Bank credit can support firms during recessions in contexts where banks are sufficiently capitalised to lend. However, whether bank lending amplifies or mitigates a downturn – depends not only on banks’ fundamentals, but also on changes to their risk tolerance in the face of the downturn. During the COVID-19 pandemic in Mexico, heightened uncertainty made banks more risk-averse, leading to tightened credit conditions, despite their relatively strong fundamentals. The resulting negative credit supply shocks had sizable adverse effects on employment and firm survival, highlighting that policies limited to liquidity provision may be insufficient without mechanisms – such as credit guarantees – to counteract heightened risk aversion.

Recessions are periods of heightened risk and uncertainty, during which firms face declining demand and tighter margins. In response, some reduce their investment or workforce to stay afloat, while others are forced to exit the market altogether. These dynamics could have long-term consequences, especially when productive, small, and young firms lose momentum or shed firm-specific human capital (Clementi and Palazzo 2016). For workers, job losses during downturns often lead to persistent earnings losses and career scarring (Davis et al. 2011).

Access to credit during recessions can play a key role in helping firms weather transitory shocks, aiding in firm survival, preserving both employment and maintaining productive capacity.

The importance of credit has been well-documented during financial recessions such as the 2008 financial crisis (Chodorow-Reich 2013) and European sovereign debt crisis (Bentolila et al. 2017). In these settings, shocks to banks’ balance sheets unambiguously lead to a decrease in credit supply. Less is known about the direction, drivers, and effects of credit supply shocks during downturns in which banks’ balance sheets are not the main source of the crisis. During non-financial recessions, firms’ demand for liquidity increases while banks are ex-ante well-positioned to lend. In such contexts, bank lending could cushion or exacerbate the economic contraction, depending on the direction of the credit supply shocks and their allocation across firms in the economy. Understanding the drivers and dynamics of credit supply in these episodes is essential for designing effective policy responses.

In our research (Rivadeneira, Oviedo, and de la Parra 2025), we study how banks in Mexico adjusted credit supply during different phases of the COVID-19 pandemic – a sharp, sudden, and non-financial recession – and investigate the determinants of these adjustments, as well as its real effects.

Credit and employment dynamics during a non-financial recession

The COVID-19 pandemic severely affected the Mexican economy, with real GDP contracting by 8.5% between Q42019 and Q42020, marking the most substantial decline over three decades. Lockdowns and reduced demand, combined with heightened uncertainty, substantially increased firms’ liquidity needs and impacted their ability to operate without credit or government support. Meanwhile, the banking sector was well-capitalised and highly liquid at the onset of the crisis, allowing it to absorb liquidity pressures. Importantly, the lessons learned about the drivers and effects of credit supply during this time extend beyond this specific episode. Instead, they can be generalised to other non-financial recessions, such as those caused by natural disasters or large-scale supply chain disruptions.

Mexico has a large share of small and medium-sized enterprises (SMEs), which are heavily dependent on bank credit (Gutierrez et al. 2023). This difference in the composition of firms and their reliance on the banking sector in emerging markets potentially affects the drivers of credit supply and its effects. But previous work on the role of credit during the pandemic has focused on developed countries (Greenwald et al. 2020, Chodorow-Reich et al. 2022).

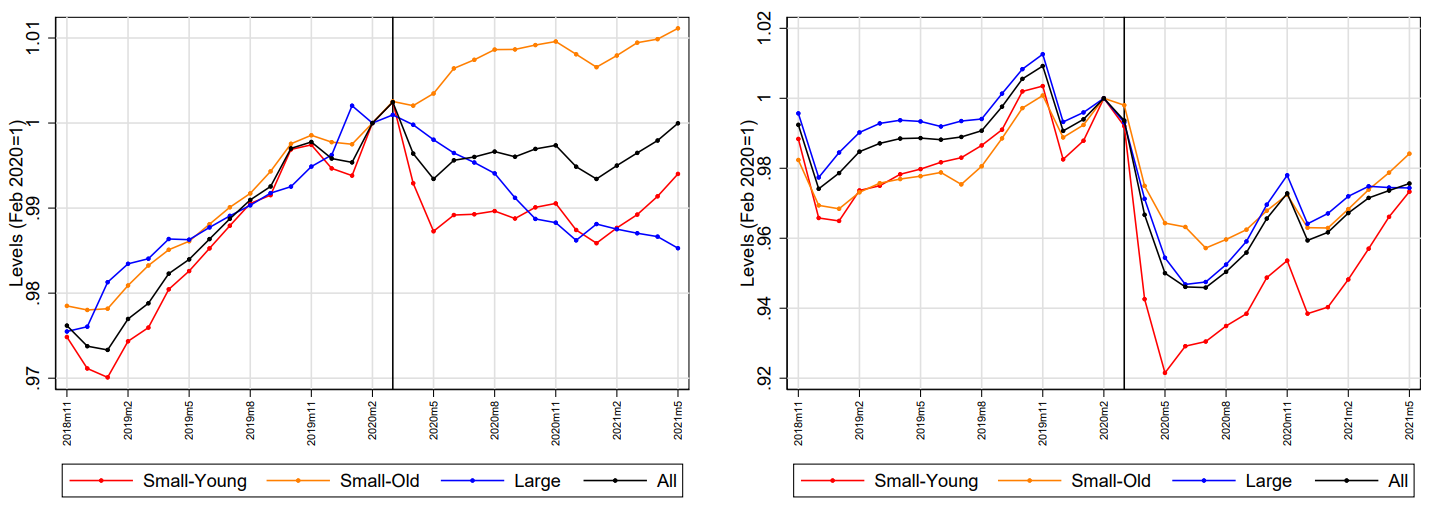

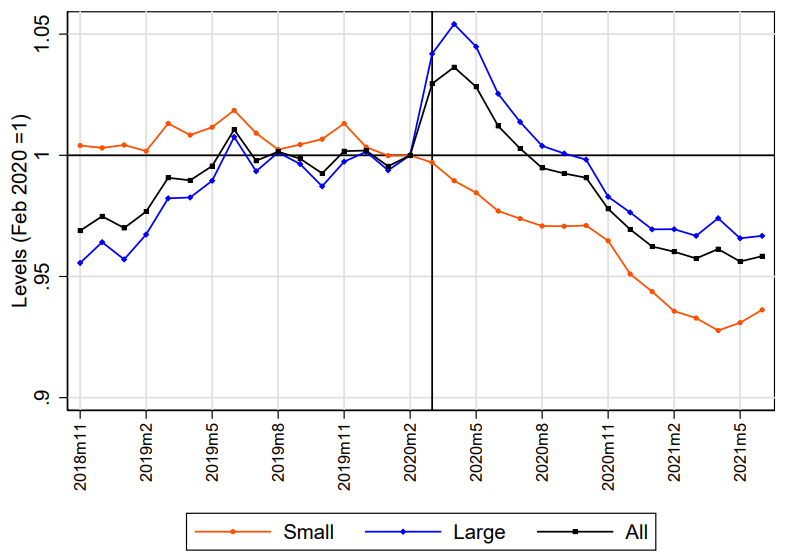

Indeed, credit and employment dynamics differed substantially between small and larger firms. In the first three months of the pandemic, around 8,300 firms (0.9%) exited the formal sector – most of which were small, young firms. While the total number of firms returned to pre-pandemic levels by mid-2021, this subset of firms did not fully recover. The total number of formal workers decreased by 5.4% during the same period. The employment trends at small, old firms and large firms closely mirrored the performance of the economy as a whole, as these firms employ close to 70% of all formal workers; while employment levels at small, young firms fell by 8%.

Credit to small firms stagnated prior to the outbreak of the pandemic and decreased during the most critical months of the crisis. An uptick in lending to these firms emerged in the second half of 2021, during the economic recovery phase. In contrast, credit to large firms initially surged between February and April of 2020, driven by increased demand for funding in anticipation of potential disruptions stemming from the pandemic. After this initial increase, a significant contraction followed until August 2021, as lending standards tightened and demand for credit dried up.

Figure 1: Firm, employment, and credit dynamics

Notes: Small firms are those with less than 100 workers, while young firms are those with less than 10 years of operation. Source: Authors’ calculations using the IMSS dataset.

What drives credit supply shocks during non-financial recessions?

Using loan-level data on the universe of commercial bank credit to formal firms in Mexico, we apply the methodology developed in Amiti and Weinstein (2018), and its subsequent refinements by Degryse et al. (2019), to identify changes in lending that are driven by bank-specific factors, from firm characteristics. This distinction is crucial, as observed credit is shaped by both firms’ performance and banks’ internal decisions, such as changes in risk tolerance or funding conditions.

Our findings show that, despite high liquidity and capital levels, many banks contracted their credit supply during the most critical months of the pandemic. Using balance sheet data and confidential information from Mexico’s Senior Loan Officer Opinion Survey on Lending Practices, we identify a key driver: a decline in banks’ risk tolerance, particularly towards large borrowers, even after controlling for portfolio quality, firms’ funding availability, and liquidity constraints. This finding is consistent with banks’ exposure to credit line drawdowns from large firms driving banks’ performance (Acharya et al. 2024) and lending conditions (Kapan and Minoiu 2021). As we detail further below, this result has crucial implications about the set of policies that are effective to foster lending during a non-financial recession.

Firms exposure to credit supply shocks and real effects

Differences in firms’ exposure to credit supply shocks affected their job destruction rates and survival probabilities. Small and young firms were more affected. Moreover, we find that credit supply shocks affected not just the level but also the composition of firms’ workforce. Employment growth experienced a larger decline among worker-types with lower adjustment costs (e.g. temporary workers and recently hired workers) at firms exposed to greater negative credit supply shocks.

Credit supply shocks accounted for roughly one-third of the total employment decline among small firms in our sample during the pandemic, an effect comparable in magnitude to that seen during the Great Recession (Chodorow-Reich 2013) and European debt crisis (Bentolila et al. 2017), despite the fundamentally different nature of the downturn.

Policy implications for non-financial recessions

Even with a well-capitalised and liquid banking sector, credit can play a decisive role in amplifying the effects of a recession. We find that the heightened uncertainty made banks more risk-averse, leading to tightened credit conditions, despite their relatively strong fundamentals. This behaviour can exacerbate economic contractions by depriving firms of the necessary liquidity.

A key takeaway is that policy tools should consider the role of risk aversion in driving lending conditions during non-financial recessions. In particular, providing liquidity to banks can be ineffective when credit contractions are not driven by such fundamentals. Instead, tools focused on mitigating risk such as credit guarantees or backstops for loans to SMEs – for example, the Paycheck Protection Program in the US (Granja et al. 2022), temporary regulatory forbearance, or accounting flexibility for banks – can be more effective during times of high uncertainty when banks’ risk tolerance is a key driver of credit supply.

References

Acharya, V V, R Engle, M Jager, and S Steffen (2024), “Why did bank stocks crash during COVID-19?,” Review of Financial Studies 37(9): 2627–2684.

Amiti, M and D E Weinstein (2018), “How much do idiosyncratic bank shocks affect investment? Evidence from matched bank-firm loan data,” Journal of Political Economy 126(2): 525–587.

Bentolila, S, M Jansen, and G Jimenez (2017), “When credit dries up: Job losses in the Great Recession,” Journal of the European Economic Association 16(3): 650–695.

Chodorow-Reich, G (2013), “The employment effects of credit market disruptions: Firm-level evidence from the 2008–9 financial crisis,” Quarterly Journal of Economics 129(1): 1–59.

Chodorow-Reich, G, O Darmouni, S Luck, and M Plosser (2022), “Bank liquidity provision across the firm size distribution,” Journal of Financial Economics 144(3): 908–932.

Clementi, G L and B Palazzo (2016), “Entry, exit, firm dynamics, and aggregate fluctuations,” American Economic Journal: Macroeconomics 8(3): 1–41.

Davis, S J, T Von Wachter, R E Hall, and R Rogerson (2011), “Recessions and the costs of job loss,” Brookings.

Degryse, H, O De Jonghe, S Jakovljević, K Mulier, and G Schepens (2019), “Identifying credit supply shocks with bank-firm data: Methods and applications,” Journal of Financial Intermediation 40: 100813.

Granja, J, C Makridis, C Yannelis, and E Zwick (2022), “Did the paycheck protection program hit the target?,” Journal of Financial Economics 145(3): 725–761.

Greenwald, D L, J Krainer, and P Paul (2020), “The credit line channel,” Federal Reserve Bank of San Francisco.

Gutierrez, E, D Jaume, and M Tobal (2023), “Do credit supply shocks affect employment in middle-income countries?,” American Economic Journal: Economic Policy 15(4): 1–36.

Kapan, T and C Minoiu (2021), “Liquidity insurance vs. credit provision: Evidence from the COVID-19 crisis.”

Rivadeneira, A, C Alcaraz, N Amoroso, R Oviedo, B Samaniego de la Parra, and H Sapriza (2025), “Credit supply shocks during a non-financial recession.”