auditor rotation is quite common more generally around the world, to limit auditor-target collusion). Consider, for example, the cities of Nantong and Yangzhou, both located in Jiangsu province. Imagine furthermore that Jiangsu’s chief auditor is initially from Nantong, and is replaced by one from Yangzhou. By examining the shifts in audit leniency as a result of this transition, we may more convincingly link audit quality to hometown ties rather than some other difference between the two cities. Furthermore, because China’s municipalities must report both total city expenditures as well as the expenditures that raised red flags for auditors, we have a ready measure of audit intensity, particularly around the time auditor transitions take place. The inner-workings of the Chinese bureaucracy are sufficiently opaque that it is extremely unlikely that Yangzhou’s officials know they’ll have a hometown auditor the following year rather than one from, say, Changzhou, or from outside the province altogether.

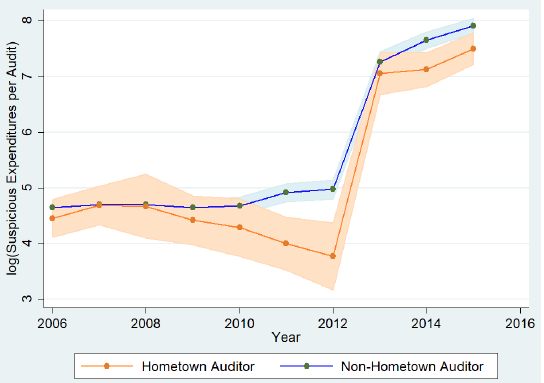

Hometown auditors report lower suspicious expenditures

Our main results can be seen in Figure 1, which graphs the fraction of city expenditures that auditors identify as suspicious, splitting the sample based on whether the provincial chief auditor was born in that city. The first pattern that jumps out at the reader is the large increase in suspicious expenditures in 2013. This will surprise no one with even casual knowledge of Chinese politics – Party Secretary Xi Jinping initiated his still-ongoing anticorruption crackdown in that year. Note also the fairly consistent gap between hometown and non-hometown auditors – in all years but one, hometown auditors report lower suspicious expenditures.

Figure 1 The average of log(Suspicious Expenditures per Audit) across years for different auditor backgrounds

While it is possible that a well-connected and well-informed hometown auditor may more effectively deter misbehaviour, as we noted earlier, even in their very first year of office, a hometown auditor uncovers less suspicious expenditures, which argues against this ‘deterrence’ interpretation. We also look at what happens in the years when one of the city's top two officials (the party secretary and the mayor) leaves office. In such years, the province’s Organisation Department, amongst the most powerful departments in the province – watches over the city’s audit, to make sure that the outgoing officials were not themselves corrupt.3 We find that in these cases – when Organisation Department oversight likely constrains the province’s chief auditor — the hometown auditor effect is cut in half (that is, we observe less hometown favouritism when one of the city's top two officials leaves office).

Policy implications

Finally, our finding that social ties are associated with greater leniency in oversight has direct policy implications for the design of conflict-of-interest rules. In general, there is a trade-off in restricting well-connected candidates from monitoring positions: a locally connected monitor may have better information or ability to enforce compliance than an outsider, an advantage that needs to be weighed against the costs of potential favouritism. Our results suggest that favouritism may be a dominant factor in our setting, which provides a rationale for the existence of rules against assignment to one's home region, precisely to reduce the potential for collusion or self-dealing.

References

Chu, J, R Fisman, S Tan, and Y Wang (2020), “Hometown favoritism and the quality of government monitoring: Evidence from rotation of Chinese auditor”, conditionally accepted for American Economic Journal: Applied Economics.

Fisman, R, J Shi, Y Wang and R Xu (2018), "Social ties and favoritism in Chinese science", Journal of Political Economy 126.3: 1134-1171.

Hodler, R and Paul A. Raschky (2014), "Regional favoritism", The Quarterly Journal of Economics 129.2: 995-1033.

Tanzi, V (1998), "Corruption around the world: causes, consequences, scope and cures", IMF Staff Papers 45.4: 559-562.

Endnotes

1 The term originates with the Roman poet Juvenal, who wrote in his Satires, “Quis custodiet ipsos custodes?”

2 And yes, the provincial chief auditors are almost all men. While more women have attained higher-level offices in China in recent years, the upper echelons of the bureaucracy in China (as elsewhere) are very much male dominated

3 The Organization Department is responsible for, amongst other things, promotions through the bureaucracy, so it takes a particular interest in the probity of outgoing officials.