In India, expanding deposit insurance coverage improved depositor welfare by reducing risk and encouraging a shift towards safer assets.

Editor's note: The authors have made slides available to accompany this research here.

There is an ongoing debate in India about the potential increase in the ceiling for deposit insurance coverage. On one hand, broader protection is associated with stronger depositor confidence, reduced risk of bank runs, and greater financial stability, as emphasised in Diamond and Dybvig (1983). On the other hand, higher coverage may weaken market discipline, leading banks to engage in riskier practices and raising the probability of failure. As a result, the overall welfare effects of expanding deposit insurance remain ambiguous.

Our research contributes to this debate by proposing a novel mechanism through which deposit insurance affects depositor welfare. Deposit insurance limits the supply of safe, liquid assets: deposits are fully safe only up to the insurance threshold, beyond which they are exposed to default risk. To study this mechanism, we develop a theoretical framework in which depositors allocate wealth between a safe (deposits) and a risky asset. The main insight of this model is that, when there is a positive probability of bank failure, investors with a high demand for safe assets face a binding constraint.

These investors would prefer to hold a larger share of their wealth in safe assets. However, since deposits are insured only up to the threshold, they tend to place the maximum covered amount in deposits and invest any excess funds in risky assets, such as stocks or mutual funds. When the insurance threshold rises, the risk associated with deposits falls, relaxing this constraint and allowing depositors to expand their deposits. As a result, deposits increase and stock holdings decrease. The most significant adjustments occur among those who previously bunched at the old threshold as they faced the tightest constraint.

In our research (Ghosh, Limodio, and Vats 2025), we leverage the February 2020 increase in the deposit insurance limit in India – from INR 100,000 to 500,000 – as a natural experiment to study how deposit insurance influences portfolio allocation. For this purpose, we use detailed household finance data that includes information on deposit holdings, spending, and ISIN-level investment in the stock market and mutual funds.

The bunching behaviour of depositors

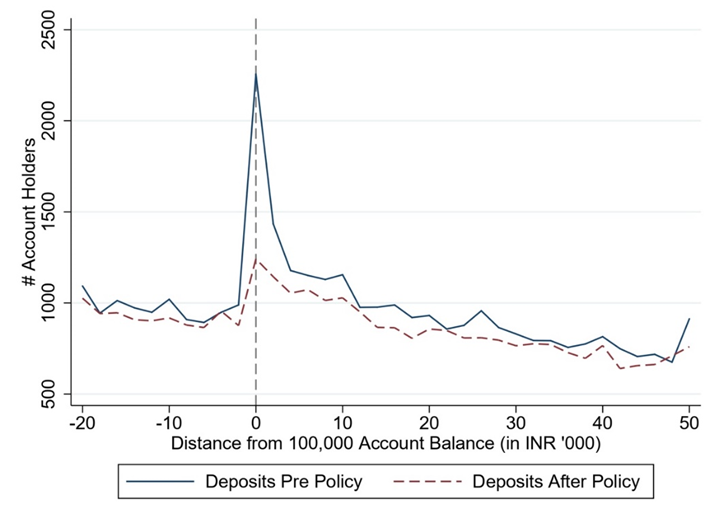

Figure 1 presents the distribution of depositors before and after the policy change within a narrow range of INR 80,000 to 150,000. The solid blue line represents the pre-policy distribution, while the dashed maroon line indicates the post-policy distribution. The vertical dashed grey line marks the INR 100,000 threshold, standardised at zero. The figure reveals a significant spike in the number of account holders at the old deposit insurance threshold, indicating excessive bunching of deposits at this level. Another key finding from Figure 1 is the substantial reduction in bunching around the INR 100,000 threshold following the increase in the deposit insurance limit. Specifically, the degree of bunching at this threshold decreases by approximately 35%, meaning that around 35% of depositors moved their balances away from the INR 100,000 threshold. This suggests that the incentives for depositors to concentrate their balances at INR 100,000 were significantly reduced after the DI limit was raised to INR 500,000 in February 2020.

Figure 1: Bunching of depositors at pre-policy deposit insurance threshold

Portfolio reallocation and deposit insurance expansion

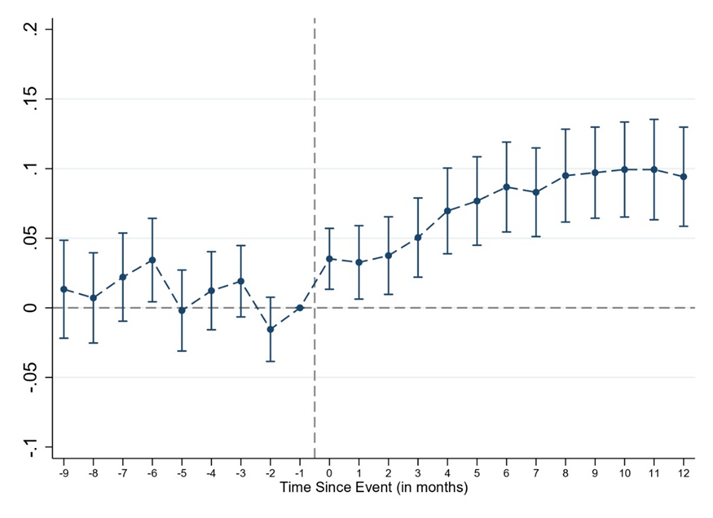

Next, we take advantage of a key prediction of our model, which highlights a source of cross-sectional variation in the response of depositors to deposit insurance. To implement this methodology, we build on the approaches in public economics developed by Chetty et al. (2011), Luttmer and Singhal (2014), and Kleven (2016). Specifically, we employ a bunching-in-differences approach to estimate the impact of deposit insurance changes on portfolio allocation. This design combines the bunching behaviour induced by a policy threshold with a differences-in-differences strategy that exploits the response of bunchers to a shift in the threshold.

We compare the behaviour of depositors who clustered around the former threshold of INR 100,000 to that of those who did not, before and after the expansion of deposit insurance coverage. On average, we find that bunchers raise their balances by 5.2% relative to non-bunchers after the policy change. Figure 2 visually describes this heterogenous response by plotting the average monthly deposit over time for bunchers relative to non-bunchers, before and after the deposit insurance expansion.

Figure 2: Assessment of pre-trends

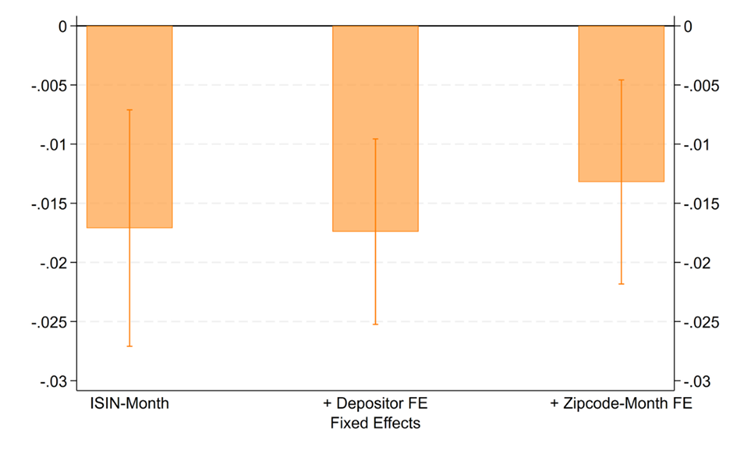

An important intuition of this research is that deposit growth among bunchers is largely financed through portfolio reallocation. We test this intuition and find that the sharp increase in deposits among bunchers is primarily driven by depositors who participate in the retail trading of stocks and mutual funds. Specifically, non-trading bunchers show minimal response compared to non-bunchers. Consistent with this interpretation, Figure 3 illustrates the differential effect of deposit insurance expansion on the total amount invested in each security by bunchers and non-bunchers. Specifically, it indicates that bunchers liquidate 1.3–1.7%, depending on model specification, more of their holdings relative to non-bunchers for the same security after the deposit insurance expansion.

Figure 3: Stock liquidation by bunchers vs. non-bunchers

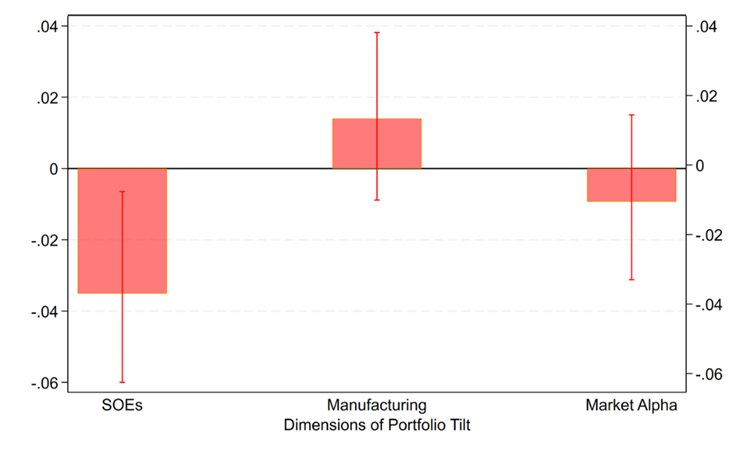

Interestingly, because bunchers invest in the stock market to compensate for their unmet demand for safe assets, our intuition is that they tend to favour relatively safer securities and are more likely to sell these assets to finance their increased deposits following a deposit insurance expansion. This intuition aligns with the evidence presented in Figure 4, which shows the change in portfolio tilts for each stock characteristic for bunchers after the deposit insurance expansion. Specifically, it indicates that bunchers tilt their investments away from state-owned firms, which are backed by government guarantees and generally regarded as safe investments in India. In contrast, there is no significant change regarding other characteristics, such as market alpha or sector of operations.

Figure 4: Bunchers reduce exposure to state-owned firms

Finally, we assess welfare effects, accounting for the possibility that higher insurance coverage encourages banks to take on greater risk. We show that even sizable increases in the probability of bank failure did little to offset depositor welfare gains. For example, eliminating these gains would require a 70–100% increase in expected failure probability. Under realistic assumptions, the net benefits of deposit insurance expansion are positive across the distribution.

Policy implications: Deposit insurance

This research highlights three important policy implications:

- First evidence on welfare effects of deposit insurance expansion: Our research provides evidence regarding the welfare impact of deposit insurance expansion on households, specifically through their portfolio allocations. We demonstrate that because deposit insurance restricts the supply of safe, liquid assets available to households, its expansion can generate significant positive welfare effects for these households. This finding is important as many other countries, including India, are considering further revisions to their deposit insurance limits.

- Introduction of a novel risk measure – buncher share: The proportion of ‘bunchers’ (depositors who concentrate their holdings at certain thresholds) serves as a sufficient statistic for regulators to estimate the implied probability of bank failure from the depositors' perspective. This measure offers a depositor-centred perspective, contrasting with existing measures based on equity or bond markets. Given that the Reserve Bank of India has recently moved towards risk-based deposit insurance pricing, this measure could be instrumental in shaping such pricing strategies.

- Impact of deposit insurance on fund reallocation and market pricing: Our findings indicate that depositors reallocate funds between bank deposits and other segments of the economy, such as stocks in seemingly safer state-owned enterprises. This reallocation can have short-term implications for the pricing of these investments. Therefore, regulators should consider these effects when evaluating the broader economic impact of deposit insurance expansion, particularly regarding the pricing and allocation of capital in related markets.

References

Chetty, R, J N Friedman, T Olsen, and L Pistaferri (2011), “Adjustment costs, firm responses, and micro vs. macro labor supply elasticities: Evidence from Danish tax records,” Quarterly Journal of Economics 126(2): 749–804.

Diamond, D W, and P H Dybvig (1983), “Bank runs, deposit insurance, and liquidity,” Journal of Political Economy 91(3): 401–419.

Ghosh, P, N Limodio, and N Vats (2025), “Household portfolio and deposit insurance: Implications for the supply of safe assets,” Unpublished manuscript.

Kleven, H J (2016), “Bunching,” Annual Review of Economics 8(1): 435–464.

Luttmer, E F, and M Singhal (2014), “Tax morale,” Journal of Economic Perspectives 28(4): 149–168.