In January 2022, the US suspended Ethiopia’s eligibility for the African Growth and Opportunity Act, ending Ethiopia’s preferential trade access to the US market, and leading to a major increase in tariffs, the loss of key buyers, and, at some companies, mass layoffs. New evidence shows that losing these formal jobs had lasting negative impacts, highlighting the importance of expanding job-loss support and changing its current design.

Editor’s note: For a broader synthesis of themes covered in this article, check out our VoxDevLit on Barriers to Search and Hiring in Urban Labour Markets.

In many low-income and lower-middle-income countries (LICs and LMICs), much of the policy discussion focuses on creating formal sector jobs, particularly in export-oriented manufacturing. But as these formal sectors expand, so too does exposure to shocks, often with little social protection available to those workers who lose their jobs.

These challenges are particularly salient today, as trade disruptions and global instability threaten jobs across the world. In the last year, for example, export-oriented manufacturers in LICs and LMICs have experienced several rounds of US tariff changes and now have to face elevated energy costs. Such shocks can trigger buyer exits, order collapses, and sudden layoffs of large numbers of employees. And if displaced workers are unable to quickly secure similar jobs, structural transformation slows down, and the worker-specific training and migration investments often needed to drive such transformation are lost.

In high-income countries, unemployment insurance helps those workers displaced by these shocks to maintain their level of consumption while searching for a new job. However, in most LICs and LMICs, unemployment insurance systems are absent. The only job-loss protection is severance pay – a lump-sum payment typically funded by the employer.

But how long-lasting are the consequences of job loss in a lower-income country, and do displaced workers need additional protection? Could alternative policy designs – such as distributing payments in tranches – better support worker welfare and labour market recovery? We lack evidence on these questions (Gerard et al. 2026).

Our research (Hensel et al. 2026) advances these questions by studying a sample of Ethiopian young female garment workers who lost employment after Ethiopia’s sudden loss of preferential US market access in 2022 – a population and setting that resemble many displacement episodes in export manufacturing, including those driven by today’s trade-policy volatility.

The African Growth and Opportunity Act tariff shock

In January 2022, Ethiopia’s rapidly growing apparel and textile sector experienced a major shock when the US suspended Ethiopia’s eligibility for the African Growth and Opportunity Act (AGOA). The AGOA suspension abruptly ended Ethiopia’s preferential trade access to the US market, resulting in a major increase in tariffs, the loss of key buyers and, sometimes, mass layoffs. In the Hawassa Industrial Park, a garment-focused manufacturing hub, the firm that we focus on in this study laid off more than 2,000 workers in response to this shock. However, many of the other firms in the park were less affected, as they had more diversified buyers’ networks in Europe and Asia, and, during the time frame of our study, generally did not lay off workers en masse.

Research design: Quasi-experimental and experimental evidence

In our research, we first provide quasi-experimental evidence on the consequences of job loss for this population of workers. We then explore experimentally the impacts of providing additional financial support, and how the structure of this support affects employment and welfare. To do this, we survey a random sample of laid-off formal workers in the study firm, and a second sample of comparable workers in a similar garment firm in the Hawassa industrial park, which was less affected by the shock and did not engage in mass layoffs.

For the experimental analysis, we divide the sample of displaced workers in three groups. A control group, who receives the Ethiopian statutory severance pay, which is equivalent to roughly two and a half months of wages, but no experimental payments. A lump-sum group that receives statutory severance pay and an additional one-time payment, worth about three months of wages. And a monthly group that receives statutory severance pay and an equivalent total top-up amount as the lump-sum group, but disbursed in equal tranches over five months. Overall, the additional funds provided as part of the experiment approximate the replacement rate and duration of unemployment insurance available to workers in upper-middle income African countries, such as South Africa or Egypt.

For the quasi-experimental analysis, we compare the outcomes of the displaced workers assigned to the control group to those of the group of similar workers sampled in the unaffected firm, who remain employed at high rates throughout the study period. These two groups are highly comparable in terms of demographics and job characteristics at baseline.

Job loss generates large and persistent welfare losses

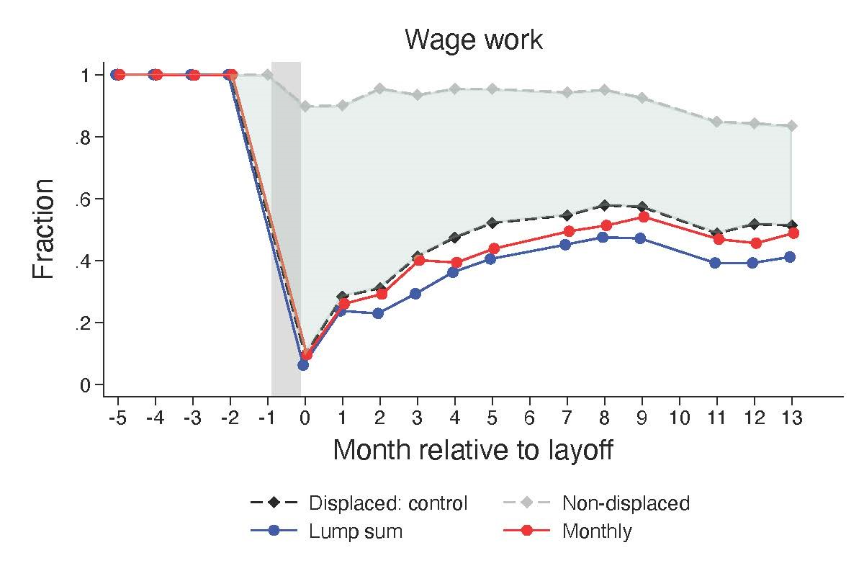

We find that job loss has persistent negative effects for the formal workers in our sample. About 14 months after displacement, the wage-employment rate among displaced workers was roughly 32 percentage points lower than among non-displaced workers. Many displaced workers left Hawassa: they were about 21 percentage points more likely to have left the city compared to their non-displaced peers, often to return to the small towns and rural areas where they grew up. And while some displaced individuals started a business, rates of self-employment remained very low throughout the period (as new businesses fail at high rates).

Labour income fell by roughly 50%, and total consumption expenditures declined by about 10% on average – reaching about 14% below baseline levels by the end of our main follow-up window. Extreme consumption poverty more than doubled. Informal transfers from family and friends partially offset income losses but were insufficient for full consumption smoothing.

The magnitude of these impacts is striking, especially when compared to prior studies of job loss in high- and middle-income countries. For example, one year after displacement, employment losses among the female factory workers in our study were roughly twice as large as those documented for similar time horizons in the US (Fallick et al. 2025) and Sweden (Athey et al. 2026). These large effects also imply that displacement shocks like the one in our study destroy a large proportion of the worker-specific training and migration investments that were incurred to create the sector in the first place

Figure 1: Wage work

Financial support can make a difference, but how it is delivered matters for both welfare and reemployment

Additional financial support can meaningfully reduce the consumption loss caused by job loss, but this crucially depends on how this support is delivered.

Lump-sum payments led to sharp spikes in consumption expenditure immediately following displacement, but those gains faded quickly; the time-averaged effect on expenditure over the follow-up was far smaller than for monthly payments (in our estimates, roughly three-quarters smaller). Lump-sum payments also reduced manufacturing employment persistently – by about 11 percentage points relative to monthly payments 14 months after job loss – and increased out-migration by about 8 percentage points, without a lasting offsetting rise in self-employment.

On the other hand, monthly payments improved consumption smoothing: on average, they offset about 40% of the decline in total expenditure induced by job loss over the 14 months we study, and helped stabilise spending over time. They also reduced expenditure poverty by about 3 percentage points on average (about one-eighth of the mean among control workers). Crucially, simply changing the modality of disbursement from lump-sum to monthly payments mitigates the effect of additional support on wage employment or migration in the long run.

Our heterogeneity analysis sheds light on the mechanisms behind these results and shows that these responses were partly predictable at baseline. The short-run spending surge among workers who received a lump sum was concentrated among workers who had expressed a strong preference for receiving support in monthly instalments – consistent with self-control motives for wanting tranche payments. By contrast, the employment and migration costs of lump-sum support were concentrated among workers who did not express a strong preference for monthly payments at baseline, for whom the lump sum appears to have enabled a durable move away from manufacturing work in Hawassa, as well as a pivot towards different family outcomes (compared to monthly tranches, lump-sum payments raise marriage and fertility among these workers and reduce investment in education).

Welfare trade-offs: Private surplus, public budgets, and industrial policy

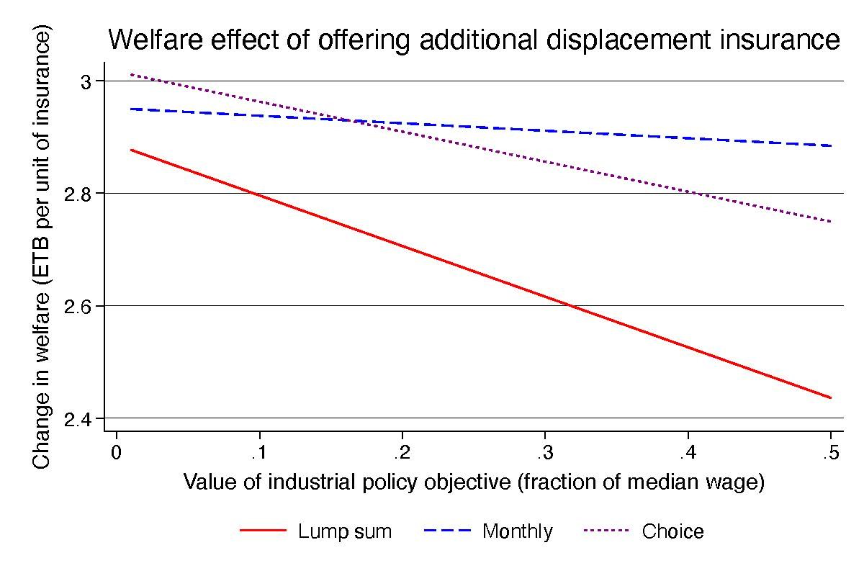

To evaluate the overall welfare, we analyse three ingredients that together determine the social value of expanding or restructuring support: workers’ private surplus from insurance, which we estimate through an incentivised willingness to pay exercise, the fiscal externality from the reduction in formal employment generated by expanded insurance, and an “industrialisation” externality that captures the external value of the worker-specific investments incurred in training and migration.

Figure 2: Welfare effect of offering additional displacement insurance

Three implications stand out. First, for any disbursement modality, expanding job-loss insurance would substantially increase social welfare in this setting. Our willingness-to-pay exercise reveals a high private value for expanded coverage, with the vast majority of workers being willing to pay for additional insurance above actuarially fair rates. Further, this large private surplus considerably exceeds the likely externalities, implying that an expansion of job-loss insurance would raise social welfare. In Figure 2 we show the magnitude of this gain: depending on the disbursement modality and the size of the industrialisation externality, an extra Ethiopian Birr offered in insurance would raise welfare by 2.4–3 Ethiopian Birr.

Second, monthly disbursement raises welfare relative to lump sum transfers, which are the main form of disbursement in today’s LICs and LMICs. This is because it delivers similar private insurance value while generating smaller fiscal and industrialisation externalities.

Third, preferences over disbursement modalities are heterogeneous, which creates a trade-off between maximising workers’ private surplus and minimising externalities. Letting workers choose their preferred modality would increase the value of insurance by about 12%, but it would also exacerbate negative externalities – as some people would choose lump-sum payments and would reduce their propensity to be in wage employment as a result. In our calibration, offering choice is optimal as long as the externality from keeping a worker in manufacturing is below 16% of the median wage; above that threshold, mandating monthly disbursement becomes preferable. While the value of this externality will depend on the setting, the general lesson is that governments have to balance worker welfare and industrialisation objectives when designing optimal social insurance.

Policy implications: Job loss and social protection

Three key lessons emerge from our findings. First, job loss can generate long-lasting negative effects for formal workers displaced by trade shocks, even when statutory severance pay exists. While our estimates need not generalise everywhere, they are relevant for many female garment workers in today’s export hubs – settings exposed not only to US tariff uncertainty but also to supply shocks coming from global instability, climate change, and the threat of automation.

Second, expanding financial support can generate large welfare gains, but careful policy design is needed. Lump-sum severance pay – the default in many LICs and LMICs – provides weak consumption smoothing for many workers and can delay durable return to wage employment, without generating lasting self-employment. Policy designs that disburse a larger share of support in tranches (for example, monthly instalments), or that allow workers to choose payment modalities, deserve a more central place in the policy debate.

Finally, offering additional insurance could likely be fiscally sustainable for the government. We find that workers in Hawassa are willing to pay premiums well above actuarially fair levels implied by observed separation rates, and above the worker contributions charged in South Africa and Mauritius for comparable unemployment insurance-style coverage. In a follow-up elicitation among formally employed workers in Addis Ababa, we find similarly high demand – suggesting that the demand for stronger job-loss insurance may extend beyond our Hawassa setting.

References

Athey, S, L K Simon, O Nordström Skans, J Vikström, and Y Yakymovych (2026), "The heterogeneous earnings impact of job loss across workers, establishments, and markets," NBER Working Paper No. 34946.

Fallick, B, J Haltiwanger, E McEntarfer, and M Staiger (2025), "Job displacement and earnings losses: The role of joblessness," American Economic Journal: Macroeconomics, 17(2), 177–205.

Gerard, F, G Gonzaga, and J Naritomi (2026), "Job displacement insurance in developing countries," in R Hanna and B A Olken (eds.), The Handbook of Social Protection: Evidence and New Directions for Low- and Middle-Income Countries.

Hensel, L ⓡ, G Abebe ⓡ, F Gerard ⓡ, and S Caria ⓡ (2026), "Mitigating the consequences of job loss in lower-income countries: Evidence from Ethiopia," IZA Discussion Paper No. 18537.