In India, shadow banks do not compete with traditional banks through a single mechanism – fintech lenders use superior data technology to reach underserved borrowers in unsecured markets, while non-fintech shadow banks exploit lighter regulatory constraints in secured lending. Policymakers should treat these as distinct phenomena, since technology-driven credit expansion offers durable inclusion benefits, while regulation-driven growth may prove fragile as oversight tightens.

Editor’s note: For a broader synthesis of themes covered in this article, check out Issue 3 of our VoxDevLit on Microfinance.

Financial theory has long emphasised traditional banks' informational advantage over other intermediaries. Banks build borrower relationships over time, accumulating soft information difficult to replicate. This relationship banking model has been viewed as a durable competitive advantage.

Despite this advantage of traditional banks, the past decade witnessed explosive shadow banking growth globally. Non-deposit-taking institutions now originate a substantial share of credit in many markets. If traditional banks possess such powerful informational advantages, how do shadow banks compete?

Researchers have proposed two explanations for this puzzle. One argues that shadow banks grow by harnessing superior technology: they use rich hard information, such as transaction histories, past payment behaviour, and other alternative data, to evaluate credit risk more accurately and disburse loans more quickly (Fuster et al. 2019). The other emphasises regulatory arbitrage: because shadow banks face lighter oversight and looser constraints than traditional banks, they can take on more risk and operate with lower capital buffers, giving them a cost and flexibility advantage (Buchak et al. 2018, Irani et al. 2021, Gopal and Schnabl 2022).

These explanations carry vastly different policy implications. Technology-driven growth promises expanded credit availability, improved consumer welfare, and sustainable market evolution. Regulatory arbitrage suggests unsustainable advantages that may collapse when regulatory gaps close.

Our research draws on granular credit bureau lending data, examining the comparative advantages that enable shadow banks to compete effectively across different retail lending markets (Cramer, Ghosh, Kulkarni, and Vats 2025). Our findings suggest that the competitive advantage of shadow banks over traditional banks is not uniform across markets; instead, it depends critically on market characteristics. In uncollateralised lending markets, such as personal loans, fintech platforms leverage technology as their primary advantage, while in collateralised markets such as vehicle loans, non-fintech shadow banks benefit from lighter regulatory oversight. These distinctions have real implications for financial policy, consumer welfare, and the future structure of credit markets.

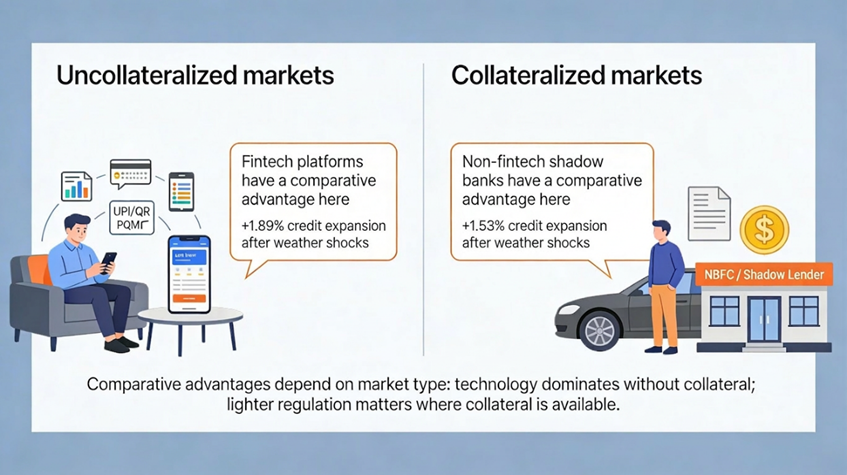

Figure 1: Uncollateralised markets vs. collateralised markets

Using weather shocks to identify competitive advantage

The analysis draws on comprehensive credit bureau data from India's retail lending market, capturing loans made across traditional banks, fintech platforms, and non-fintech shadow banks. India provides an ideal laboratory. Its large, diverse credit market features multiple institutional types, geographic variation in banking infrastructure and financial technology adoption, rich loan-level data, and natural experiments all enable causal identification.

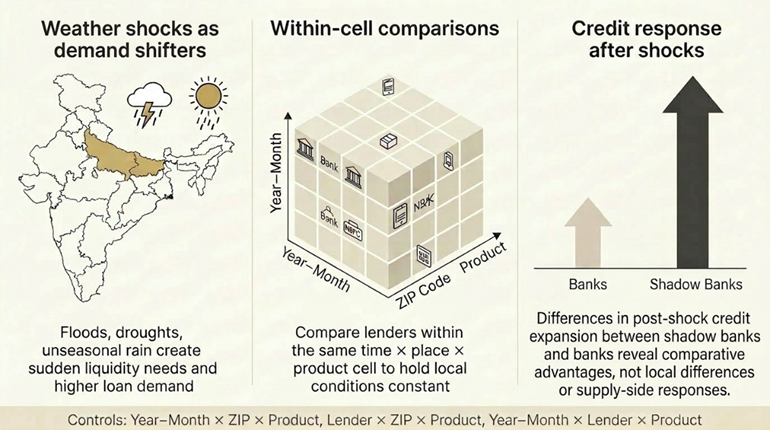

Our methodology employs weather shocks as exogenous demand shifters. When adverse weather (floods, drought, unseasonable rainfall) hits a region, households face liquidity constraints and seek credit. By measuring how different lender types respond to these demand shocks, we isolate competitive advantages while controlling for potential supply-side confounds or strategic pricing.

Figure 2: Identifying the comparative advantage of shadow banks following demand shocks

Notes: The empirical design relies on saturated fixed effects, comparing lenders within tightly defined market cells. Year-month × ZIP code × product fixed effects ensure that within any given month, ZIP, and product, comparisons involve lenders facing identical local demand, competition, and macro conditions. Lender × ZIP code × product fixed effects absorb stable matching between lenders and neighbourhoods or product mixes. Year-month × lender × product fixed effects absorb time-varying shocks at the lender-product level. These controls ensure that the analysis isolates how different lender types adjust to the same demand shock hitting the same market simultaneously, holding constant place, product, and lender conditions.

Shadow banks outperform traditional banks, but not equally

We document substantial differences in how shadow banks respond to liquidity-driven demand shocks:

Fintechs significantly outperform traditional banks, issuing 1.55% more credit after weather shocks within the same geography, time period, and loan category. In aggregate terms, this corresponds to approximately US$3 million per month or US$209 million across the full study period. For median households, the incremental fintech credit represents 8% of urban monthly expenditure and 12% of rural monthly expenditure, indicating economically meaningful impacts on financial inclusion.

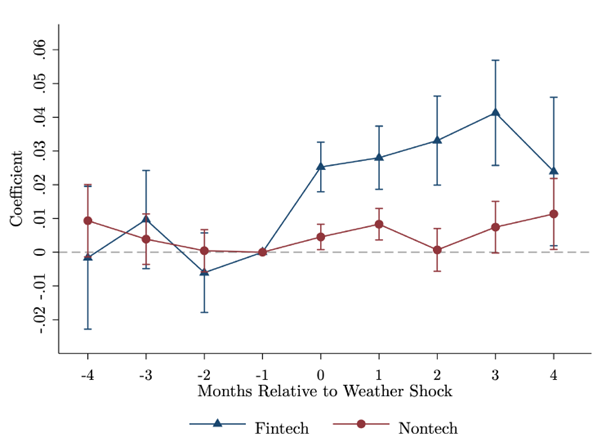

Non-fintech shadow banks also respond positively, issuing 0.31% more credit than traditional banks, but this response is substantially weaker than fintechs. Figure 3 documents the evolution of the response of fintechs and non-fintech around the weather shock.

Figure 3: Dynamics of fintech and non-fintech credit issuance around the weather shock

Market segmentation: Collateralised vs. uncollateralised

The headline response rates mask important heterogeneity. Specifically, the shadow bank responses depend crucially on loan types.

In uncollateralised markets (personal loans, small business loans without collateral), fintechs dominate with substantially stronger credit expansion (1.89%). Technology advantages become paramount, assessing borrower risk without collateral requires sophisticated analysis of transaction patterns, payment history, and behavioural signals. Speed and convenience matter more for short-term, smaller-balance products.

In collateralised markets (vehicle loans, gold-backed loans), non-fintech shadow banks show comparative advantage (1.53% expansion). Regulatory constraints on traditional banks matter more than technology. Collateral reduces information sensitivity, the asset itself provides security, making rapid risk assessment less critical. Regulatory burdens (capital requirements, underwriting standards, consumer protection) place traditional banks at a disadvantage in this market segment.

This market segmentation finding is crucial: it demonstrates that shadow bank variability reflects fundamental differences in how institutional models compete across product markets, not merely fintech versus traditional finance.

The technology mechanism

To isolate technology as a distinct mechanism, our research exploits geographic variation in adoption of India's Unified Payment Interface (UPI), a zero-cost digital payment infrastructure enabling customers to share detailed, verifiable transaction data with lenders. UPI represents a technological asset available to all lenders but differentially utilised by those with technological capabilities (Figure 4).

Figure 4: The UPI transactions history creates a verifiable income information that can be used by fintech lenders to make loan decisions

Fintech lending response to demand shocks increases monotonically with regional UPI adoption. In lowest-quartile UPI regions, fintech lending expands only 0.65%, whereas in highest-quartile regions, expansion reaches 2.32%. This 3.5-fold difference across the UPI distribution demonstrates technology's substantial role in fintech competitive advantage, concentrated primarily in uncollateralised markets where granular transaction data provides maximum informational value.

The regulatory arbitrage mechanism

Our research exploits four natural experiments where regulatory changes created differential impacts across lender types, providing evidence for regulatory arbitrage theory in collateralised markets. Non-fintech shadow banks particularly benefit from reduced regulatory constraints, suggesting their competitive advantage stems partly from avoiding stringent capital, liquidity, and reserve requirements. Our evidence suggests that regulation does not explain fintech advantages in uncollateralised markets.

Complementary role: Expanding credit access

Rather than cannibalising traditional bank lending, shadow banks serve important complementary roles. They disproportionately lend to subprime borrowers with low credit scores and new-to-credit individuals with little formal payment history, roughly 572 million people in India, including 20% with low scores and 50% who are new to credit.

Fintech lending concentrates in regions with limited traditional bank presence, particularly where sparse branch networks or regulatory constraints exist. Using Facebook social network data as proxy for informal risk-sharing, we find fintech lending substantially higher in areas with weaker informal insurance, suggesting digital credit partially substitutes for missing formal finance.

Critically, increased shadow bank lending after weather shocks does not raise default risk. Despite serving riskier borrowers, shadow banks do not experience substantially higher default rates, pointing to genuine competitive advantage rooted in superior screening, monitoring, and operational technology.

Policy implications

For fintech platforms, technology-based advantages are durable and expanding as digital infrastructure deepens. Sustained growth depends on real risk-assessment capabilities, not regulatory gaps. Unsecured lending is the natural competitive domain, positioning as complements to banks strengthens long-run viability.

For non-fintech shadow banks, business models built primarily on lighter regulation are unlikely to be stable as supervisory standards converge. Investment in data and digital capabilities becomes increasingly necessary.

For traditional banks, regulatory requirements are policy choices that can be recalibrated. Investments in transaction data analytics may help compete in uncollateralised segments. Markets with weak informal insurance and large underbanked populations represent growth opportunities.

For policymakers, regulatory interventions could accelerate technology adoption. Shadow banks have real capacity to reach historically excluded households. Public investment in transaction data ecosystems can generate positive spillovers. Well-designed digital infrastructure can advance both borrower welfare and competitive efficiency.

Beyond credit market outcomes, shadow bank lending appears to buffer the real economy against climate-related disruptions. Using geographic variation in digital payment adoption as an instrument for fintech credit expansion, we find that areas receiving more fintech credit after weather shocks experience smaller declines in local economic activity. This suggests that fintechs can help smooth consumption and production fluctuations caused by extreme weather — a particularly important function in emerging economies, where climate vulnerability is high and traditional insurance mechanisms are often absent.

The rise of shadow banking reflects neither monolithic trends nor single mechanisms. Different institutional models evolved comparative advantages reflecting fundamental capabilities: fintech platforms excel through technology-enabled risk assessment where collateral is unavailable and speed matters; non-fintech shadow banks benefit from regulatory flexibility enabling profitable lending where regulations constrain traditional banks; traditional banks retain advantages in relationship-based lending and borrowers with strong credit histories.

Complementary roles that shadow banks play in serving underbanked populations, filling geographic gaps, and substituting for absent informal insurance suggest credit market structure is expanding overall access. As digital payment infrastructure expands globally, technology advantages will increasingly drive competitive advantage in unsecured lending, holding substantial promise for financial inclusion within appropriate policy frameworks recognising market segmentation.

References

Buchak, G, G Matvos, T Piskorski, and A Seru (2018), "Fintech, regulatory arbitrage, and the rise of shadow banks," Journal of Financial Economics, 130: 453–483.

Cramer, K F, P Ghosh, N Kulkarni, and N Vats (2025), "Shadow banks on the rise: Evidence across market segments," Unpublished manuscript.

Fuster, A, M Plosser, P Schnabl, and J Vickery (2019), "The role of technology in mortgage lending," The Review of Financial Studies, 32: 1854–1899.

Gopal, M, and P Schnabl (2022), "The rise of finance companies and fintech lenders in small business lending," The Review of Financial Studies, 35: 4859–4901.

Irani, R M, R Iyer, R R Meisenzahl, and J Peydro (2021), "The rise of shadow banking: Evidence from capital regulation," The Review of Financial Studies, 34: 2181–2235.