In India, a guaranteed income programme acted as insurance rather than a substitute for credit, reducing downside risk for small farmers and increasing their willingness to borrow – unlocking large credit-financed gains in investment, productivity, and income.

For decades, development economists have observed a frustrating disconnect: microenterprises in poor countries have extraordinarily high returns to capital, yet credit expansion does little to unlock investment. Research finds that while handing cash to farmers and small-business owners increases productivity, simply expanding access to credit has little effect (Woodruff 2018, Kremer et al. 2019). The question remains: why would entrepreneurs leave money on the table?

The conventional answer – credit constraints – does not quite fit. Microfinance schemes and banking deregulation, for instance, have all expanded credit supply without proportionally increasing enterprise growth. This suggests that there is another constraint at play.

Evidence from a natural experiment in India that provided guaranteed income to all landowning farmers suggests that the binding constraint on their investment may be uninsured risk. Rather than more credit, what farmers need is credible downside protection that makes them willing to use existing credit for productive investment. Framing universal basic income (UBI) as an unconditional amount guaranteed to small entrepreneurs can protect them against downside risk, thereby offering a promising solution.

India's accidental experiment

In March 2019, India launched PM-KISAN, an unconditional guaranteed income programme delivering INR 6,000 annually (US$285 PPP) to every landowning farmer. The transfer is modest relative to annual farm income, roughly 7%, but permanent, universal, and uniform regardless of household wealth or effort.

What makes this policy useful for causal inference is that the state of West Bengal refused to implement the programme, creating sharp geographic discontinuities: farmers in border districts of adjacent states received the benefit, while identical regions just across the boundary received nothing.

In our research (Ghosh and Vats 2025), we exploit this spatial discontinuity along state boundaries to compare adjacent villages that differ only in programme exposure. Specifically, we combine this natural experiment with satellite imagery, administrative data, bank lending records, and farmer surveys to trace the policy's effects from fields to balance sheets.

Impact of guaranteed income on agricultural productivity

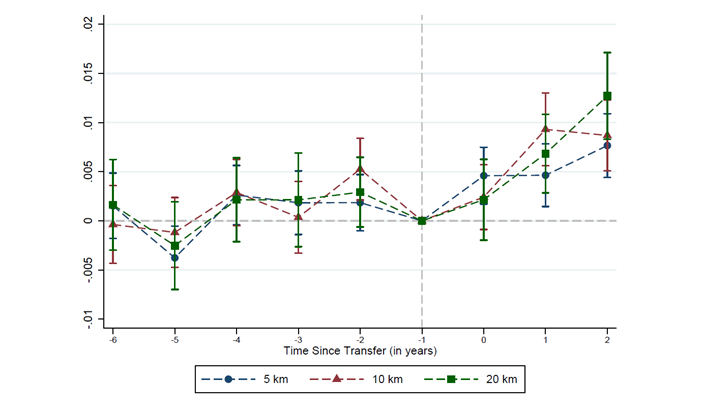

The productivity gains were substantial. Using satellite-based vegetation indices as a proxy for agricultural output, we find that treated regions experienced productivity improvements of 7.4–9.1% relative to identical neighbouring areas just across the border (see Figure 1). Household income of treated farmers rose 15.8% compared to otherwise similar farmers in noncompliant districts.

Figure 1: Effect of guaranteed income on agricultural production in treated areas relative to adjacent control areas

What explains the rise in production and income?

We argue that this increase in agricultural productivity and income is driven by a shift towards a more capital-intensive mode of production. We document that investment surged dramatically for treated farmers compared to otherwise similar farmers in adjacent noncompliant districts. For instance, tractor sales increased 12–14%, fertiliser use rose 32%, and cultivated area expanded 48–55%. These findings indicate that the cash transfers facilitated both lumpy investment in agricultural machinery and higher expenditure on variable inputs, enabling farmers to expand production.

What finances this increased investment?

The magnitude of the increase in investment is striking as it exceeds the direct cash transfer of INR 6,000. For instance, a tractor costs approximately INR 700,000, which is over 115 years' worth of annual PM-KISAN benefits. Clearly, farmers were not simply using the transferred cash to finance these new investments. We argue that this increase in investment is financed using borrowing. Using the universe of formal lending data, we document that agricultural lending increased by 7.2% in treated areas.

Returns to guaranteed income

Using farmer-level data, we find that each additional dollar of guaranteed income generates approximately $1.76 in additional income, by inducing a shift towards more capital‑intensive production financed with credit. A one‑dollar increase in guaranteed income raises term loans by $6.78 and credit‑card borrowing by $3.33, for a total credit increase of $10.12, around 58.68% of the transfer’s perpetuity value. Loan composition shows that this new borrowing finances productive assets rather than consumption or short‑term liquidity. Assuming a loan‑to‑value ratio of 0.8, the policy generates an upper‑bound increase in capital of $11.81 ($8.48 from term loans and the rest from credit cards), roughly 68.52% of the transfer’s perpetuity value, and implied returns to capital of at least 14.90%.

Figure 2: Linking guaranteed income to credit, investment, and income from work

Survey evidence from 4,000 farmers closely matches these patterns, and hypothetical responses from non‑recipient tenant farmers look similar, suggesting that these behavioural responses would likely generalise if transfers were extended beyond current beneficiaries.

The credit demand channel

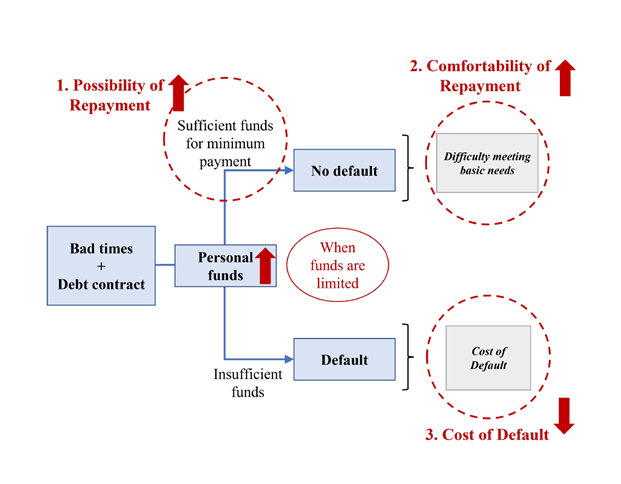

We next show that the rise in credit for small farmer-entrepreneurs is driven by a demand-side mechanism. Guaranteed income raises borrowers’ willingness to take loans by making repayment in bad times more feasible, ensuring basic needs can still be met after repayment, and lowering the expected consumption loss from default (Figure 3).

Our most potent evidence on the demand side channel of guaranteed income comes from Kisan Credit Cards (KCC), whose limits and interest rates are fixed by design and unaffected by the policy, so they isolate changes in credit demand from changes in supply. After the reform, KCC utilisation rises by 5.8 percentage points for treated farmers, indicating the existence of a credit demand effect among the treatment group.

We further supplement our analysis by examining the policy’s effect on suggestive proxies for credit demand and supply. We find a 1.7% increase in the number of applications, corresponding to a 41% increase over the sample mean. Meanwhile, we do not observe economically meaningful changes in the probability of acceptance. Overall, the results show that treated farmers submitted more credit applications following the policy, while their acceptance rates remained unchanged.

Figure 3: How guaranteed income increases credit demand

Finally, survey evidence reinforces this channel: around 80% of farmers report that higher credit demand, not improved credit availability, was the primary channel through which the policy increased their borrowing.

Why risk matters in agriculture

Agriculture is exposed to large, uninsured income shocks from volatile rainfall. When farmers borrow for lumpy investments like tractors or land expansion, they face fixed repayments regardless of harvest outcomes, so a bad crop quickly creates a binding liquidity crunch. Default brings lasting consumption losses and reputational damage, while repaying by cutting spending below subsistence is intolerable, so farmers rationally under-borrow even when expected returns are high. Guaranteed income changes this calculus by providing a permanent safety net that continues even when farm earnings collapse, lowering the cost of the worst-case state and making borrowing acceptable.

To further shed light on the underlying mechanism, we elicit the beliefs of PM-KISAN recipients to understand the motivations driving their increased willingness to borrow. 22% of respondents said that guaranteed income increased their credit demand by increasing their comfort in meeting basic needs after loan repayment during bad times. 40% of respondents rated the reduction in the (expected) cost of default, i.e. reduced consumption loss, as the primary reason through which guaranteed income increased their credit demand. 21% of respondents rated reduction in probability of default as the primary reason for increased credit demand.

Lastly, we document a decline in delinquency rates among agricultural borrowers following the programme rollout. This suggests that guaranteed income provides a buffer that helps borrowers weather temporary income shocks without missing repayments.

Policy Implications for agriculture

India's PM-KISAN experiment reveals that guaranteed income programmes for businesses do not necessarily discourage enterprise. Instead, by cushioning downside risk, these programmes catalyse productive investment when combined with formal credit access. Our findings suggest that the binding constraint on small-enterprise investment is not necessarily credit access. Where uninsured income risk is large and formal insurance is weak, it is risk itself. Guaranteed income can unlock credit demand and productive investment simultaneously by reducing that downside risk.

References

Ghosh, P, and N Vats (2025), “Safety nets, credit, and investment: Evidence from a guaranteed income program,” Unpublished manuscript.

Kremer, M, G Rao, and F Schilbach (2019), “Behavioral development economics,” in Handbook of Behavioral Economics: Applications and Foundations 1, Elsevier 2: 345–458.

Woodruff, C (2018), “Addressing constraints to small and growing businesses,” Unpublished manuscript.